{kind=link}

Quite a few reader requests following our article, Company REITs For A Bull Steepener, prompted us to jot down this follow-up with extra element about easy methods to analyze company REITs. This text doesn’t suggest particular company REITs, but it surely does lay out a number of the elementary fundamentals of the biggest publicly traded company REITs. In doing so, this evaluation and the prior article present a stable basis for additional evaluating company REITs.

Earlier than diving in, it’s price noting that the majority company REITs provide most popular shares. Whereas we don’t talk about them on this article, most popular shares may show rewarding and fewer dangerous within the present bull-steepening rate of interest atmosphere.

(Disclosure: RIA Advisors has a place in NLY and REM in its shopper portfolios.)

Managing A REIT

An company REIT is simply nearly as good as its portfolio administration group. As we wrote in Company REITs For A Bull Steepener, the portfolio administration group has to purchase rewarding belongings and concern acceptable liabilities to fund the investments, but it surely should additionally continually hedge the portfolio for rate of interest and mortgage unfold danger. Moreover, they actively commerce derivatives to remodel the phrases and circumstances of their liabilities.

As a result of leverage employed by the company REITs, a agency making poor hedging selections may very well be pressured to promote belongings or concern liabilities at inopportune occasions. Poor administration can lead to diminished or missed dividend funds.

Conversely, the prices of over-hedging can eat dearly into the REITs earnings, leading to minimal dividends. Discovering the fitting steadiness between belongings, liabilities, and hedges is a tall activity. The portfolio supervisor’s expertise in managing the portfolio could make a giant distinction in returns when evaluating REITs.

We can not quantify portfolio administration ability ranges, however we share info on every REIT that can assist you higher perceive some variations between the biggest company REITs.

Evaluating Company REITs

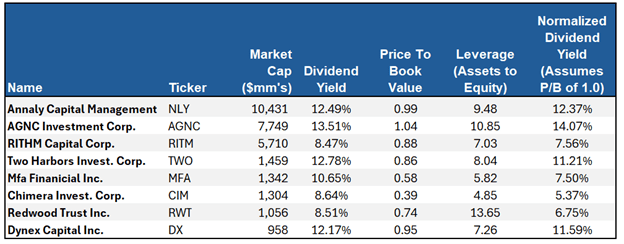

As a result of distinctive company REIT enterprise mannequin, analysis requires instruments totally different from these generally used for shares. Company REIT buyers favor metrics like value to ebook worth, leverage, rate of interest spreads, dividend reliability, and worth in danger. Earnings, gross sales, and conventional margin and valuation calculations aren’t as useful.

The next desk shares info on the highest publicly traded company REITs. Additional sections beneath give attention to three elements that assist decide danger and investor returns. The tables in these sections present the newest respective knowledge, the ten-year ranges, and the scale of the ranges to offer higher context for the present figures.

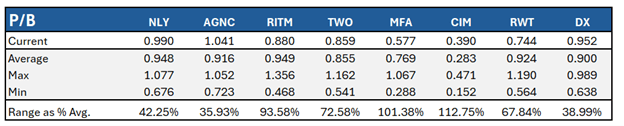

Value To Guide Worth

The value to ebook worth tells buyers how a lot portfolio worth or fairness (belongings minus liabilities) they personal per share. The ratio varies as a result of whims of buyers. Buyers ought to favor a price-to-book worth ratio beneath 1.0 as they basically purchase the portfolio for lower than 100% of its worth. Nevertheless, a price-to-book worth ratio nicely beneath 1.0 might point out bother.

As a result of risky nature of company REIT belongings, liabilities, and hedges, the ebook worth is in fixed movement. Sadly, most company REITs solely report the ebook worth quarterly. Accordingly, warning is warranted as a result of the ebook worth is at all times stale, whereas value modifications are present. In different phrases, there are solely 4 days a 12 months when the price-to-book worth ratio is right. There are methods to estimate ebook worth to assist overcome this downside.

Company REITs are incentivized to develop as a bigger portfolio creates extra earnings for the corporate executives and the portfolio administration group. Rising entails issuing extra fairness.

Company REITs usually provide new shares to the market when the price-to-book worth is above 1.0. Doing so permits them to boost more cash per share than the web portfolio worth. New issuance usually causes the inventory value to say no towards a price-to-book ratio of 1.0. When the price-to-book ratio is beneath 1.0, issuing shares shouldn’t be as economically useful to the REIT; nonetheless, it provides worth to current shareholders.

The desk beneath reveals the newest price-to-book worth of the eight largest publicly traded company REITs. Typically, these are about three months previous. Since bond yields fell over the previous few months and the unfold of mortgages to liabilities tightened, the portfolio values are seemingly greater than final reported. That stated, many share costs of the shares additionally elevated in worth.

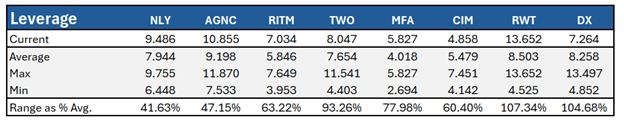

Leverage

To higher respect the significance of leverage, we share the next simplified abstract of the creation of an company REIT. It’s from Company REITs For A Bull Steepener.

Hypothetically, let’s begin a brand new company REIT that can assist you respect how they function.

- We solicit $1 billion from fairness buyers.

- A good portion of the $1 billion is used to purchase mortgage-backed securities (MBS).

- We then borrow $4 billion from a financial institution utilizing the $1 billion of MBS as collateral.

- The proceeds from the $4 billion mortgage are additionally used to buy MBS.

- Our new REIT has about $5 billion of MBS towards $1 billion of fairness and $4 billion of debt.

- Consequently, the REIT has 5x leverage.

The quantity of leverage is a necessary gauge of danger. If, within the instance above, the REIT borrowed $50 billion with solely $1 billion of fairness, leading to 50x leverage. A 2% antagonistic transfer within the portfolio would wipe out your entire fairness worth. Conversely, 5x leverage takes a 20% loss earlier than fairness holders are worn out.

Not solely is the quantity of leverage important to trace, however how and when the leverage modifications will help us gauge the portfolio supervisor’s stance towards current dangers. Additionally of equal significance to these gauging danger is the hedging exercise. Particularly, how is the portfolio administration group utilizing derivatives to remodel liabilities and handle danger?

Stable hedging expertise can partially offset the dangers of excessive leverage. Conversely, a REIT might have low leverage however nonetheless poses excessive danger as a consequence of poor hedges.

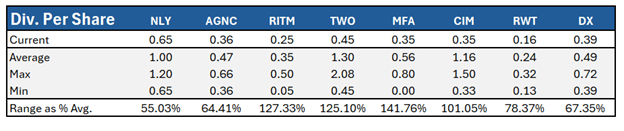

Dividend Reliability

Given the outsized dividend yields on company REITs, the reliability of the REIT’s dividend is essential. Like different key metrics, we should always evaluate the present dividend to its historic vary to understand the way it can doubtlessly change in favorable or antagonistic environments.

An Company REIT Various

In case you are uncomfortable selecting particular company REITs, we suggest diversifying amongst many to cut back idiosyncratic portfolio dangers.

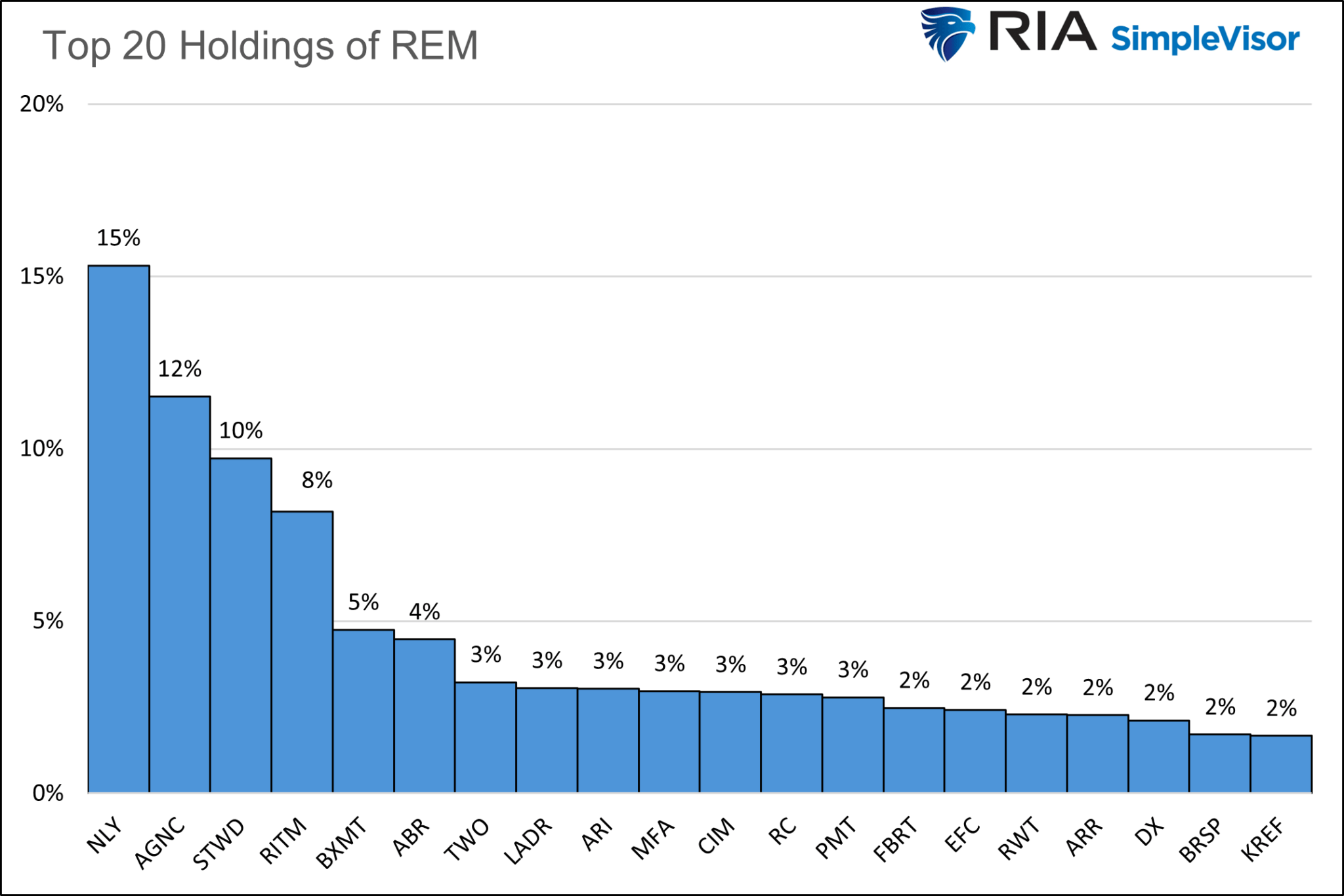

A technique is through the iShares Mortgage Actual ETF (REM). The ETF’s two largest holdings, accounting for over 25%, are NLY and AGNC. Keep in mind a few of its holdings aren’t company REITs. Accordingly, they might comprise belongings that the federal government doesn’t assure.

Abstract

And not using a background in managing a portfolio of mortgages, analyzing company REITs might be difficult. Nevertheless, placing in additional homework than is typical for a inventory funding can present buyers with returns usually uncorrelated with the broader market, thus providing a novel type of diversification. If you happen to resolve to analysis company REITs, we extremely suggest you learn their quarterly and annual experiences, that are extremely detailed and insightful.

Company REITs aren’t for buy-and-hold buyers. They have an inclination to carry out nicely in particular financial and rate of interest environments and poorly in others. We consider the present bullish steepening shift within the yield curve might provide buyers alternatives with the company REIT sector. Nevertheless, we stress REIT portfolios can achieve worth whereas its shares lose worth.

Michael Lebowitz, CFA is an Funding Analyst and Portfolio Supervisor for RIA Advisors. specializing in macroeconomic analysis, valuations, asset allocation, and danger administration. RIA Contributing Editor and Analysis Director. CFA is an Funding Analyst and Portfolio Supervisor; Co-founder of 720 World Analysis.

Observe Michael on Twitter or go to 720global.com for extra analysis and evaluation.

Buyer Relationship Abstract (Kind CRS)

Put up Views: 88

2024/10/09