{kind=link}

Family fairness allocations are once more sharply rising, because the “Worry Of Lacking Out” or “F.O.M.O.” fuels a close to panic mentality to chase markets greater. As Michael Hartnett from Financial institution of America just lately famous:

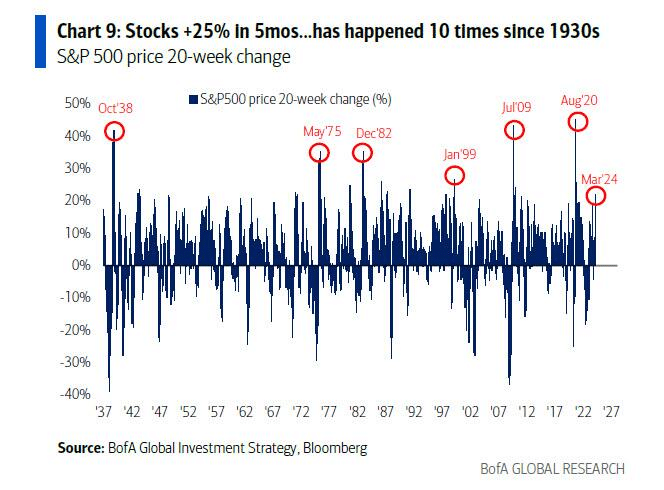

“Shares are up a ferocious +25% in 5 months, which has occurred simply 10 instances because the Nineteen Thirties. Usually, such surges happen from recession lows (1938, 1975, 1982, 2009, 2020), however, in fact, we didn’t have a recession in 2023, in line with the Biden administration. These surges additionally happen initially of bubbles (Jan’99).”

As mentioned within the latest Bull Bear Report, we will solely determine bubbles in hindsight. Such is the issue with attempting to “time” a market high, as they’ll final for much longer than logic would predict. George Soros defined this nicely in his idea of reflexivity.

“Monetary markets, removed from precisely reflecting all of the out there data, at all times present a distorted view of actuality. The diploma of distortion could differ infrequently. Generally it’s fairly insignificant, at different instances it’s fairly pronounced. When there’s a vital divergence between market costs and the underlying actuality, the markets are removed from equilibrium situations.“

Each bubble has two parts:

- An underlying development that prevails in actuality and;

- A false impression referring to that development.

“When optimistic suggestions develops between the development and the misunderstanding, a boom-bust course of will get set into movement. The method is liable to be examined by unfavorable suggestions alongside the way in which, and whether it is sturdy sufficient to outlive these checks, each the development and the misunderstanding get strengthened. Ultimately, market expectations change into up to now faraway from actuality that folks get compelled to acknowledge {that a} false impression is concerned. A twilight interval ensues throughout which doubts develop, and extra individuals lose religion, however the prevailing development will get sustained by inertia.” – George Soros

In simplistic phrases, Soros says that after the bubble inflates, it’ll stay inflated till some surprising, exogenous occasion causes a reversal within the underlying psychology. That reversal then reverses psychology from “exuberance” to “worry.”

What’s going to trigger that reversion in psychology? Nobody is aware of.

Nevertheless, the necessary lesson is that market tops and bubbles are a operate of “psychology.” The manifestation of that “psychology” manifests itself in asset costs and valuations that exceed financial progress charges.

As soon as once more, traders are piling into equities and “writing checks that the financial system can’t money.”

An Financial Underpinning

To know the issue, we should first notice from which capital good points are derived.

Capital good points from markets are primarily a operate of market capitalization, nominal financial progress, plus dividend yield. Utilizing John Hussman’s system, we will mathematically calculate returns over the following 10-year interval as follows:

(1+nominal GDP progress)*(regular market cap to GDP ratio / precise market cap to GDP ratio)^(1/10)-1

Due to this fact, IF we assume that GDP may keep 2% annualized progress sooner or later, with no recessions ever, AND IF present market cap/GDP stays flat at 2.0, AND IF the dividend yield stays at roughly 2%, we get ahead returns of:

(1.02)*(1.2/1.5)^(1/10)-1+.02 = -(1.08%)

However there are a “complete lotta ifs” in that assumption. Most significantly, we should additionally assume the Fed can get inflation to its 2% goal, cut back present rates of interest, and, as said, keep away from a recession over the following decade.

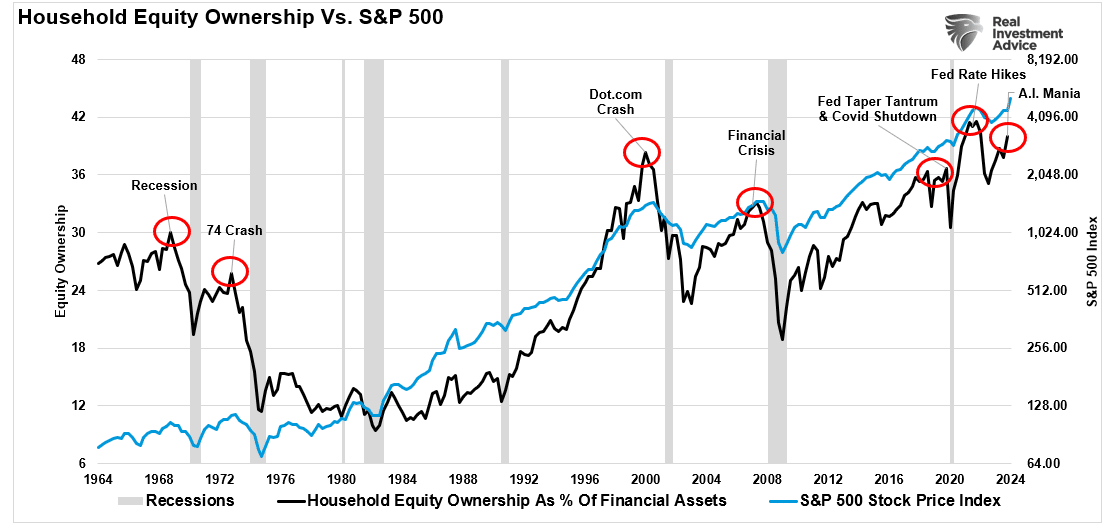

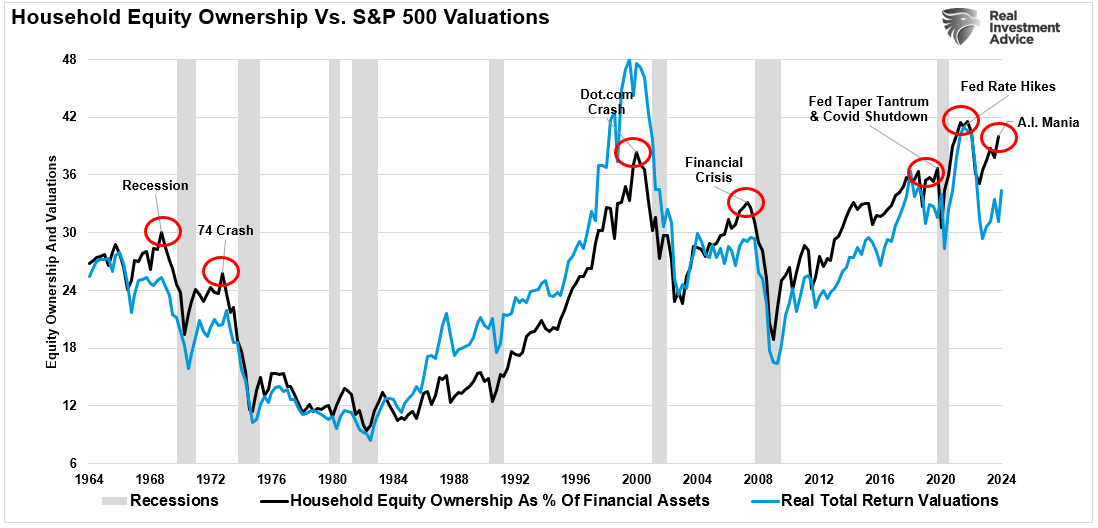

But, regardless of these important elementary components, retail traders once more throw warning to the wind. As proven, the present ranges of family fairness possession have reverted to near-record ranges. Traditionally, such exuberance has been the mark of extra necessary market cycle peaks.

If financial progress is reversed, the valuation discount will probably be fairly detrimental. Once more, such has been the case at earlier peaks the place expectations exceed financial realities.

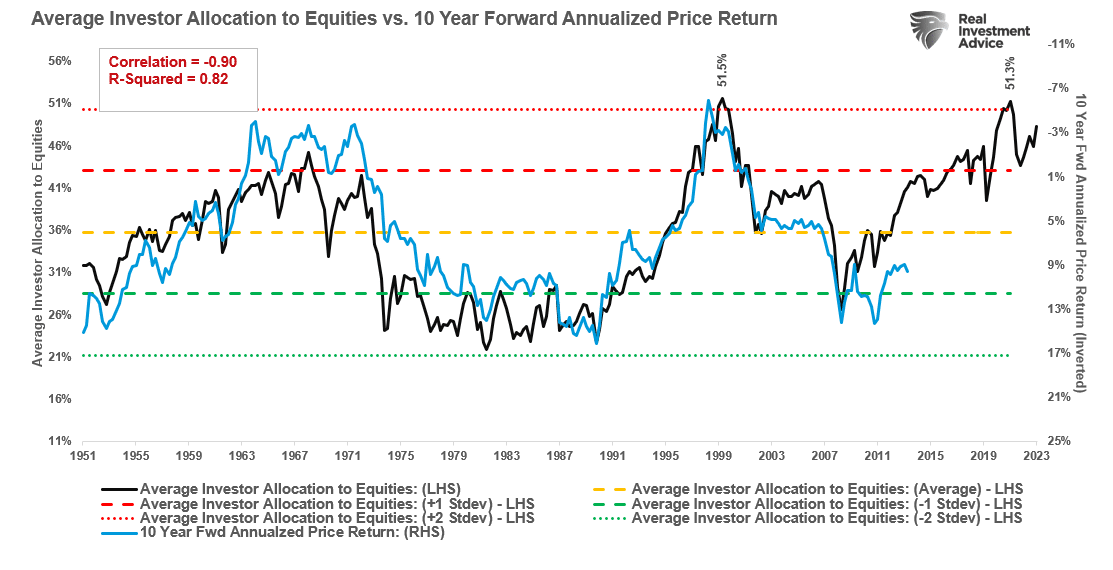

Bob Farrell as soon as quipped traders have a tendency to purchase essentially the most on the high and the least on the backside. Such is just the embodiment of investor conduct over time. Our colleague, Jim Colquitt, beforehand made an necessary remark.

“The graph beneath compares the typical investor allocation to equities to S&P 500 future 10-year returns. As we see, the info may be very nicely correlated, lending credence to Bob Farrell’s Rule #5. Notice the correlation statistics on the high left of the graph.”

The ten-year ahead returns are inverted on the appropriate scale. This means that future returns will revert towards zero over the following decade from present ranges of family fairness allocations by traders.

The reason being that when investor sentiment is extraordinarily bullish or bearish, such is the purpose the place reversals have occurred. As Sam Stovall, the funding strategist for Normal & Poor’s, as soon as said:

“If all people’s optimistic, who’s left to purchase? If all people’s pessimistic, who’s left to promote?”

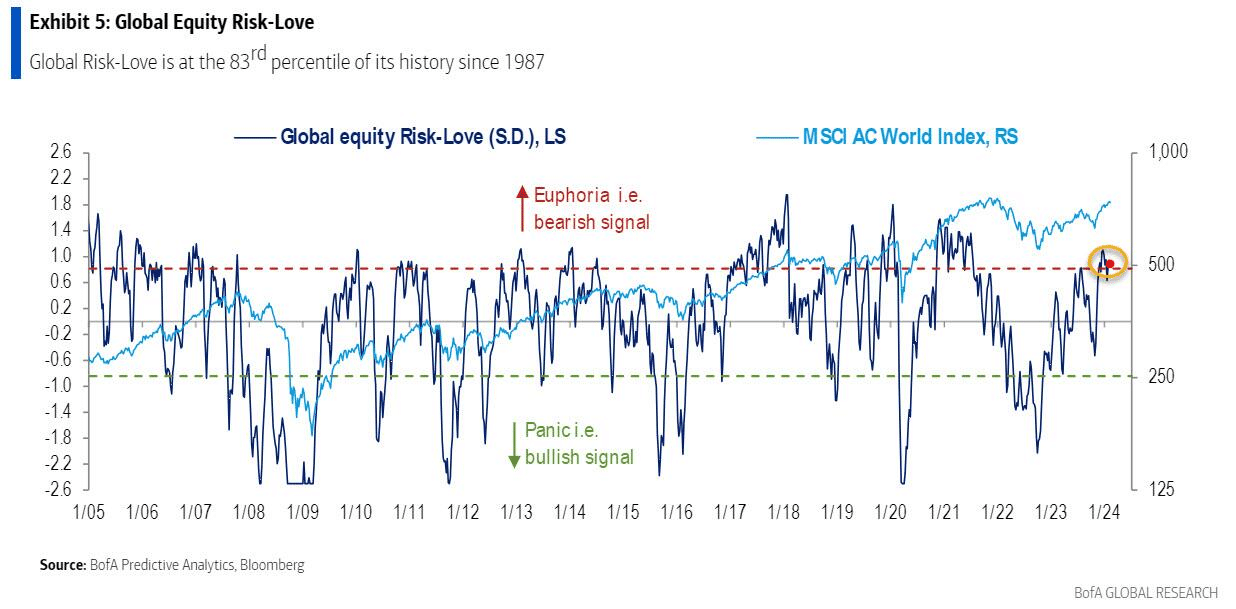

Everybody may be very optimistic in regards to the market. Financial institution of America, one of many world’s largest asset custodians, screens threat positioning throughout equities. At the moment, “threat love” is within the 83rd percentile and at ranges which have usually preceded short-term corrective actions.

The one query is what finally reverses that psychology.

A Disappointment Of Hopes

In January 2022, Jeremy Grantham made headlines along with his market outlook titled “Let The Wild Rumpus Start.” The crux of the article is summed up within the following paragraph.

“All 2-sigma fairness bubbles in developed international locations have damaged again to development. However earlier than they did, a handful went on to change into superbubbles of 3-sigma or larger: within the U.S. in 1929 and 2000 and in Japan in 1989. There have been additionally superbubbles in housing within the U.S. in 2006 and Japan in 1989. All 5 of those superbubbles corrected all the way in which again to development with a lot larger and longer ache than common.

Right this moment within the U.S. we’re within the fourth superbubble of the final hundred years.”

Whereas the market corrected in 2022, the reversion wanted to reverse the surplus deviation from the long-term progress traits was not achieved. Due to this fact, except the Federal Reverse is dedicated to a unending program of zero rates of interest and quantitative easing, the eventual reversion of returns to their long-term means stays inevitable.

Such will end in revenue margins and earnings returning to ranges that align with precise financial exercise. As Jeremy Grantham as soon as famous:

“Revenue margins are in all probability essentially the most mean-reverting sequence in finance. And if revenue margins don’t mean-revert, then one thing has gone badly unsuitable with capitalism. If excessive earnings don’t appeal to competitors, there’s something unsuitable with the system, and it isn’t functioning correctly.” – Jeremy Grantham

Traditionally, actual earnings have at all times finally reverted to underlying financial realities.

Many issues can go unsuitable within the months and quarters forward. Such is especially the case at a time when deficit spending is operating amok, and financial progress is slowing.

Whereas traders cling to the “hope” that the Fed has all the pieces below management, there’s a cheap probability they don’t.

The truth is that the following decade might be a disappointment to overly optimistic expectations.

Put up Views: 698

2024/03/15