{kind=link}

Inside This Week’s Bull Bear Report

- 2024 Assessment – One other 20% 12 months

- How We Are Buying and selling It

- Analysis Report – The ACA & The Inflation Of Healthcare

- Youtube – Earlier than The Bell

- Market Statistics

- Inventory Screens

- Portfolio Trades This Week

Final Likelihood For Early Chook Registration

Since New 12 months’s fell in the course of the week, I’m extending the “Early Chook Low cost” for our upcoming RIA 2025 Financial Summit via Sunday for our weekly e-newsletter readers.

Don’t miss the chance to get your tickets for the 2025 Financial and Investing Summit earlier than costs improve on Monday to $149. Seating may be very restricted, and we can have time to go to personally with attendees to reply your burning questions on 2025.

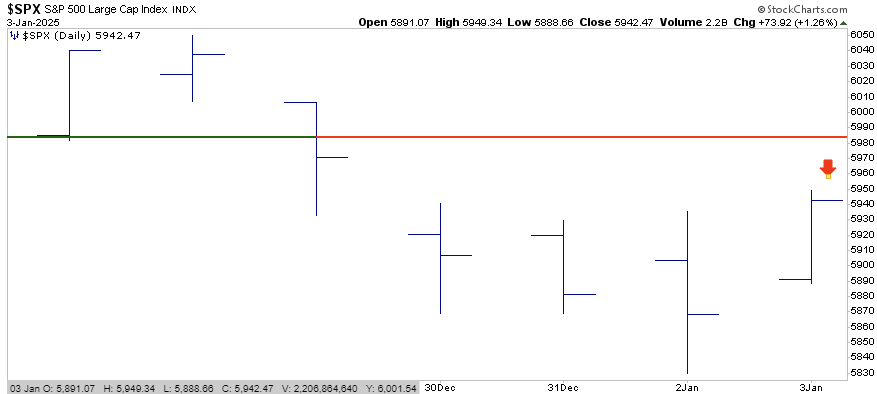

Santa Is A No-Present

Final week, we mentioned the way it appeared as if Santa arrived on Christmas Eve, pushing the markets again above the essential 50-DMA. Nevertheless, by the top of the 12 months, it appeared buyers have been naughty this 12 months and acquired a “lump of coal,“ with markets promoting off again towards current lows. One essential be aware was that momentum and relative energy remained weak, preserving promoting stress intact.

There isn’t a approach to sugarcoat the market’s poor efficiency. Whereas December began with a bang, it ended with a whimper, with a protracted stretch of day by day losses into year-end. Now, 2025 is opening with a whimper. Small caps fell aside after making an attempt to “make a comeback,” and total market breadth declined. Nevertheless, with the markets now oversold, we must always anticipate a rally heading into the Presidential inauguration, which seemingly began on Friday.

Regardless of Friday’s spectacular reflexive rally, the market fell about 0.5% wanting rallying sufficient to save lots of the “Santa Rally.”

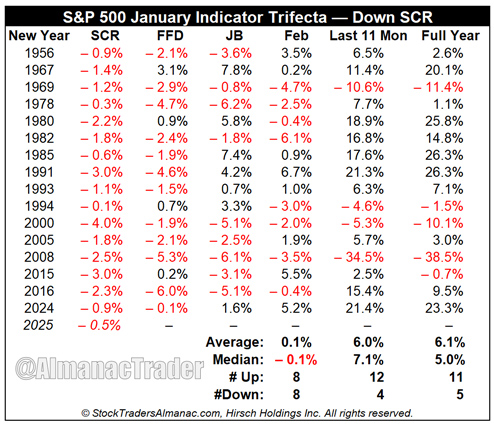

Nevertheless, though the “Santa Rally” did not materialize, bullish hopes for 2025 aren’t but misplaced.

“Since 1950, when all three January indicators (The Santa Claus Rally (SCR), First 5 Days (FFD) and the full-month January Barometer (JB)) are up, the S&P 500 was up 90.6% of the time (29 out of 32 years) with a mean acquire of 17.7%. When a number of of the Trifecta is down, on this case, the SCR, the 12 months is up 59.5% of the time (25 of 42) with a paltry common acquire of two.9%.” – Stocktraders Almanac

Whereas the dearth of a Santa rally is disappointing, as famous by Stocktraders Almanac:

“Of the 16 down SCRs since 1950, 11 years have been up and 5 down, however the common acquire is a tepid 6.1%.“

Nevertheless, even with a failed Santa rally, the January barometer holds the important thing for the 12 months. Traditionally, a optimistic January has been a bullish signal for shares. The chart under highlights that the favored Wall Avenue maxim has stood the take a look at of time. Since 1950, the S&P 500 has posted a mean annual return of 16.8% throughout years that included a optimistic January. Moreover, the index generated optimistic returns in 89% of those years. In distinction, when the index traded decrease in January, annual returns dropped to -1.7%, with solely 50% of occurrences yielding optimistic outcomes.

With the bulls needing a optimistic January efficiency, the market has its work reduce out. Nevertheless, with the market’s short-term oversold and breadth, there’s a affordable technical setup for an enchancment in efficiency in January.

Nevertheless, will 2025 be one other banner 12 months? Possibly. However the market actually faces headwinds, from elevated earnings expectations to valuations. Our greatest guess is that whereas this 12 months will seemingly see a continuation of the bull market cycle, will probably be punctuated by elevated bouts of volatility that may weigh on investor sentiment. In different phrases, “buckle up and hold your arms and belongings contained in the automobile.”

This week, we’ll do a brief 2024 evaluation.

Want Assist With Your Investing Technique?

Are you in search of full monetary, insurance coverage, and property planning? Want a risk-managed portfolio administration technique to develop and defend your financial savings? No matter your wants are, we’re right here to assist.

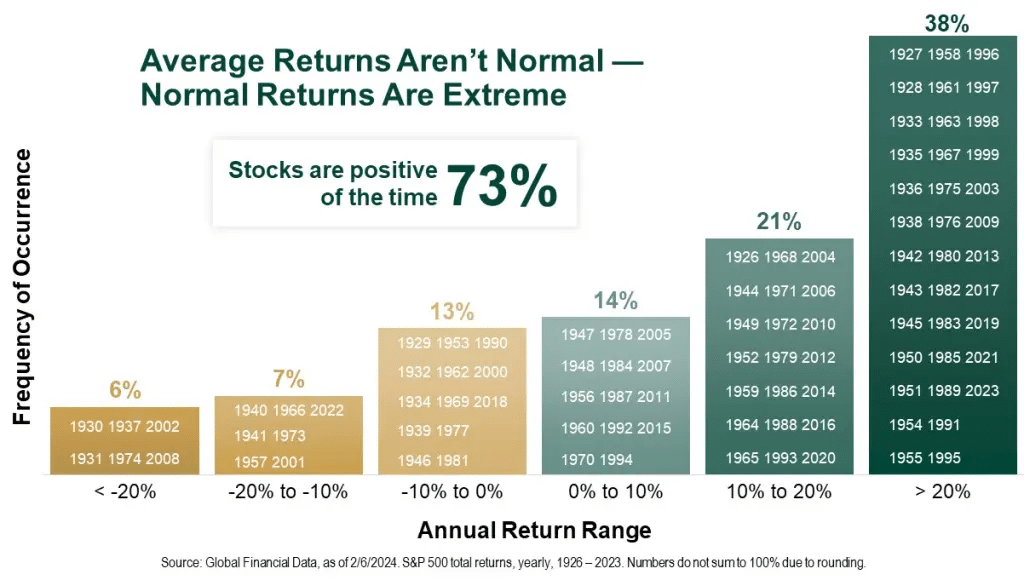

2024 Assessment – One other 20% Plus 12 months

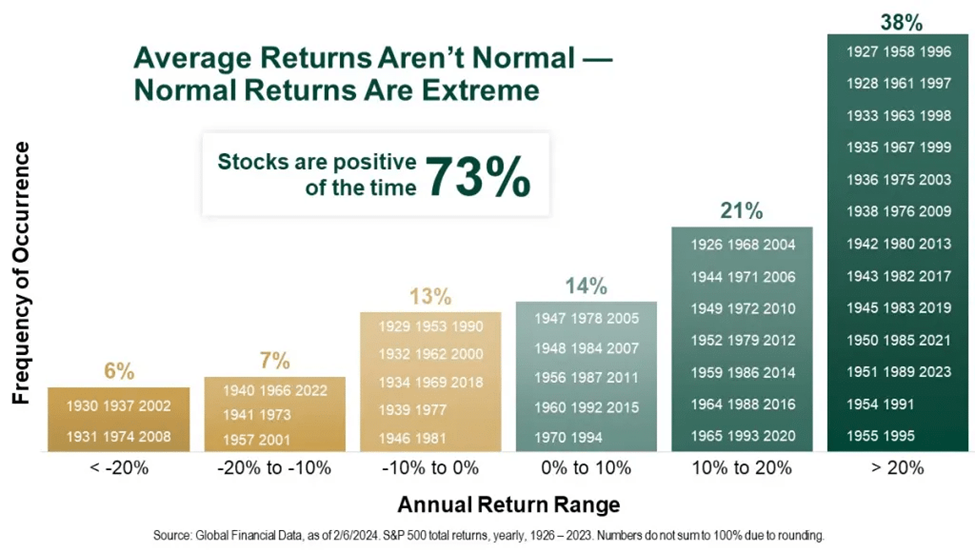

The market had one other 20% plus return for the 12 months. As we mentioned beforehand, the market not often delivers an “common” return of 8-10%. About 38% of the time, the market delivers 20% or extra returns.

Since 1900, the inventory market has “averaged” an 8% annualized fee of return. Nevertheless, this does NOT imply the market returns 8% yearly. As we mentioned not too long ago, a number of key details about markets ought to be understood. Shares rise extra typically than they fall: Traditionally, the inventory market will increase about 73% of the time. The opposite 27% of the time, market corrections reverse the excesses of earlier advances. The desk under exhibits the dispersion of returns over time.”

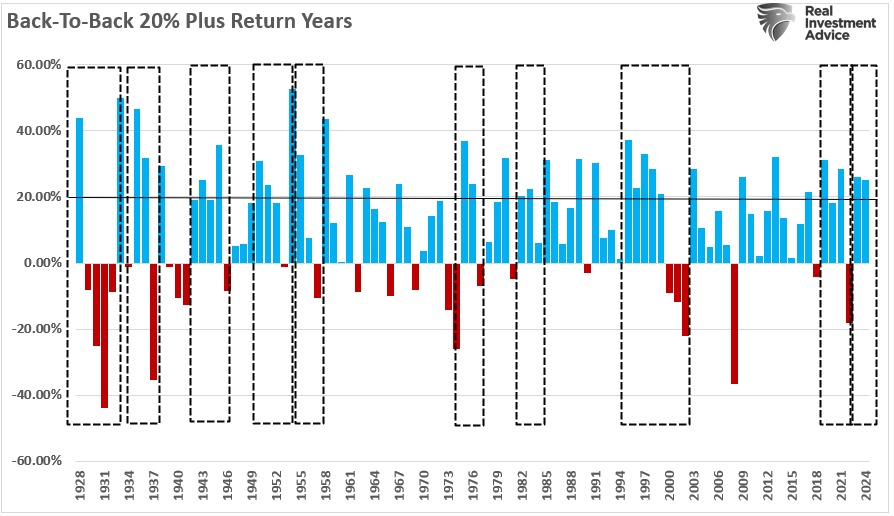

For analysts, being completely “bullish” results in a 73% success fee on market calls, which, in case you are an expert baseball participant, a .730 batting common will enshrine you within the “Corridor Of Fame.” Nevertheless, as buyers, the issue with being all the time bullish is the impression on our portfolios for the “different” 27% of outcomes. That is essential in the historical past of 20% plus annual returns. Within the desk above, within the far-right column, there are durations the place 20% plus good points have been clustered.

{kind=link}

So, what does that imply?

The Lengthy Time period

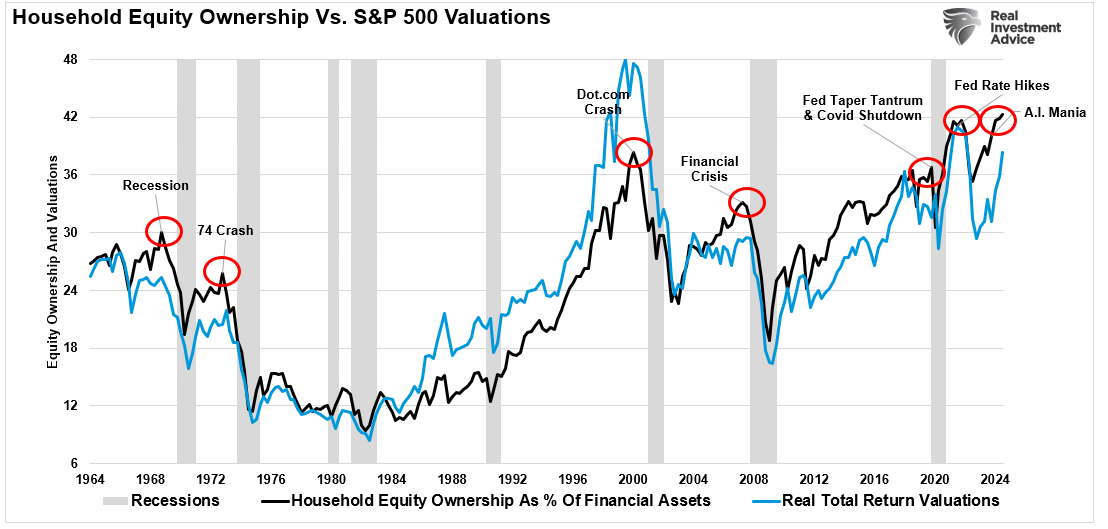

It’s price noting that these durations of “well-above-average” returns have been adopted by “well-below-average” returns. As proven, these durations of “mean-reversion” have been typically triggered by some occasion that reversed elevated valuation ranges.

As we see available in the market, these durations of extra valuations are a psychological byproduct of investor sentiment. Our 2024 evaluation discovered that investor allocations to equities reached a report, equivalent to a pointy improve in valuation ranges as buyers have been keen to overpay for earnings progress.

{kind=link}

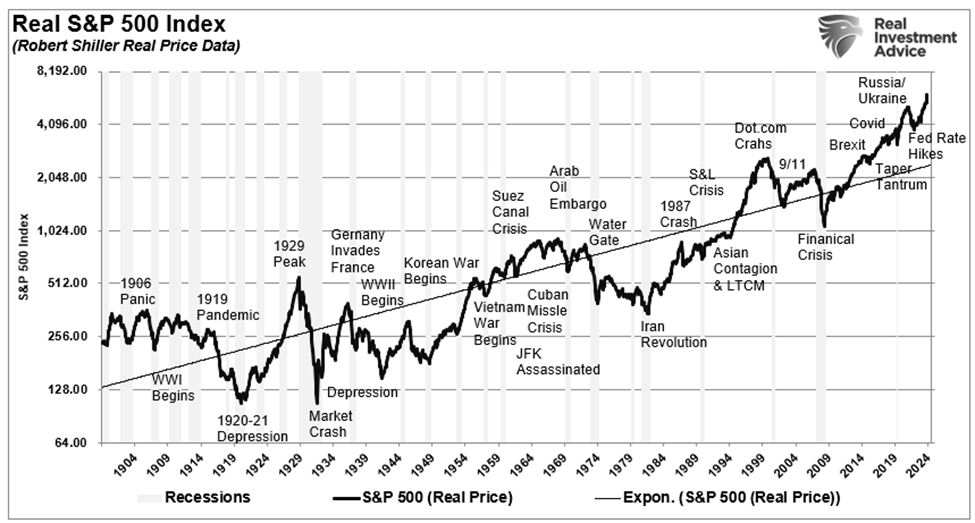

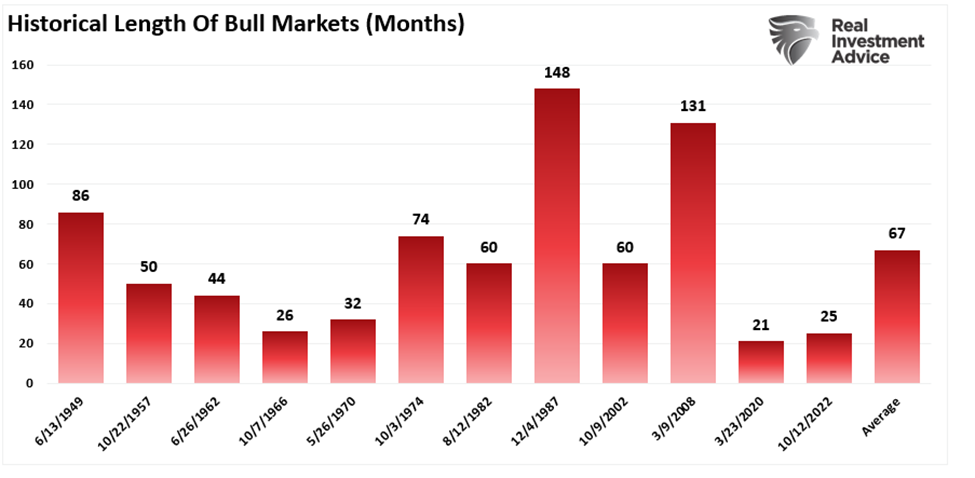

As asset costs rise, hypothesis. will increase, making a “suggestions loop.” The extra asset costs rise, the extra assured buyers develop into, resulting in additional worth will increase fueling a bull market. The chart under exhibits the size of earlier bull markets all through historical past, with the common size of bull markets working about 5 1/2 years.

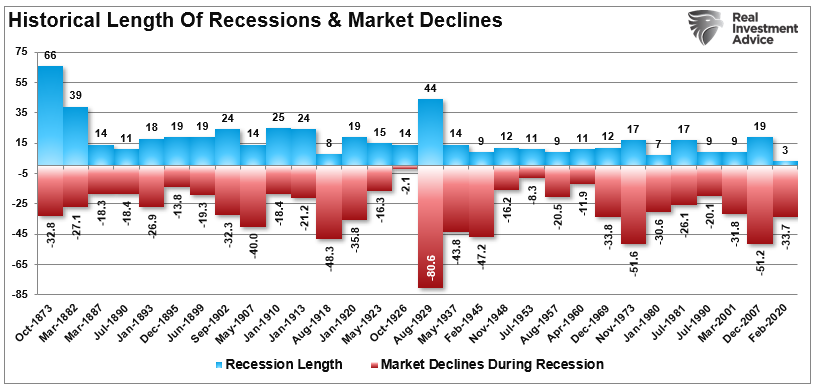

Nevertheless, whereas the lengthy length of bull markets favors being bullish, the issue is that finally, some “occasion” happens that causes a reversal of expectations. When that happens, buyers reprice the market again to actuality. As proven, bear markets and the following recessions are typically very brief. Most bear markets final lower than 18 months and are extra painful experiences.

Does that imply 2025 will probably be a “imply reverting” 12 months? No. Nevertheless, as mentioned on this 2024 evaluation, there are specific warning indicators that subsequent 12 months may very well be very completely different.

{kind=link}

2024 Assessment – A 12 months Of Focus

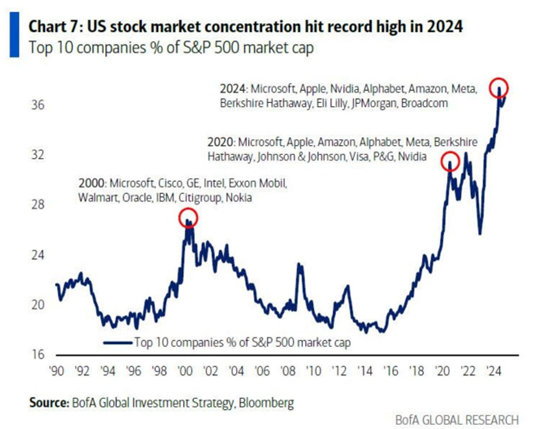

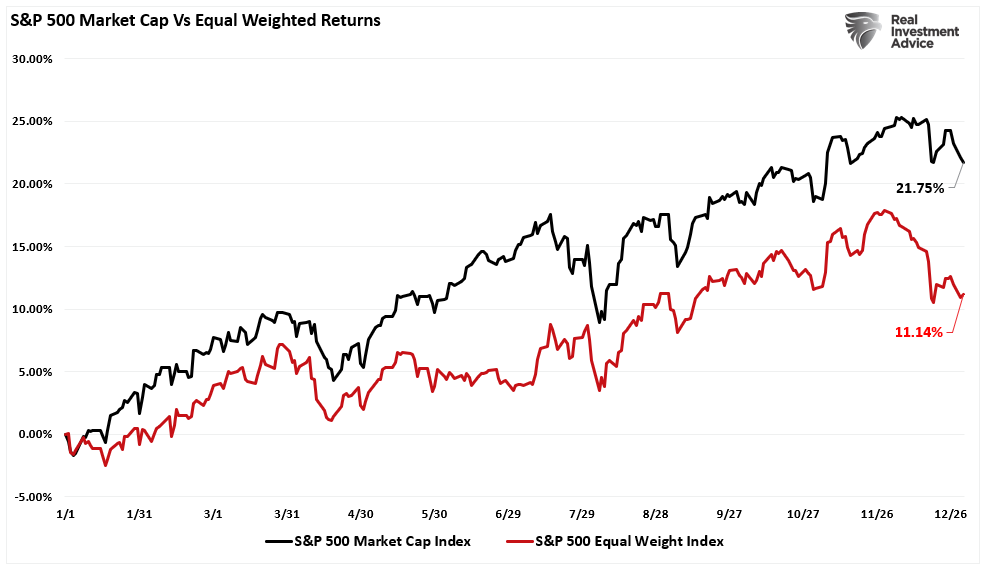

For the second 12 months in a row, the one huge standout was the extent of market focus. The “Mega-cap” shares have develop into an ever-increasing share of the S&P 500 index. We’ve got not witnessed this because the early 70s with the “Nifty-Fifty” and simply earlier than the “Dot.com” crash.

Over the previous few years, capital flows into the biggest market capitalization shares have led to an growing skew between the “have and have nots.” Over the past 12 months, the businesses that dominate the market capitalization weighting of the S&P 500 index created a considerable outperformance over the equal-weighted index.

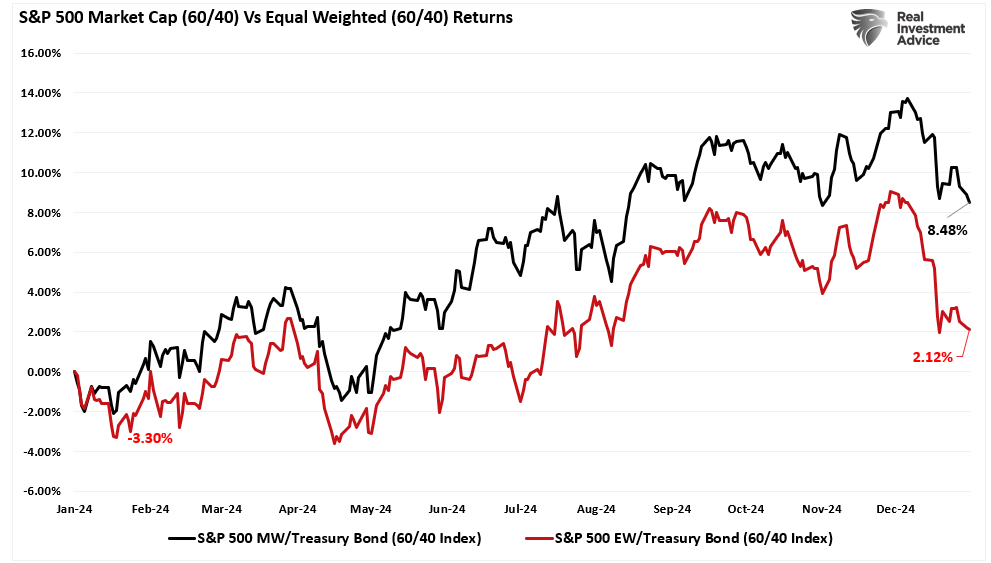

Talking of the “have-nots,” the 60/40 allocation lagged far behind the S&P 500 index on a efficiency foundation as bonds struggled with “sticky inflation” and continued to push to extend portfolio danger as buyers chased asset costs larger.

Nevertheless, that continued efficiency chase has led to essentially the most important rolling two-year efficiency unfold between the market capitalization and equal-weighted index since 2008 and 2019.

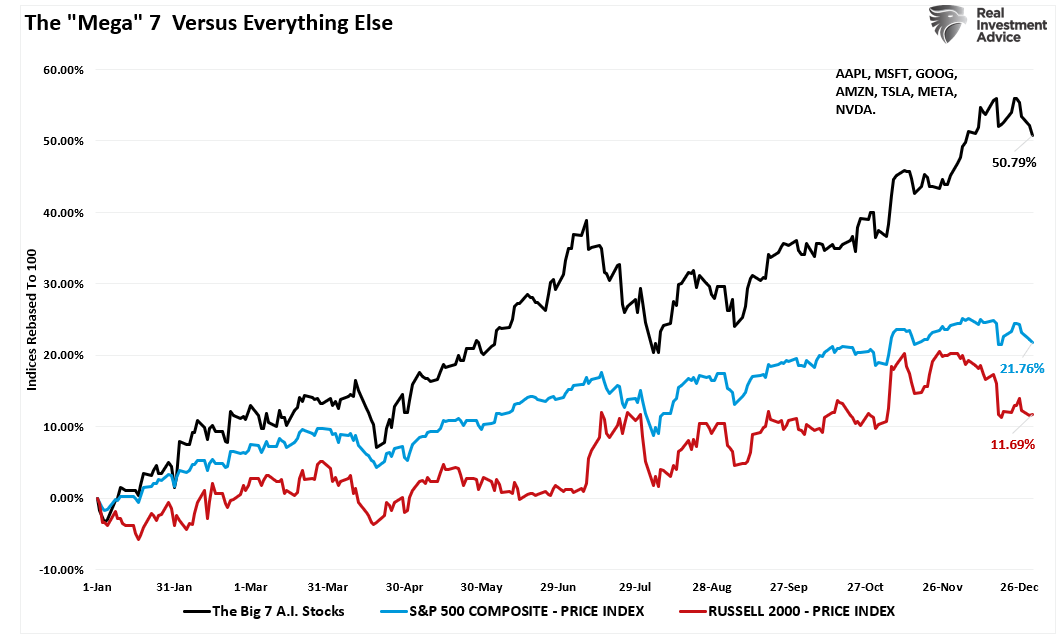

Whereas the surge in market focus has been notable during the last two years, the chase for efficiency has been a rising difficulty since 2014. As proven, the Nasdaq and S&P 500 (each market-capitalization-weighted and dominated by the identical shares) have massively outperformed every part from small and mid-capitalization firms to gold, oil, and bonds.

Notably, in 2024, the “Mega 7” market-capitalization firms returned 50%, whereas the S&P 500 was larger by 22%, and the Russell 2000 trailed far behind, rising simply 12%.

The query is, why is that this occurring?

2024 Assessment – Hypothesis Goes Parabolic

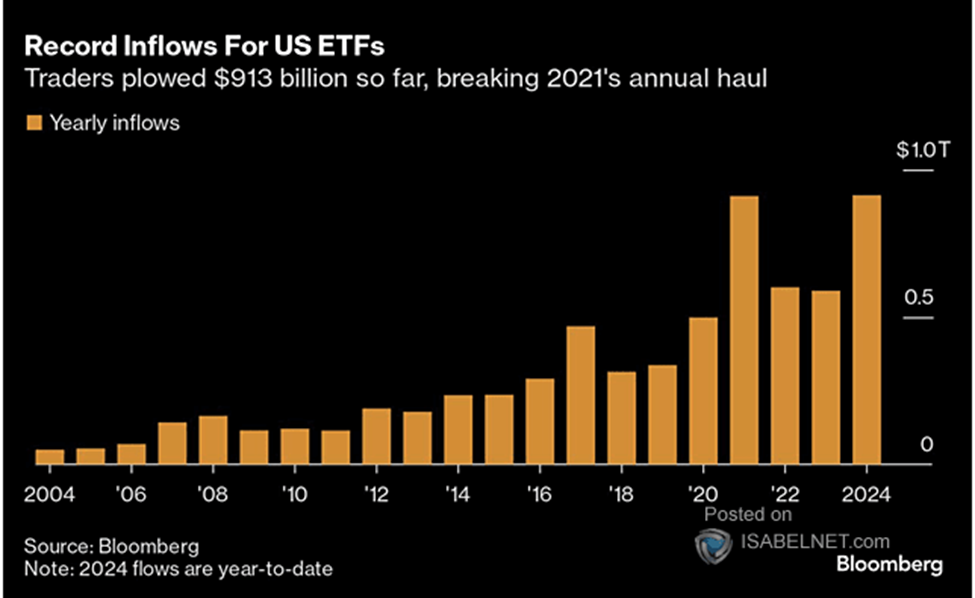

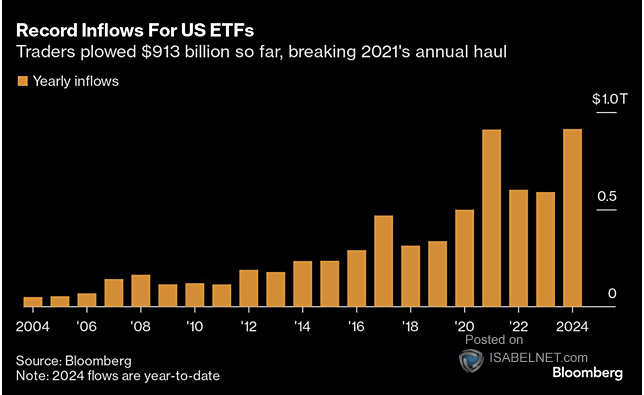

As mentioned, the surge in “Alternate-Traded Funds” or “ETFs” has modified the investing panorama.

“Following the 2020 pandemic shutdown, the Authorities and Federal Reserve went into overdrive, offering spherical after spherical of fiscal and financial help. Cash flooded the financial system, from PPP Loans to hire moratoriums, $1500 checks on to customers, debt forgiveness, zero rates of interest, and quantitative easing. Unsurprisingly, a lot of that cash entered the monetary markets, and retail buyers plowed practically $900 billion in market-related ETFs. Curiously, in 2024, most of these helps are gone, rates of interest have risen sharply, and the Federal Reserve is lowering its steadiness sheet. But, someway, buyers discovered a approach to push $913 billion (YTD) into ETFs, which is a report influx.”

That surge of capital into ETFs contributed to the outsized efficiency of enormous capitalization firms, primarily the “Magnificent 7,” relative to the remainder of the index, as proven above. This occurs as a result of most of those passive ETFs are market capitalization-weighted.

{kind=link}

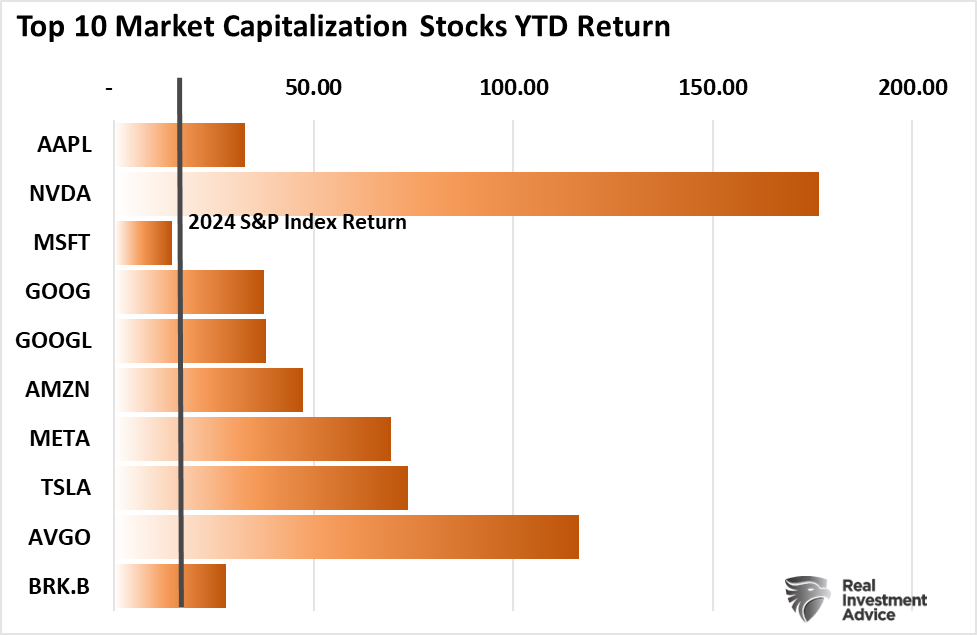

For instance, each ETF that tracks the S&P 500 index, the Nasdaq, or some variation thereof has the identical prime holdings. At present, the highest 10 shares comprise roughly 40% of these ETFs.

Subsequently, each time somebody invests $1 into a kind of ETFs, roughly 40 cents of that greenback flows into simply 10 shares. Such is why, in our 2024 evaluation, these 10 shares, besides Microsoft, outperformed the S&P 500 index by a large margin.

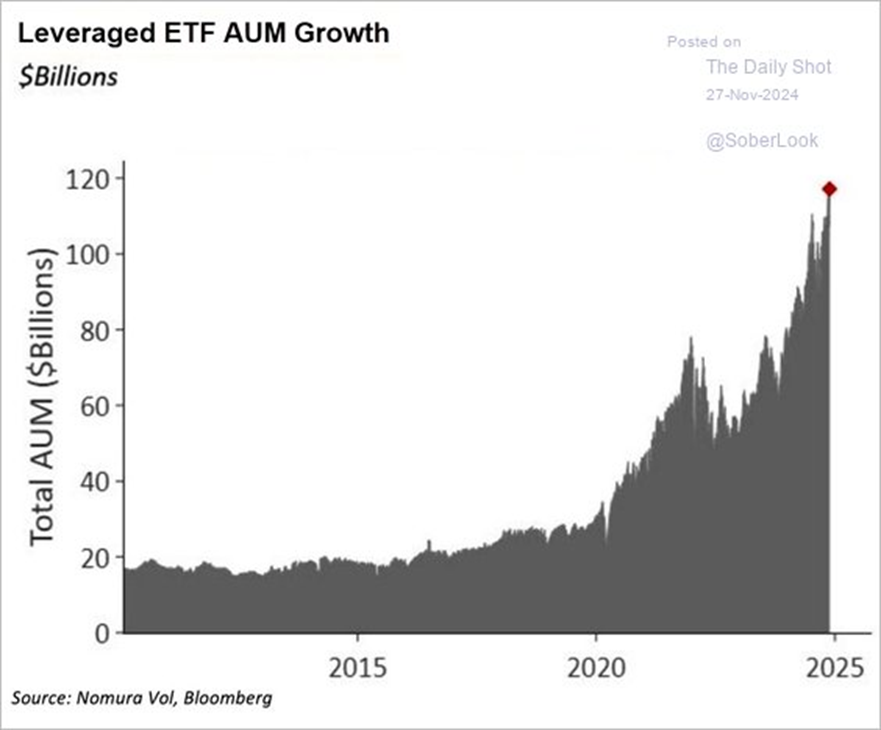

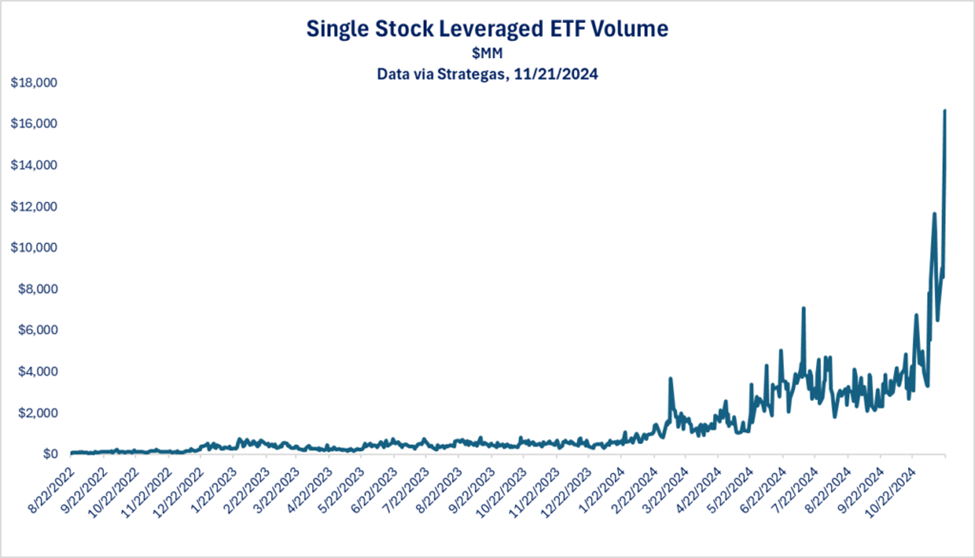

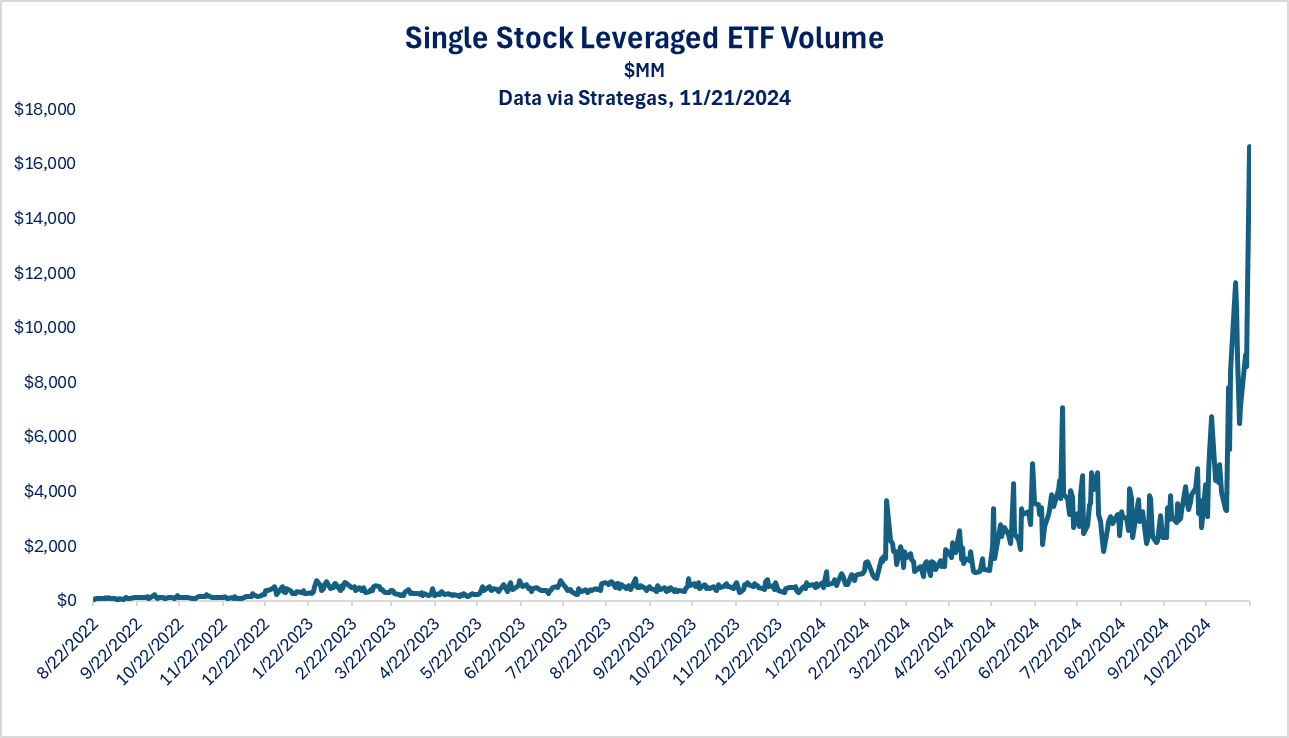

The byproduct of persistently rising costs and buyers’ chase for efficiency creates demand for Wall Avenue to supply extra merchandise for buyers to buy. Because of this 2024 noticed a large improve in single-stock ETFs and, extra critically, leveraged ETFs.

The rising demand by buyers to leverage speculate available in the market is a subject we lined not too long ago in our Each day Market Commentary and is the hallmark of our 2024 evaluation:

“We see surging quantity in leveraged single-stock ETFs. An instance of such an ETF is Granite Shares NVDL. The ETF presents a 2x leveraged holding of Nvidia shares. If Nvidia falls by 3%, the ETF will decline by 6%. Conversely, if Nvidia rises by 5%, the ETF will climb 10%. Accordingly, leveraged single-stock ETFs could be extremely speculative. Moreover, the large surge in quantity in such ETFs, as we share under, additional confirms speculative behaviors are rising.

Leverage and excessive hypothesis can drive markets larger than most buyers forecast. Nevertheless, within the course of, they create a divergence between fundamentals and valuations, thus exposing the markets to danger. Elevated leverage and hypothesis aren’t causes to promote instantly, however they point out that markets are getting frothy, warranting our shut consideration.“

The essential level is that whereas 2024 was a fantastic 12 months within the markets, historical past means that expectations for 2025 ought to seemingly be tempered. Such brings us to the plain query, “What ought to I be looking ahead to to sign a shift in investor sentiment?”

{kind=link}

2024 Assessment – What To Watch For In 2025

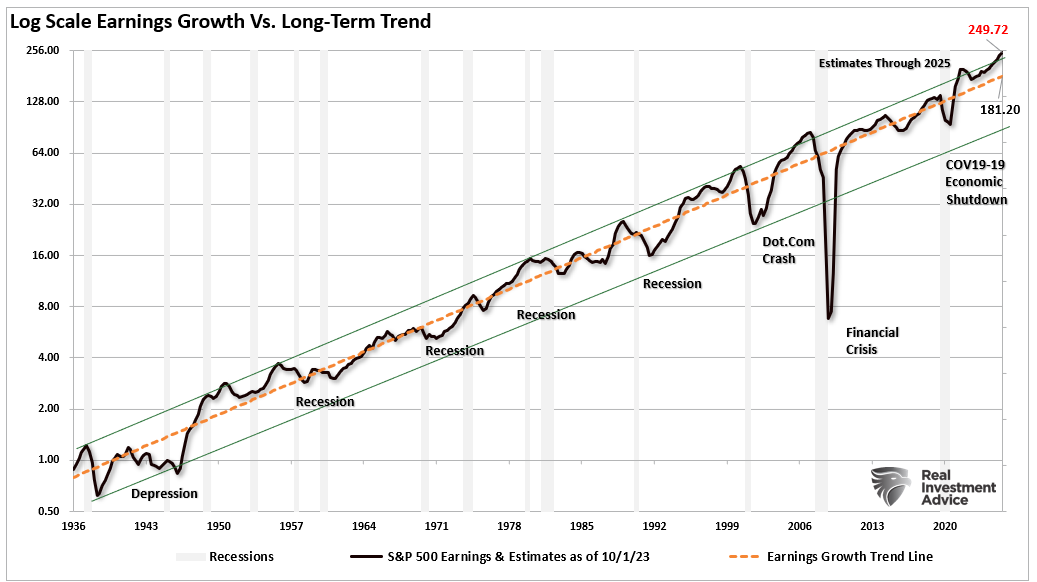

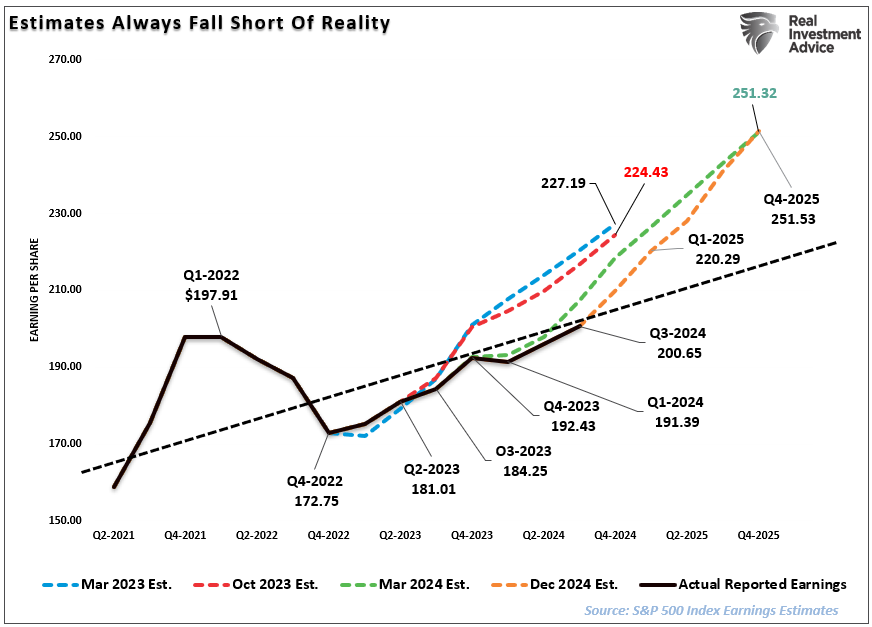

Whereas buyers are giddy with returns over the previous 12 months, that exuberance has elevated the expectation that issues will proceed in 2025. After all, earnings progress would be the greatest driver for returns in 2025.

Ahead earnings estimates are optimistic and effectively above their long-term historic logarithmic progress pattern. Analysts anticipate the S&P 500 will see earnings attain $249/share from $208/share on the finish of 2024. That’s an anticipated progress fee of 19% for earnings. Nevertheless, that present estimate is $68/share above historic earnings’ long-term exponential progress pattern. Whereas such deviations existed beforehand, they have been normally near the purpose the place such optimism ended. The ends of these exuberant durations of earnings progress typically coincided with a recession or a mean-reverting occasion. Nevertheless, whereas estimates are at present very elevated, they will stay elevated longer than you suppose attainable.

The timing of “the” occasion that reverses extra excessive investor exuberance and hypothesis is all the time essentially the most difficult. Nevertheless, it all the time happens when it’s least anticipated. As we enter 2025, investor sentiment of anticipated inventory returns over the following 12 months is close to the best ranges on report. On the identical time, credit score spreads stay close to the bottom ranges on report, confirming the excessive diploma of complacency in as we speak’s markets.

{kind=link}

Such exuberance and overconfidence are inclined to precede some degree of disappointment.

Earnings Matter Extra Than You Suppose

Probably the most important danger in 2025 is an occasion that causes a major decline in earnings expectations. As proven, there’s a very excessive correlation between earnings tendencies and the speed of change in asset costs.

As I mentioned in “Predictions For 2025:”

“The issue with present ahead estimates is that a number of elements should exist to maintain traditionally excessive earnings progress.

- Financial progress should stay extra sturdy than the common 20-year progress fee.

- Wage and labor progress should reverse to maintain traditionally elevated revenue margins, and,

- Each rates of interest and inflation should reverse to very low ranges.

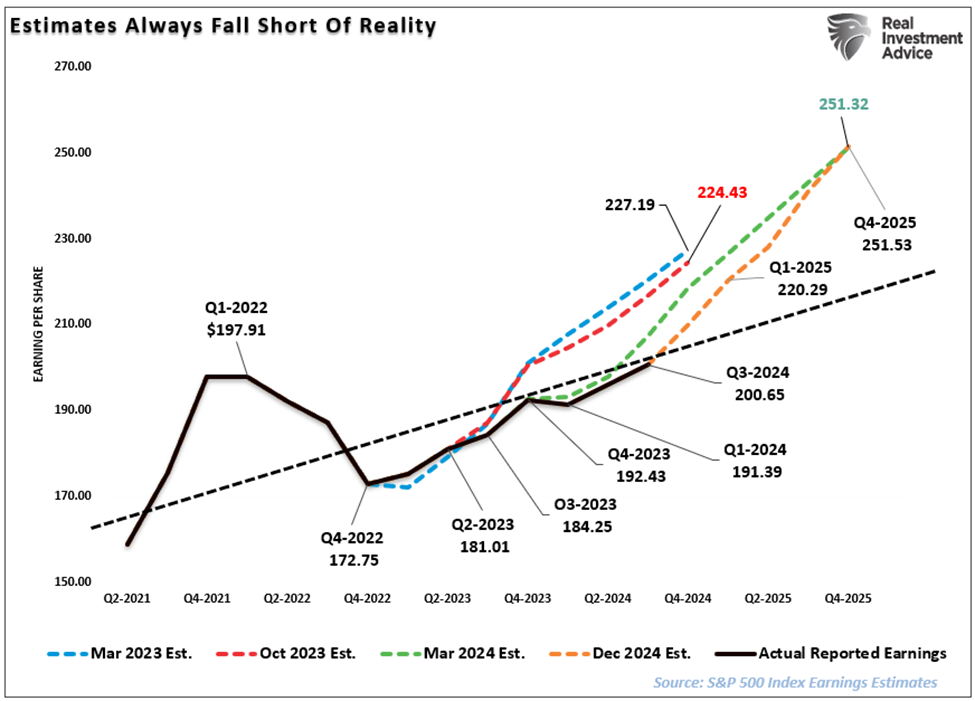

Whereas such is feasible, the chances are low, as sturdy financial progress can not exist in a low inflation and interest-rate setting. Extra notably, if the Fed cuts charges additional, as most economists and analysts anticipate subsequent 12 months, such will probably be in response to a slowing financial setting or monetary stress. Such wouldn’t help extra optimistic earnings estimates of $251 per share subsequent 12 months. This represents roughly a 19% improve from This fall-2024 ranges. (In 2023, estimates for 2024 recommended a 14% improve, which was simply 9%. The long-term pattern of earnings progress from 1900 to the current is simply 7.7%).”

Whereas the bullish predictions for subsequent 12 months are actually attainable, that consequence faces many challenges. That is significantly true on condition that the market trades at pretty lofty valuations. Even in a “gentle touchdown” setting, earnings ought to weaken, which makes present valuations at 27x earnings tougher to maintain. Subsequently, assuming earnings decline towards their long-term pattern, that might counsel present estimates fall to $220/share by the top of 2025. This considerably modifications the outlook for shares.

{kind=link}

Comply with The Guidelines

Wanting again at 2024, it was actually a really bullish 12 months.

I don’t know how 2025 will end up.

Nevertheless, I’m sufficiently old to know that each one good issues finally finish. As such, it solely appears prudent to mood expectations for returns subsequent 12 months and watch credit score spreads intently to find out when to cut back portfolio danger aggressively.

As we begin a brand new 12 months, it’s price repeating the principles that stored us out of bother final 12 months.

The Guidelines

- Reduce losers brief and let winners run. (Be a scale-up purchaser.)

- Set targets and be actionable. (With out particular targets, trades develop into arbitrary.)

- Emotionally pushed choices void the funding course of. (Purchase excessive/promote low)

- Comply with the pattern. (80% of portfolio efficiency is set by the long-term, month-to-month pattern. Whereas a “rising tide lifts all boats,” the alternative can be true.)

- By no means let a “buying and selling alternative” flip right into a long-term funding. (Consult with rule #1. All preliminary purchases are “trades” till your funding thesis is proved right.)

- An funding self-discipline doesn’t work if it’s not adopted.

- “Dropping cash” is a part of the funding course of. (If you’re not ready to take losses once they happen, you shouldn’t be investing.)

- The chances of success enhance considerably when the technical worth motion confirms the elemental evaluation. (This is applicable to each bull and bear markets)

- By no means, below any circumstances, add to a dropping place. (“Solely losers add to losers.” – Paul Tudor Jones)

- Markets are both “bullish” or “bearish.” Throughout a “bull market,” be solely lengthy or impartial. Throughout a “bear market,” be solely impartial or brief. (Bull and Bear markets are decided by their long-term pattern.)

- When markets are buying and selling at, or close to, extremes do the alternative of the “herd.”

- Do extra of what works and fewer of what doesn’t. (Conventional rebalancing takes cash from winners and provides it to losers. Rebalance by lowering losers and including to winners.)

- “Purchase” and “Promote” indicators are solely helpful if carried out. (Managing with out a “purchase/promote” self-discipline is designed to fail.)

- Attempt to be a .700 “at bat” participant. (No technique works 100% of the time. Be constant, management errors, and capitalize on alternatives to win.)

- Handle danger and volatility. (Management the variables that result in errors to generate returns as a byproduct.)

I sincerely want you a contented and affluent 2025.

Be happy to achieve out if you wish to navigate these unsure waters with knowledgeable steerage. Our crew makes a speciality of serving to purchasers make knowledgeable choices in as we speak’s unstable markets.

Have a fantastic week.

Analysis Report

Subscribe To “Earlier than The Bell” For Each day Buying and selling Updates

We’ve got arrange a separate channel JUST for our brief day by day market updates. Please subscribe to THIS CHANNEL to obtain day by day notifications earlier than the market opens.

Click on Right here And Then Click on The SUBSCRIBE Button

Subscribe To Our YouTube Channel To Get Notified Of All Our Movies

Bull Bear Report Market Statistics & Screens

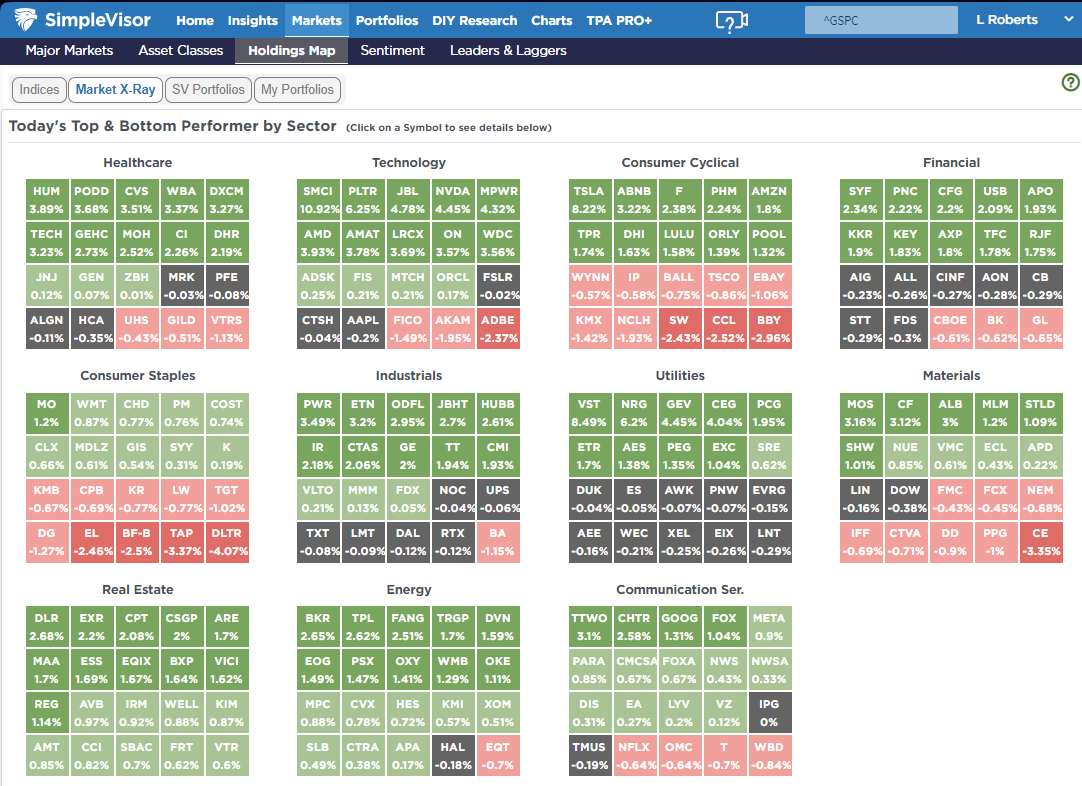

SimpleVisor Prime & Backside Performers By Sector

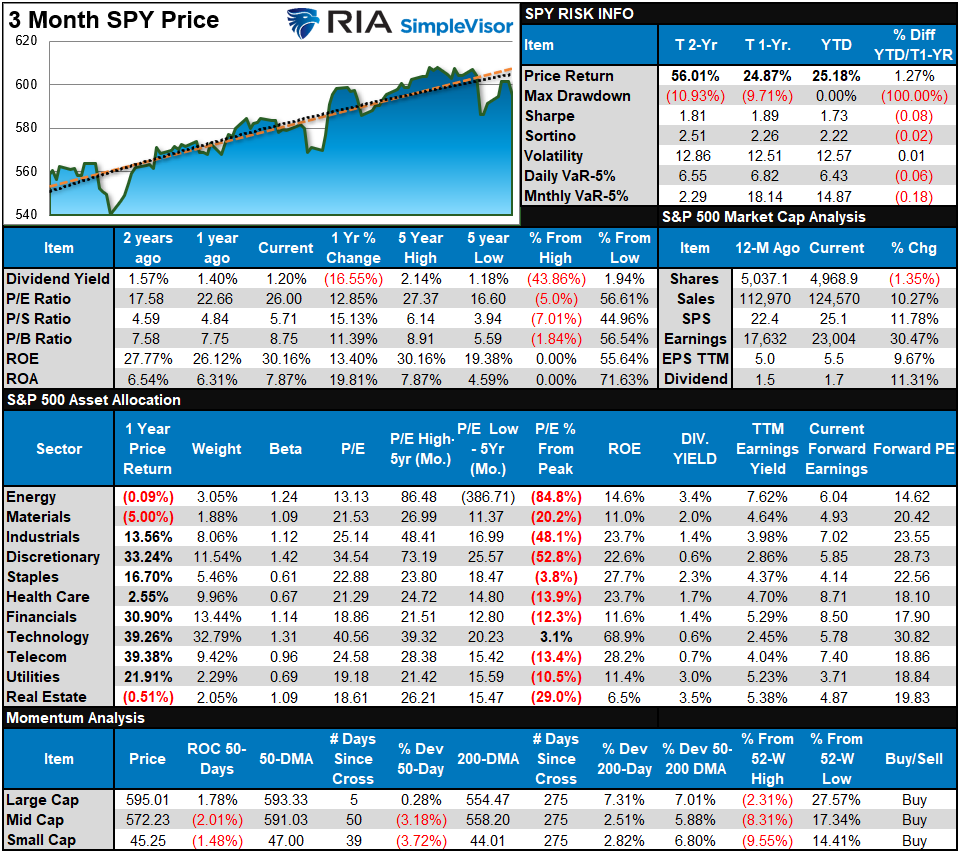

S&P 500 Weekly Tear Sheet

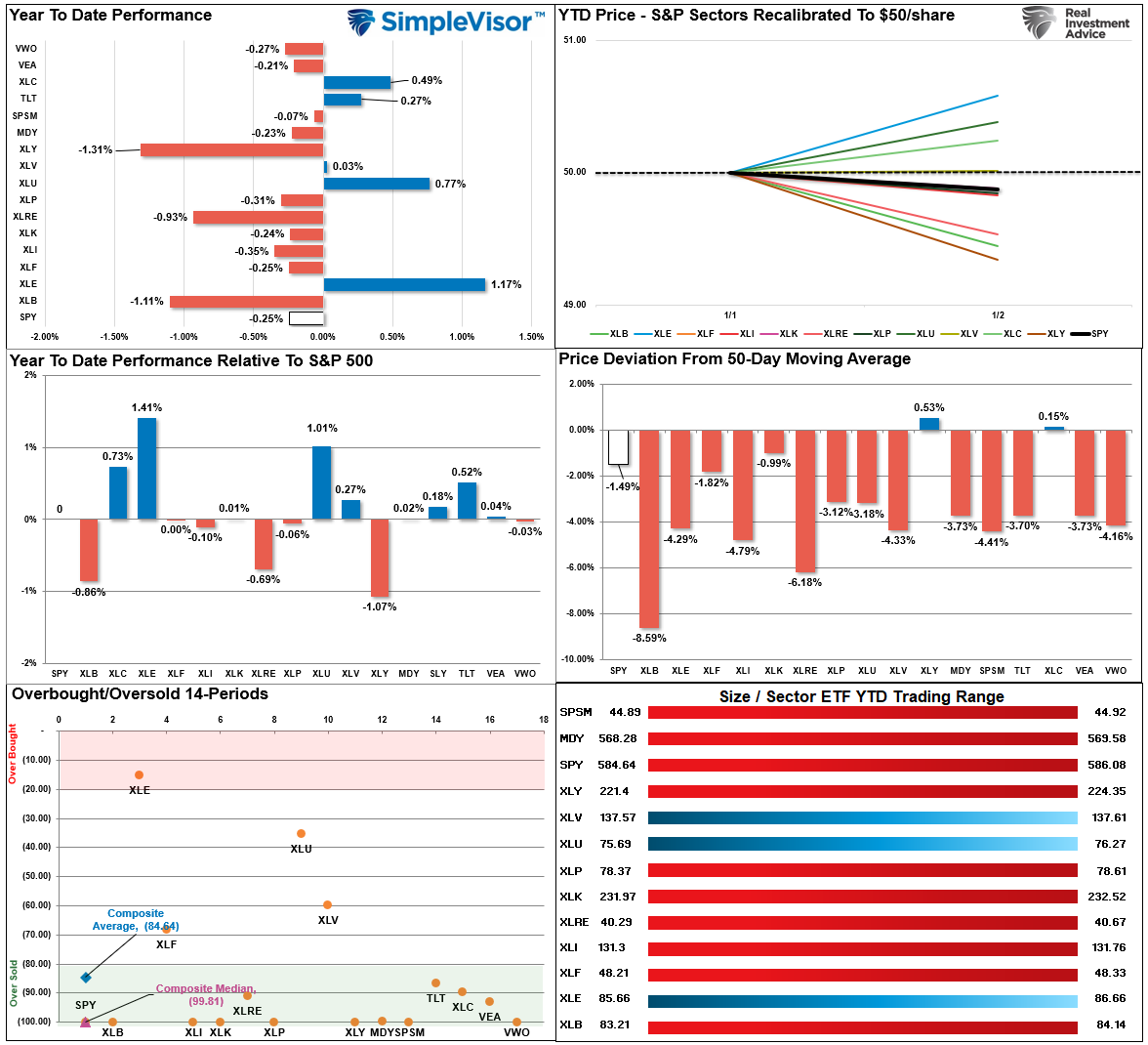

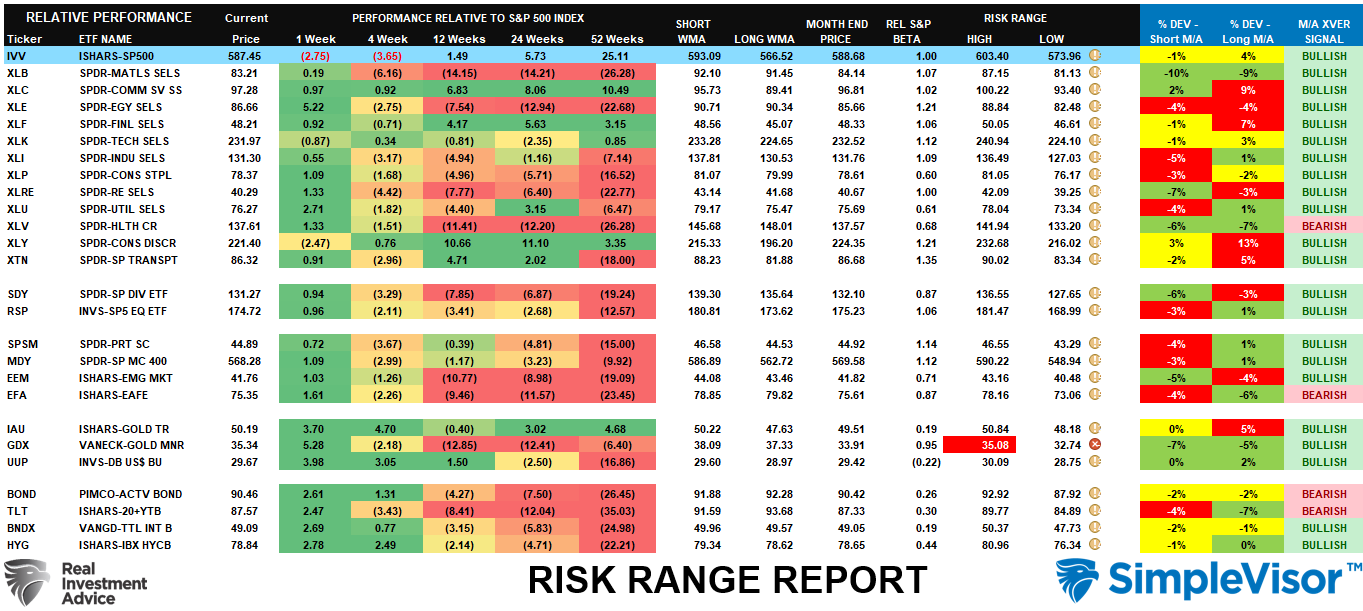

Relative Efficiency Evaluation

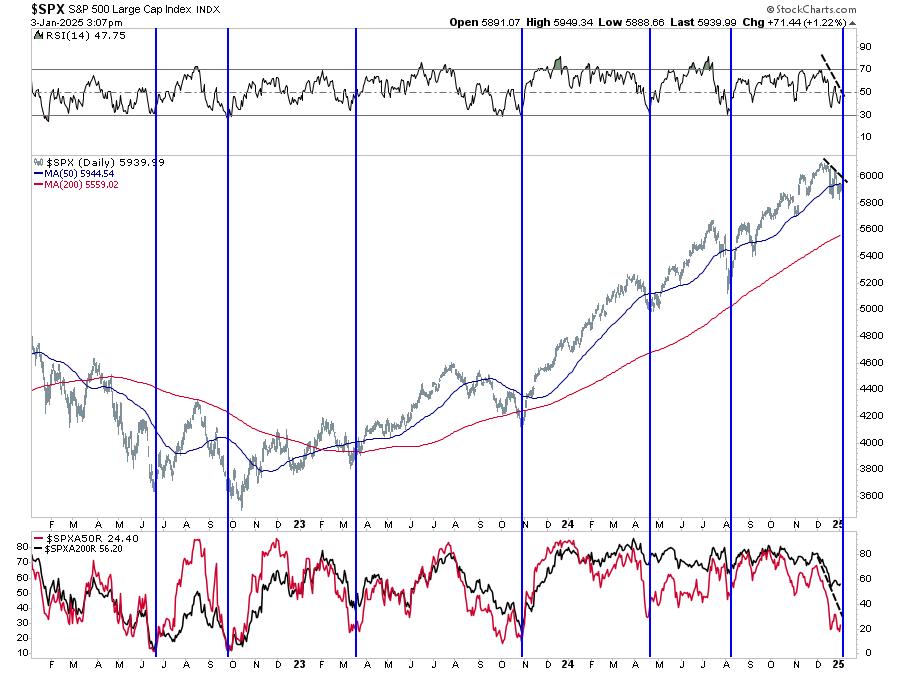

In final week’s e-newsletter, we famous that a lot of the rebalancing course of occurred as anticipated, and now the market is generally oversold. That remained the case this previous week. With 2024 behind us, we start monitoring relative market efficiency as soon as once more. It’s too early to make any assessments concerning the market with solely two days of buying and selling within the books, however over the following few weeks, we must always start to see early tendencies emerge. With markets at present oversold, search for the rally that began on Friday to proceed into subsequent week.

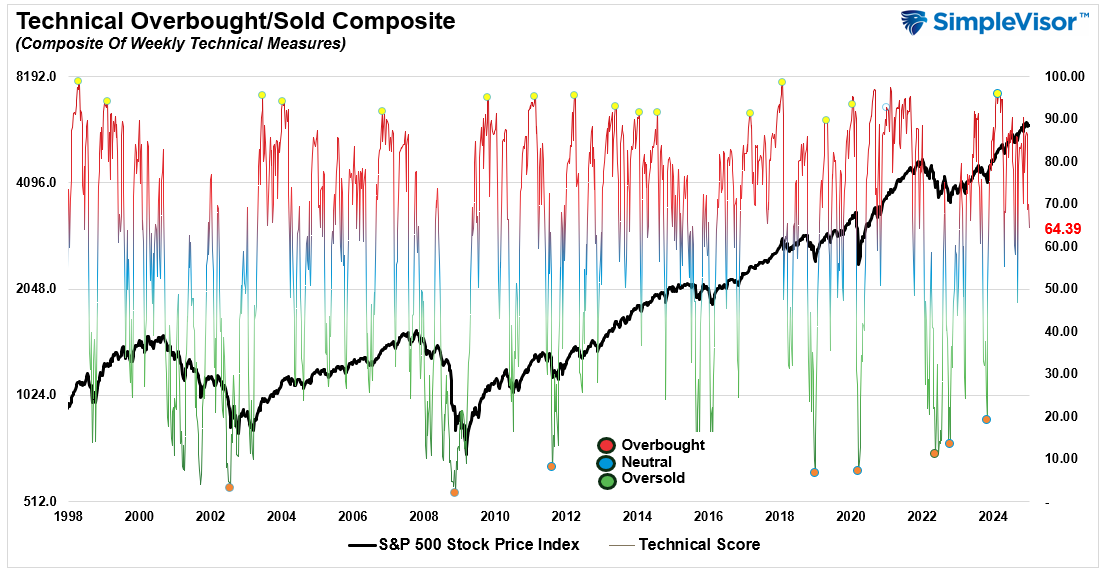

Technical Composite

The technical overbought/offered gauge includes a number of worth indicators (R.S.I., Williams %R, and so forth.), measured utilizing “weekly” closing worth knowledge. Readings above “80” are thought of overbought, and under “20” are oversold. The market peaks when these readings are 80 or above, suggesting prudent profit-taking and danger administration. The perfect shopping for alternatives exist when these readings are 20 or under.

The present studying is 64.39 out of a attainable 100.

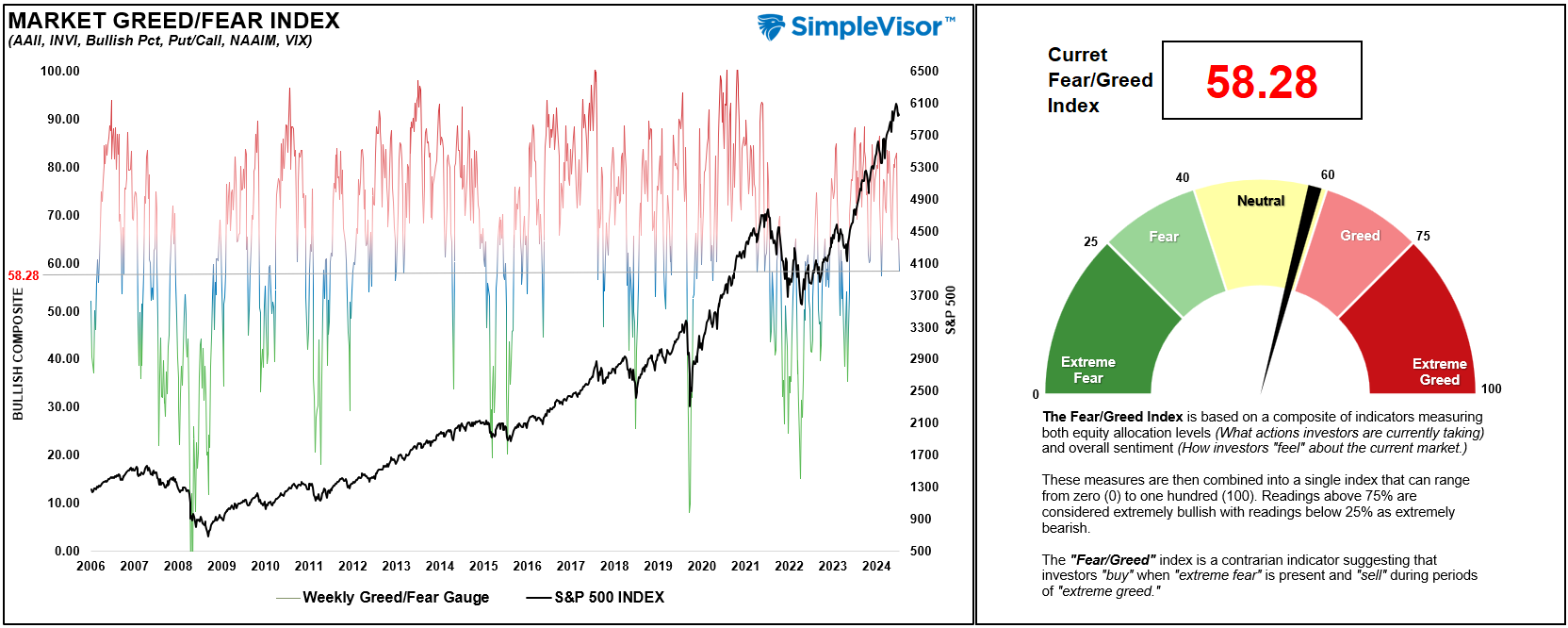

Portfolio Positioning “Worry / Greed” Gauge

The “Worry/Greed” gauge is how particular person {and professional} buyers are “positioning” themselves available in the market primarily based on their fairness publicity. From a contrarian place, the upper the allocation to equities, the extra seemingly the market is nearer to a correction than not. The gauge makes use of weekly closing knowledge.

NOTE: The Worry/Greed Index measures danger from 0 to 100. It’s a rarity that it reaches ranges above 90. The present studying is 58.28 out of a attainable 100.

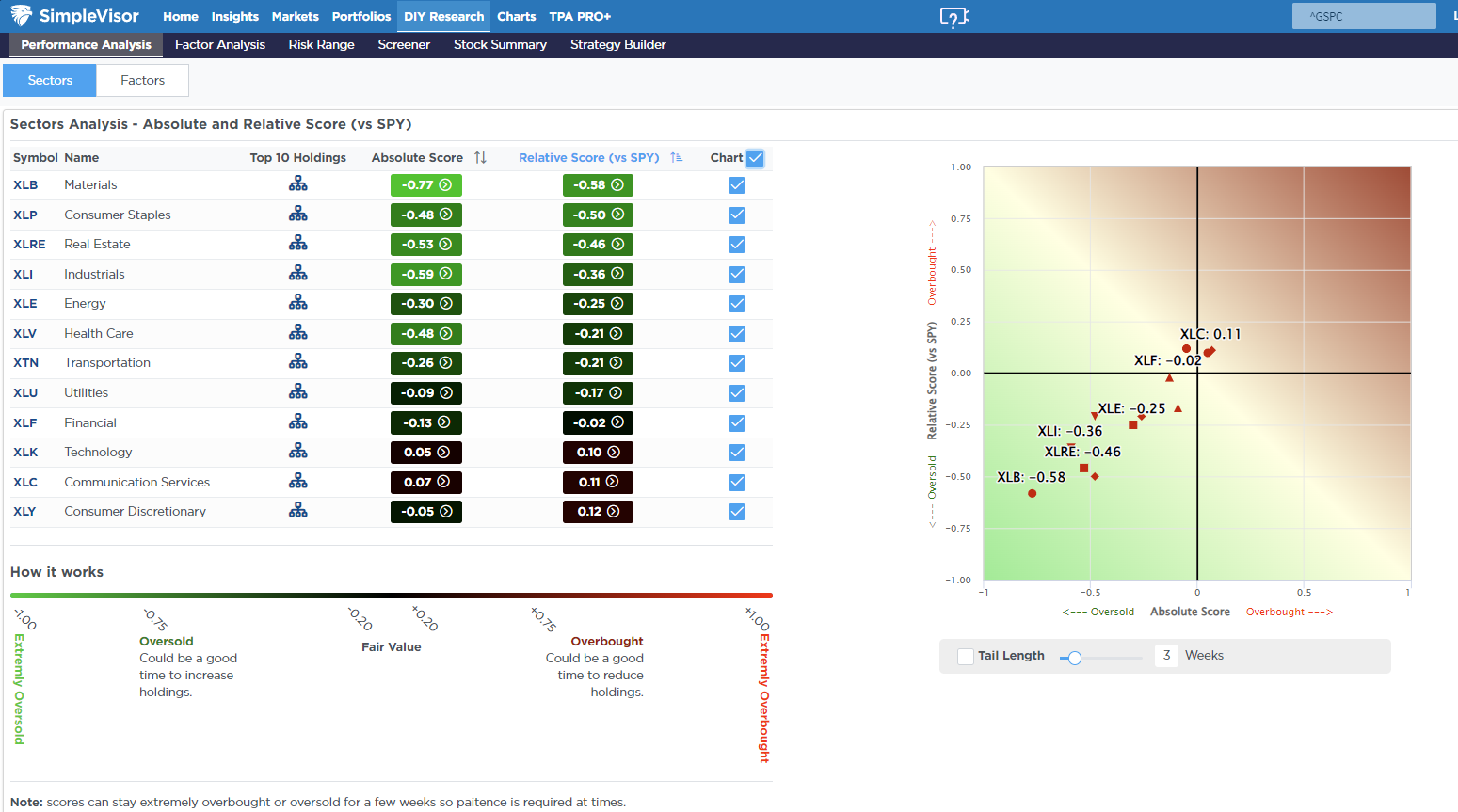

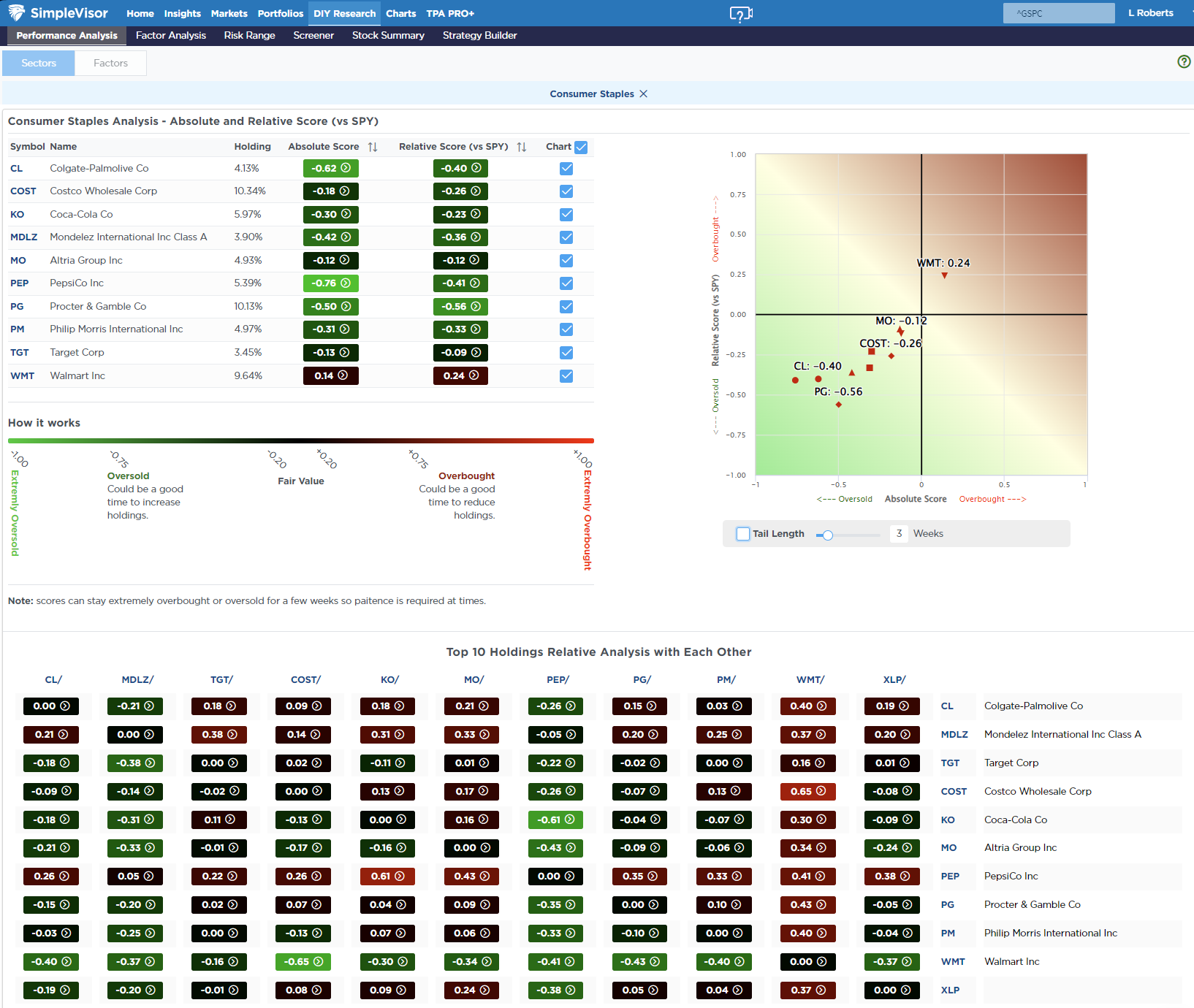

Relative Sector Evaluation

Most Oversold Sector Evaluation

Sector Mannequin Evaluation & Threat Ranges

How To Learn This Desk

- The desk compares the relative efficiency of every sector and market to the S&P 500 index.

- “MA XVER” (Shifting Common Crossover) is set by the short-term weekly transferring common crossing positively or negatively with the long-term weekly transferring common.

- The danger vary is a operate of the month-end closing worth and the “beta” of the sector or market. (Ranges reset on the first of every month)

- The desk exhibits the worth deviation above and under the weekly transferring averages.

With solely two buying and selling days into the brand new 12 months, there’s inadequate knowledge to calculate every sector’s and market danger ranges. We are going to replace the evaluation in full subsequent week.

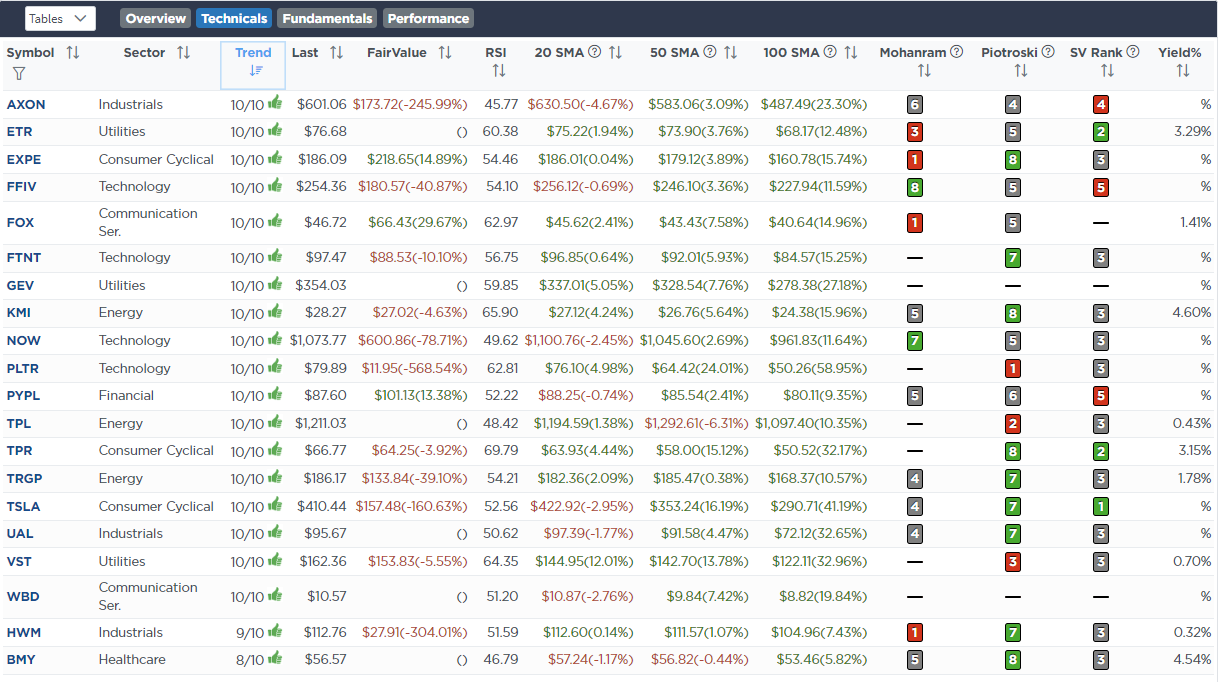

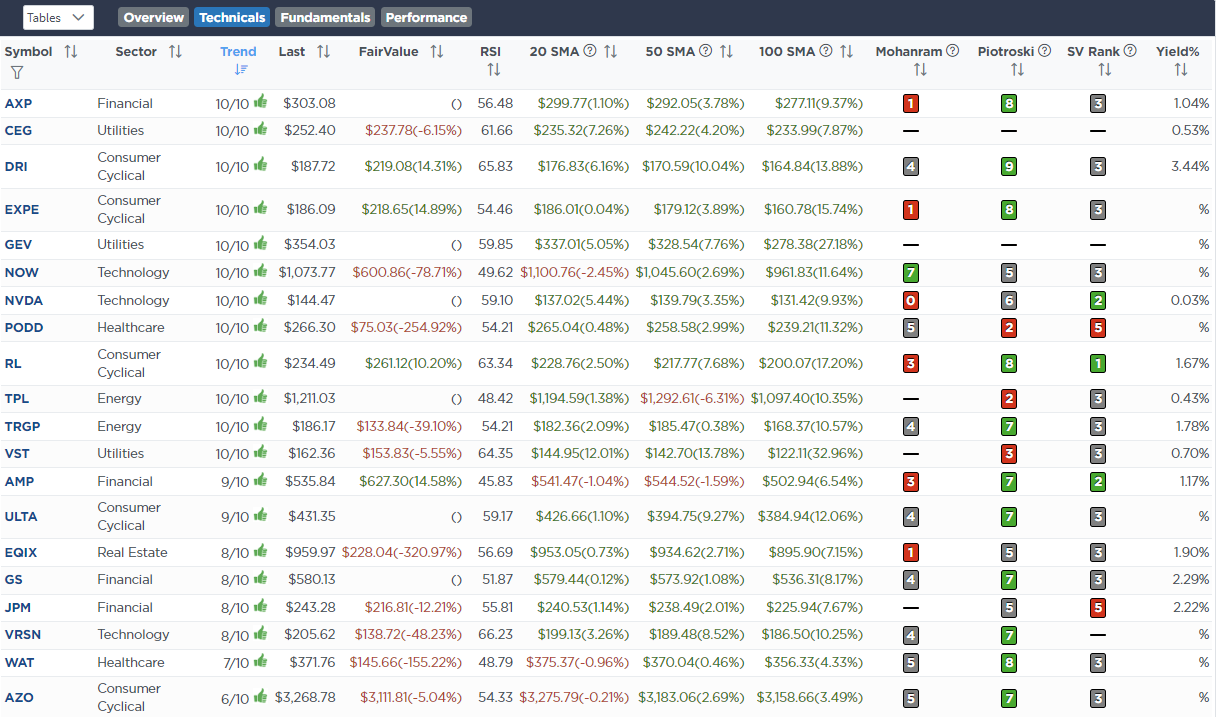

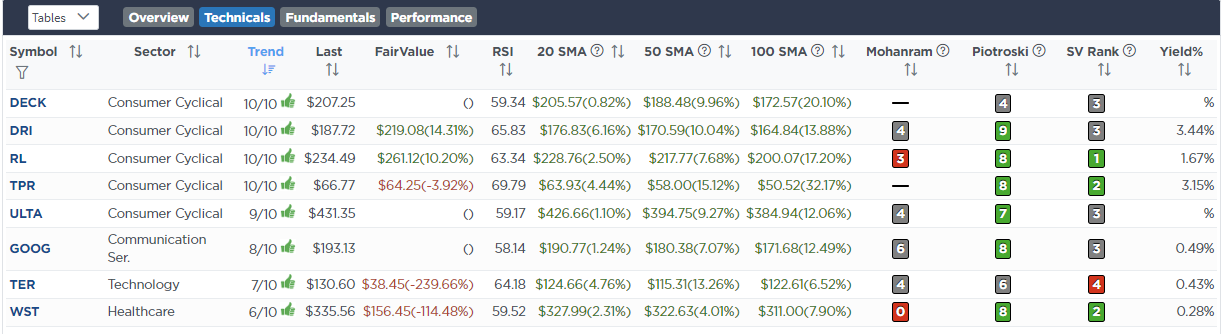

Weekly SimpleVisor Inventory Screens

We offer three inventory screens every week from SimpleVisor.

This week, we’re trying to find the Prime 20:

- Relative Energy Shares

- Momentum Shares

- Elementary & Technical Energy W/ Dividends

(Click on Photographs To Enlarge)

RSI Display

Momentum Display

Elementary & Technical Display

SimpleVisor Portfolio Adjustments

We put up all of our portfolio modifications as they happen at SimpleVisor:

No Trades This Week

Lance Roberts, C.I.O., RIA Advisors

Have a contented, secure, and affluent New 12 months.