{kind=link}

Wall Road analysts proceed considerably decreasing the earnings bar as we enter the Q2 reporting interval. Whilst analysts decrease that earnings bar, shares have rallied sharply over the previous few months.

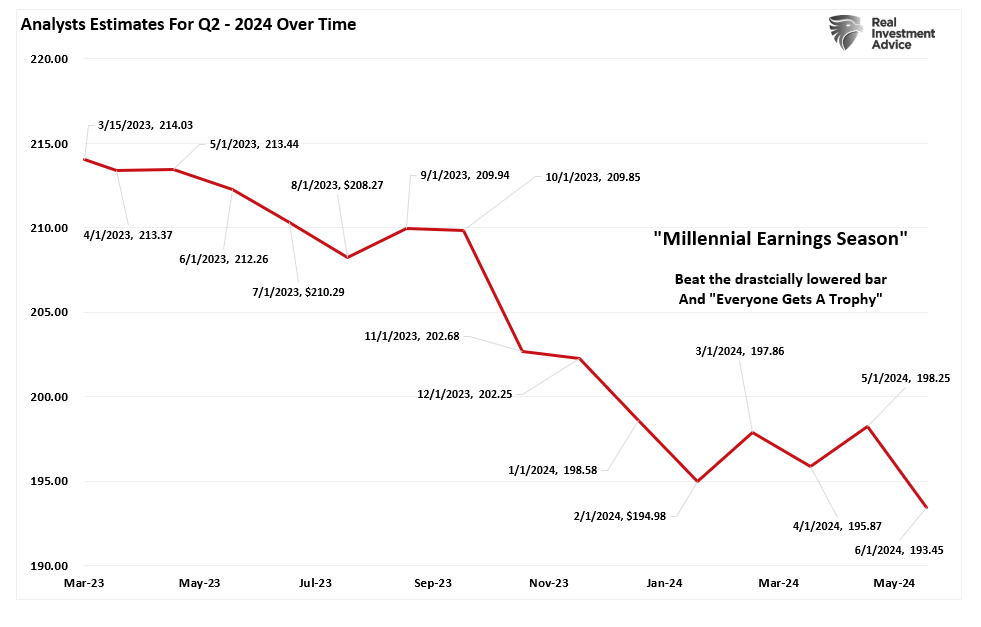

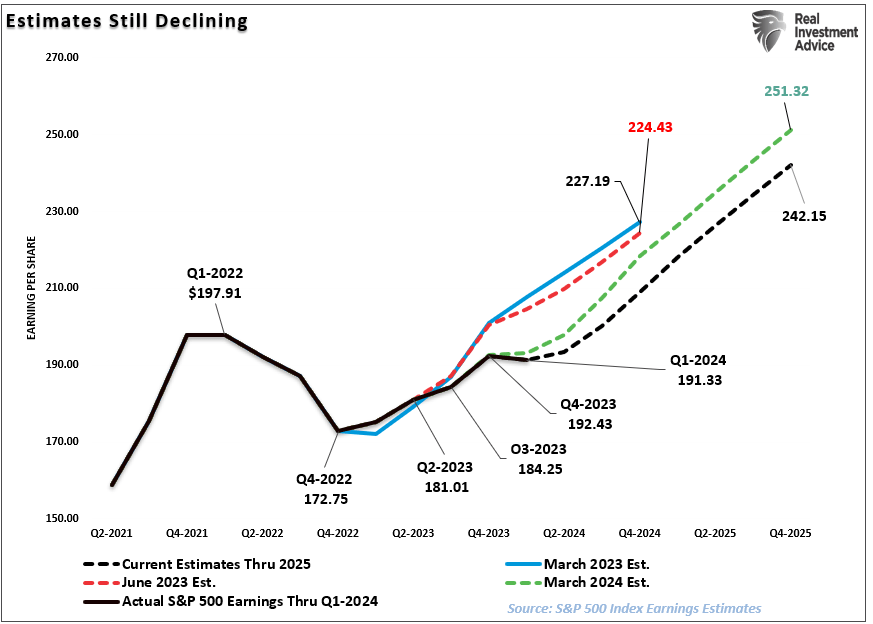

As we now have mentioned beforehand, it will likely be unsurprising that we are going to see a excessive share of corporations “beat” Wall Road estimates. In fact, the excessive beat charge is all the time the case because of the sharp downward revisions in analysts’ estimates because the reporting interval begins. The chart beneath exhibits the adjustments for the Q2 earnings interval from when analysts supplied their first estimates in March 2023. Analysts have slashed estimates over the past 30 days, dropping estimates by roughly $5/share.

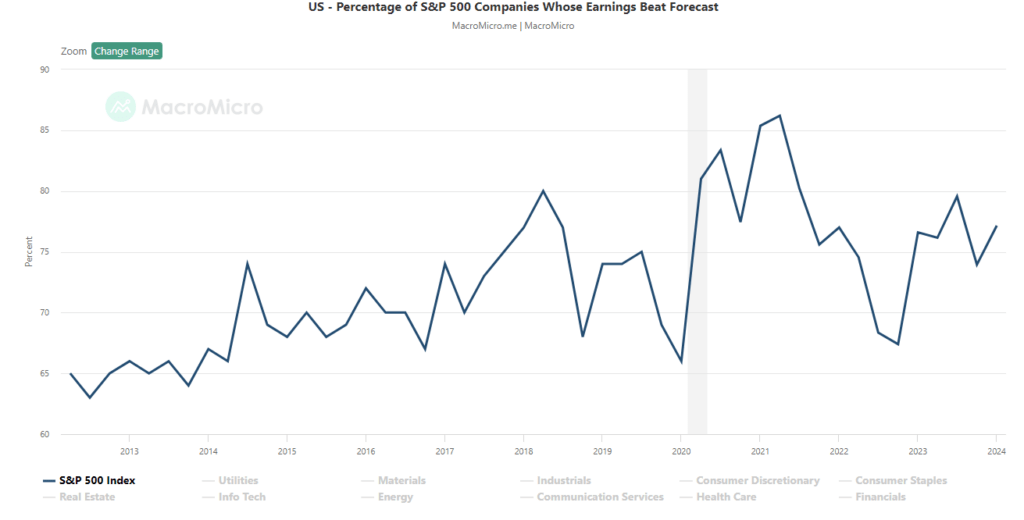

That’s the reason we name it “Millennial Earnings Season.” Wall Road constantly lowers estimates because the reporting interval approaches so “everybody will get a trophy.” A simple solution to see that is the variety of corporations beating estimates every quarter, no matter financial and monetary situations. Since 2000, roughly 70% of corporations often beat estimates by 5%, however since 2017, that common has risen to roughly 75%. Once more, that “beat charge” could be considerably decrease if buyers held analysts to their authentic estimates.

Analysts stay optimistic about earnings even with financial development weakening, inflation remaining elevated, and liquidity declining. Nonetheless, regardless of the decline in Q2 earnings estimates, analysts nonetheless imagine that the primary quarter of 2023 marked the underside for the earnings decline. Once more, that is regardless of the Fed charge hikes and tighter financial institution lending requirements that can act to gradual financial development.

Nonetheless, between March and June of this yr, analysts reduce ahead expectations for 2025 by roughly $9/share.

Nonetheless, even with the earnings bar lowered going ahead, earnings estimates stay indifferent from the long-term development development.

As mentioned beforehand, financial development, from which corporations derive income and earnings, should additionally strongly develop for earnings to develop at such an anticipated tempo.

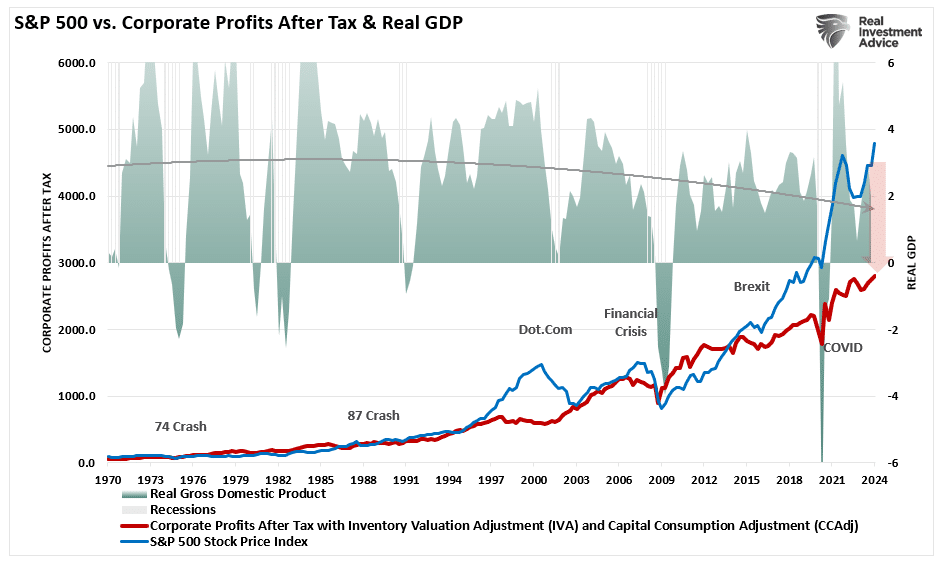

Since 1947, earnings per share have grown at 7.72%, whereas the financial system has expanded by 6.35% yearly. That shut relationship in development charges is logical, given the numerous function that client spending has within the GDP equation. Nonetheless, whereas nominal inventory costs have averaged 9.35% (together with dividends), reversions to underlying financial development will ultimately happen. Such is as a result of company earnings are a operate of consumptive spending, company investments, imports, and exports. The identical goes for company income, the place inventory costs have considerably deviated.

Such is important to buyers because of the coming impression on “valuations.”

Given present financial assessments from Wall Road to the Federal Reserve, robust development charges are unlikely. The info additionally recommend a reversion to the imply is completely doable.

The Reversion To The Imply

Following the pandemic-driven surge in financial coverage and a shuttering of the financial system, the financial system is slowly returning to regular. In fact, regular could appear very totally different in comparison with the financial exercise we now have witnessed over the past a number of years. Quite a few components at play assist the concept of weaker financial development charges and, subsequently, weaker earnings over the following few years.

- The financial system is returning to a gradual development surroundings with a threat of recession.

- Inflation is falling, which means much less pricing energy for firms.

- No synthetic stimulus to assist demand.

- Over the past three years, the pull ahead of consumption will now drag on future demand.

- Rates of interest stay considerably larger, impacting consumption.

- Customers have sharply diminished financial savings and better debt masses.

- Earlier stock droughts are actually surpluses.

Notably, this reversion of exercise will develop into exacerbated by the “void” created by pulling ahead consumption from future years.

“We have now beforehand famous an inherent drawback with ongoing financial interventions. Notably, the fiscal insurance policies applied put up the pandemic-driven financial shutdown created a surge in demand and unprecedented company earnings.”

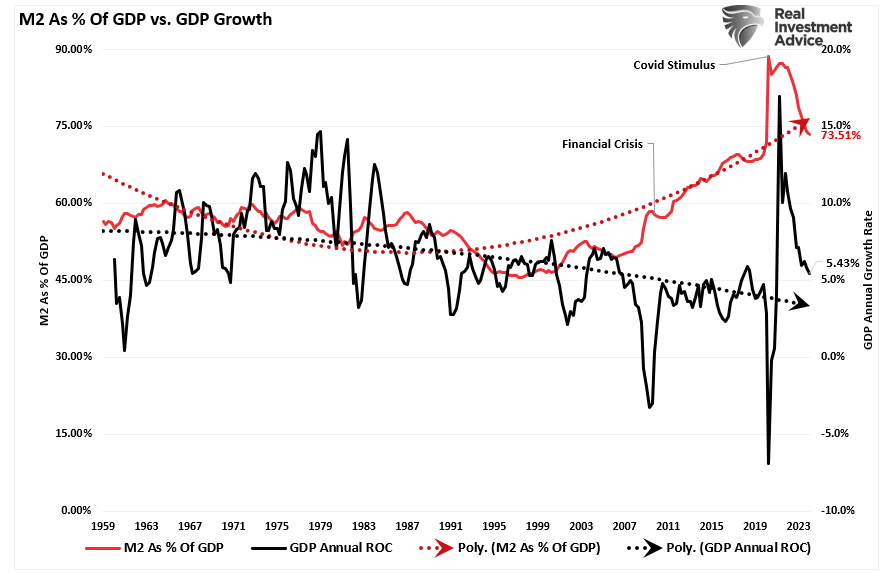

As proven beneath, the surge within the M2 cash provide is over. With out additional stimulus, financial development will revert to extra sustainable and decrease ranges.

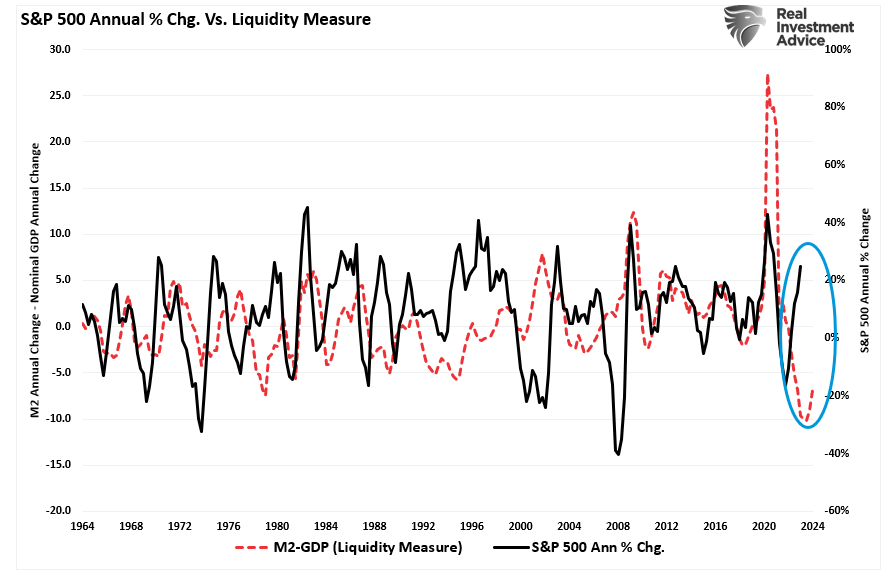

Whereas the media usually states that “shares usually are not the financial system,” as famous, financial exercise creates company revenues and earnings. As such, shares can’t develop sooner than the financial system over lengthy durations. An honest correlation exists between the enlargement and contraction of M2 much less GDP development (a measure of liquidity extra) and the annual charge of change within the S&P 500 index. At present, the deviation appears unsustainable. Extra notably, the present share annual change within the S&P 500 is approaching ranges which have preceded a reversal of that development charge.

So, both the annualized charge of return from the S&P 500 will decline resulting from repricing the marketplace for lower-than-expected earnings development charges, or the liquidity measure is about to show sharply larger.

Valuations Stay A Threat

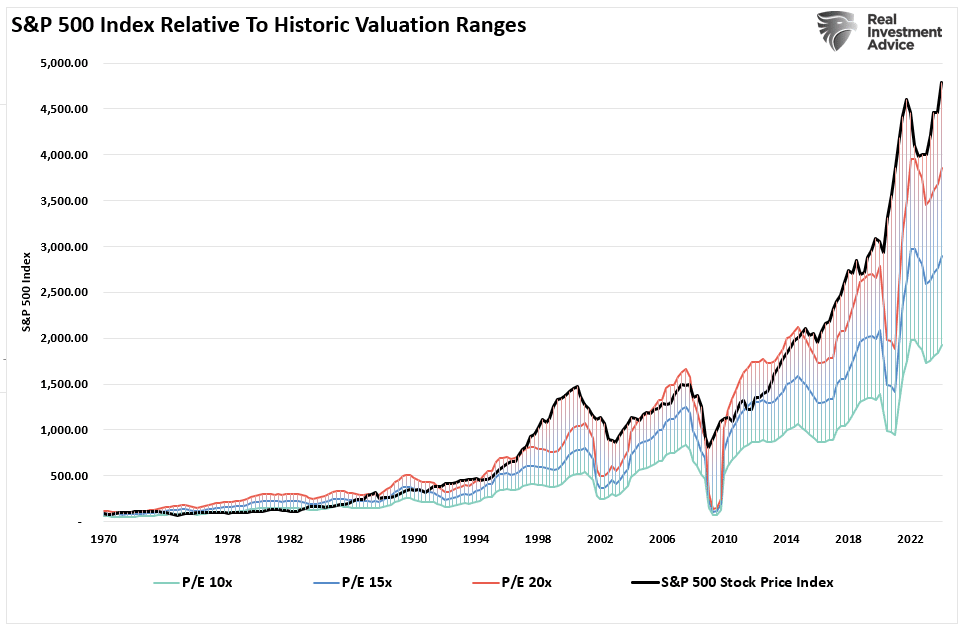

The issue with Wall Road constantly decreasing the earnings bar by decreasing ahead estimates ought to be apparent. Provided that Wall Road touts ahead earnings estimates, buyers overpay for investments. As ought to be apparent, overpaying for an funding as we speak results in decrease future returns.

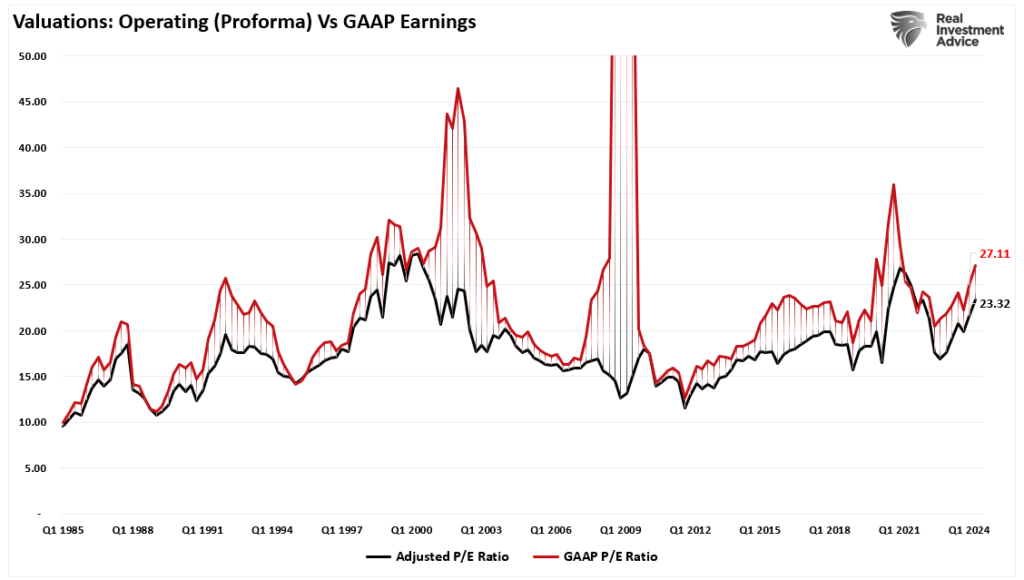

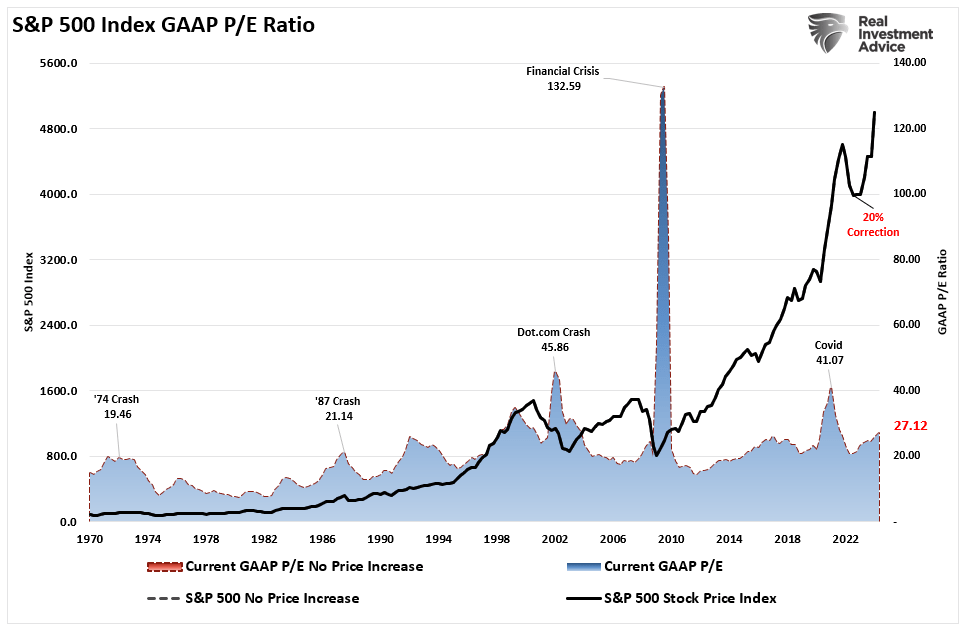

Even with the decline in earnings from the height, valuations stay traditionally costly on each a trailing and ahead foundation. (Discover the numerous divergences in valuations throughout recessionary durations as adjusted earnings do NOT replicate what is going on with precise earnings.)

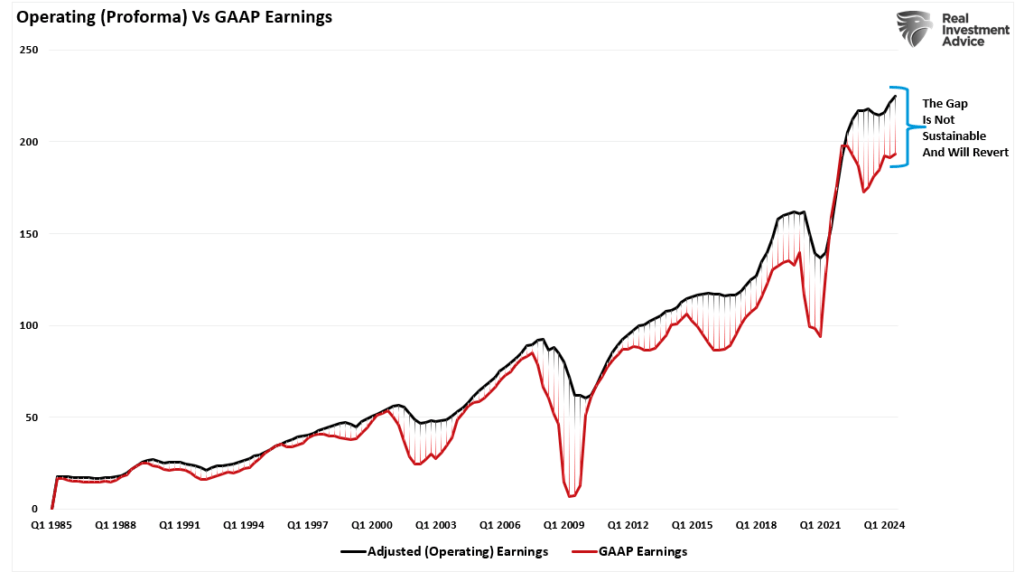

Most corporations report “working” earnings, which obfuscate profitability by excluding all of the “unhealthy stuff.” A major divergence exists between working (or adjusted) and GAAP earnings. When such a large hole exists, you will need to query the “high quality” of these earnings.

The chart beneath makes use of GAAP earnings. If we assume present earnings are appropriate, then such leaves the market buying and selling above 27x earnings. (That valuation stage stays close to earlier bull market peak valuations.)

Since markets are already buying and selling nicely above historic valuation ranges, this implies that outcomes will doubtless not be as “bullish” as many presently anticipate. Such is especially the case if extra financial lodging from the Federal Reserve and the Authorities are absent.

Trojan Horses

As all the time, the hope is that Q2 earnings and the complete coming yr’s stories will rise to justify the market’s overvaluation. Nonetheless, when earnings are rising, so are the markets.

Most significantly, analysts have a protracted and sordid historical past of being overly bullish on development expectations, which fall brief. Such is especially the case as we speak. A lot of the financial and earnings development was not natural. As an alternative, it was from the flood of stimulus into the financial system, which is now evaporating.

Overpaying for belongings has by no means labored out nicely for buyers.

With the Federal Reserve intent on slowing financial development to quell inflation, it’s only logical that earnings will decline. If so, costs should accommodate decrease earnings by decreasing present valuation multiples.

On the subject of analysts’ estimates, all the time stay cautious of “Greeks bearing presents.”

Put up Views: 2,672

2024/07/02