{kind=link}

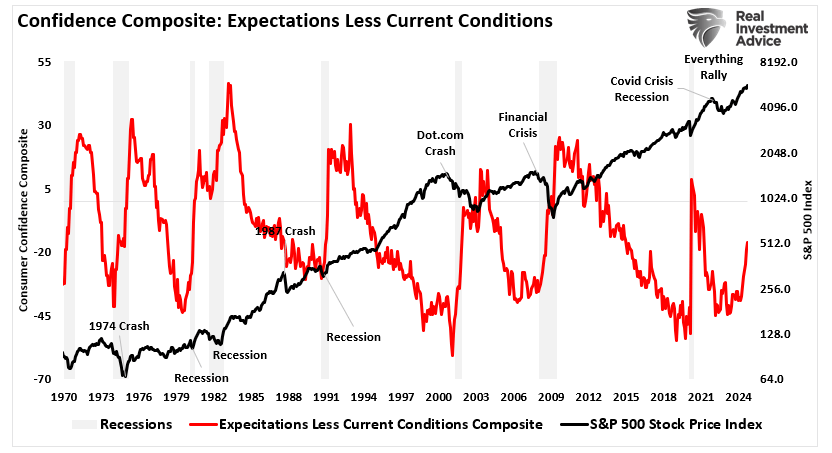

The Bureau of Financial Evaluation (BEA) not too long ago launched its second-quarter GDP report for 2024, showcasing a 2.96% progress fee. This quantity has sparked discussions amongst buyers and analysts, significantly these predicting an imminent recession. There are actually many supportive information factors which have traditionally predicted recessionary downturns. The reversal of the yield curve inversion, the 6-month fee of change within the main financial index, and most not too long ago, client confidence warn of a recessionary onset.

Nevertheless, regardless of these warning indicators, the U.S. economic system continues to point out resilience, defying many bearish forecasts. This text will discover the latest GDP report, the dangers to continued progress, and potential investing alternatives.

Defying Recession Calls: The Resilient U.S. Economic system

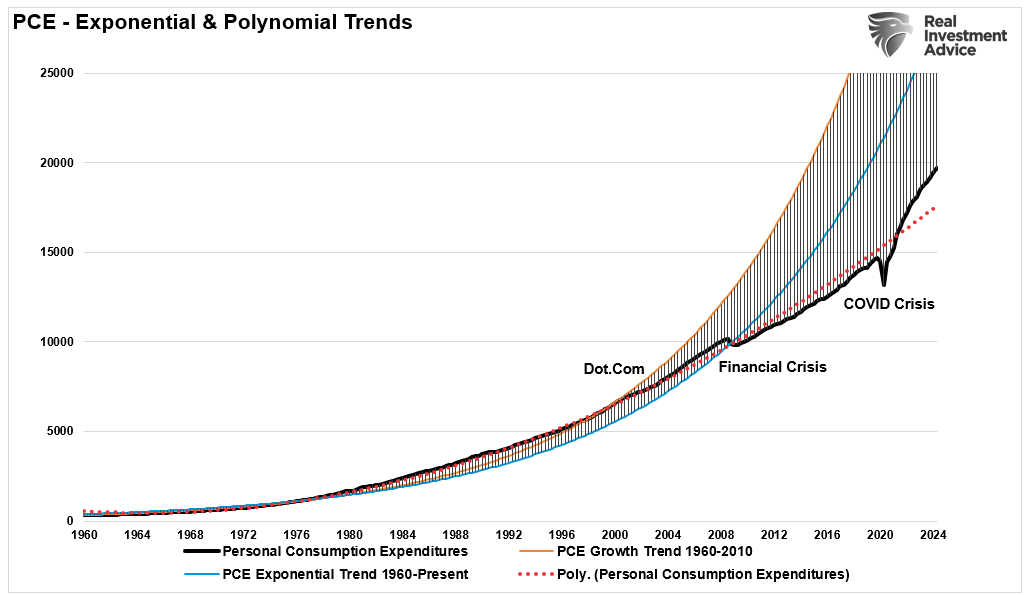

Quite a few market analysts have warned of an impending recession since early 2023, citing a number of elements: fast fee hikes by the Federal Reserve, excessive inflation, and rising geopolitical dangers. But, the Q2-2024 GDP progress of two.96% suggests the U.S. economic system is holding up higher than anticipated. That resilience is especially evident in client spending, which stays sturdy regardless of persistent inflation and better rates of interest. Presently, Private Consumption Expenditures (PCE), which contains about 70% of the GDP report, proceed to be properly above the polynomial progress development.

Given PCE’s somewhat important impression on the GDP report, a recession stays unlikely until spending slows markedly.

A number of elements of the GDP report spotlight the financial power that has caught many bearish forecasters off guard:

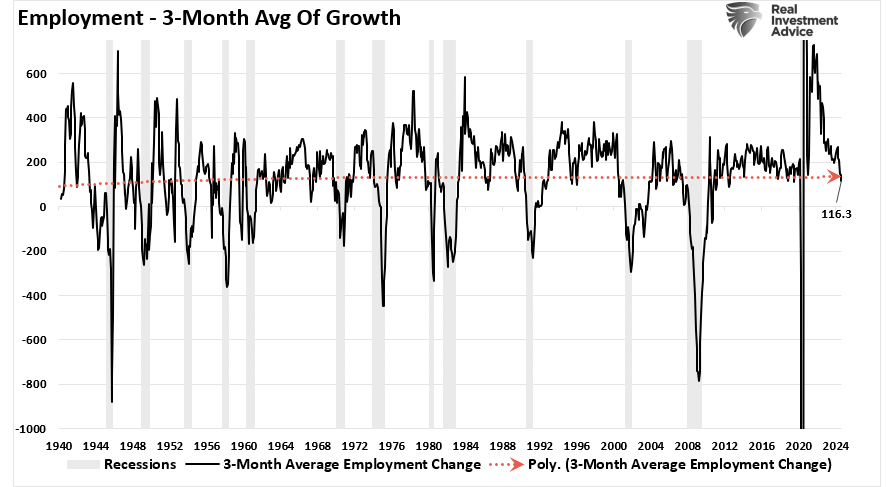

Moreover, the labor market stays supportive of financial progress. Sure, as proven, employment progress has slowed considerably following the “re-hiring” surge after the pandemic-related shutdown. Nevertheless, as demand within the economic system normalizes, employment progress is returning to its long-term progress development. The chart under reveals the 3-month common progress fee of hiring. As famous, employment progress has slowed however stays in progress mode. Till that 3-month common approaches zero job progress, the danger of a recession stays muted.

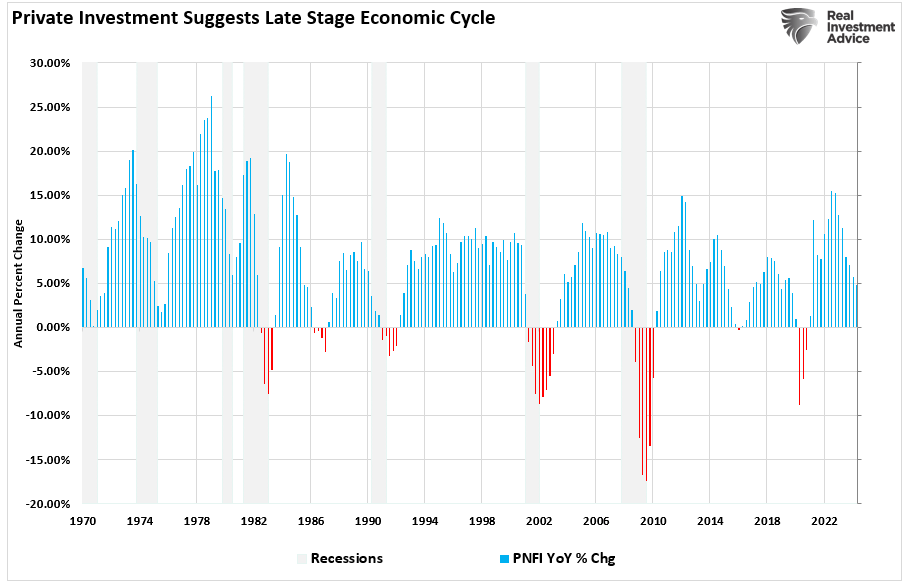

Lastly, enterprise funding, one other contributing issue to the GDP calculation, doesn’t help the recessionary expectations. Though enterprise funding has been considerably uneven and positively weaker following the post-pandemic surge, there are indicators that firms are nonetheless increasing. At almost 5% annualized, non-public funding is just not close to ranges usually related to an financial recession.

These parts, all a part of the final GDP report, counsel that predictions of an impending recession might have been overly pessimistic, at the very least for now. We’ll proceed to watch this information, and when it begins to strategy ranges usually related to recessionary outcomes, we are going to warn our readers accordingly.

Nevertheless, the implications for the inventory and bond markets are clear for now.

Market Reactions: Why Traders Are Optimistic

Unsurprisingly, monetary markets reacted positively to the most recent GDP report, viewing it as proof that the economic system has prevented a recession from a interval of elevated rates of interest. That optimism has been significantly evident within the inventory market, the place equities have climbed on the again of constructive client information.

A notable instance is the latest surge in economically delicate sectors of the market. As famous not too long ago by Sentiment Dealer:

“When 90% of cyclical sub-industry teams shut above their respective 10, 20, 50, 100, and 200-day shifting averages for the primary time in six months, and the S&P 500 is inside 2% of a five-year excessive, the world’s most benchmarked index displayed stable returns and consistency throughout all time horizons. Over the next three months, the S&P 500 superior 81% of the time, reaching 13 consecutive beneficial properties since 1992.”

Most notably, growth-oriented sectors outperformed the S&P 500 over the following 12 months.

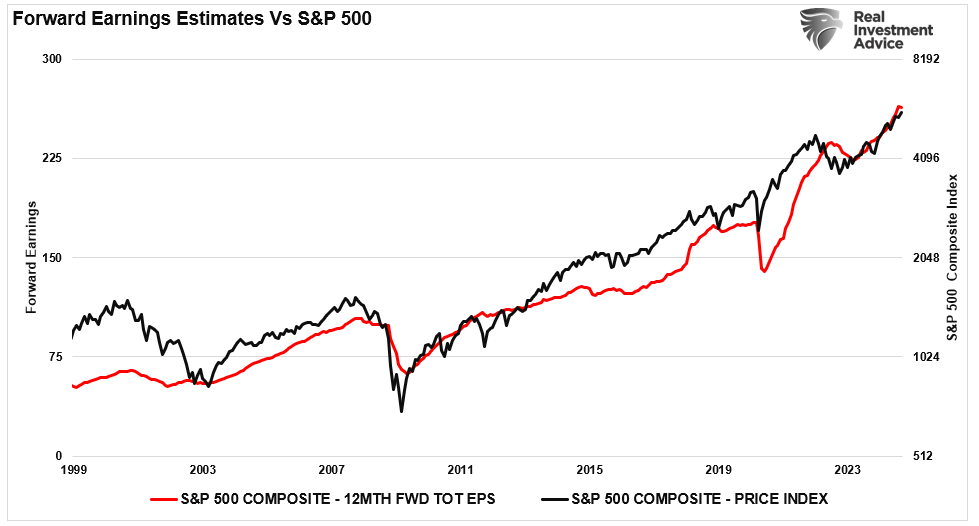

Unsurprisingly, as the danger of recession stays low, progress shares have outperformed high-dividend “defensive” shares. It’s because financial progress gives help for earnings progress. During the last 12 months, analysts have continued pushing estimates increased into 2025, favoring shares depending on quicker earnings progress charges.

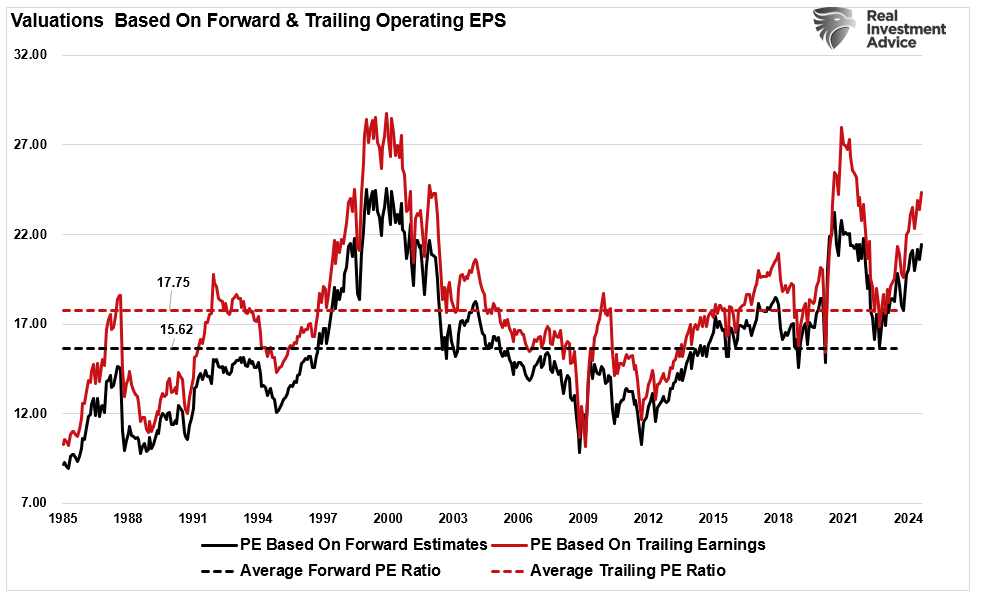

Since buyers are prepared to “pay up” for future earnings, valuations have risen sharply.

As we mentioned not too long ago, the general inventory market is buying and selling on optimism the Federal Reserve will proceed to chop charges. With inflation coming down and progress remaining constructive, many buyers are betting on a situation the place the economic system avoids a recession solely. This “delicate touchdown” narrative has propelled the S&P 500 and different indices regardless of many recessionary issues.

Dangers to Continued Financial Development

Regardless of the Fed’s intervention, a number of dangers to financial progress stay. The Q2 GDP report, whereas constructive, revealed sure vulnerabilities that might threaten future progress, even with decrease charges.

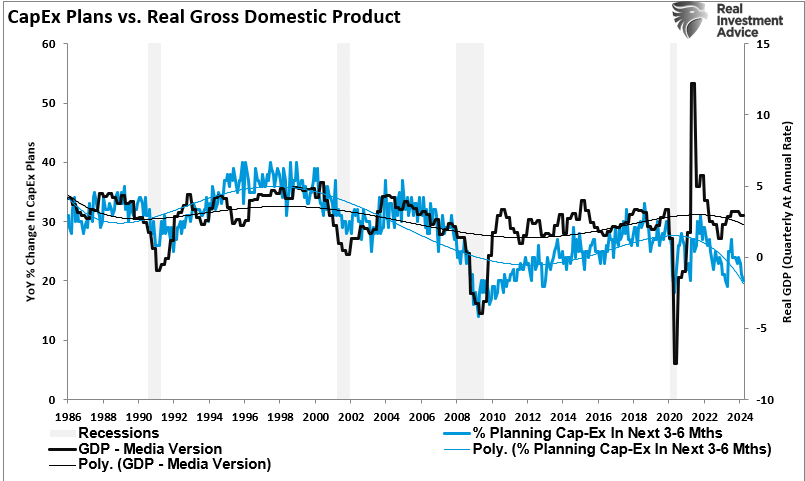

1. Weakened Enterprise Funding

Enterprise funding has slowed in latest reviews, and as famous above, is a direct enter into the GDP report. Whereas decrease borrowing prices will encourage some firms to develop, sectors like manufacturing and development stay constrained by world provide chain points and exterior demand. Moreover, as famous within the NFIB Small Enterprise report, companies might change into extra reluctant to speculate considerably if the economic system slows additional or the upcoming election consequence suggests increased taxes and extra rules are forthcoming.

2. Housing Market Nonetheless Underneath Stress

The housing market, one of the interest-sensitive sectors, has been battered by excessive mortgage charges. The Fed’s fee minimize will present some reduction, nevertheless it is probably not sufficient to totally revive housing demand. With mortgage charges nonetheless elevated by historic requirements and residential costs excessive, affordability stays a difficulty for a lot of potential patrons. Subsequently, whereas we might even see a slight pickup in housing exercise, the general impression of the speed minimize on the housing market might be restricted.

3. Shopper Spending May Sluggish

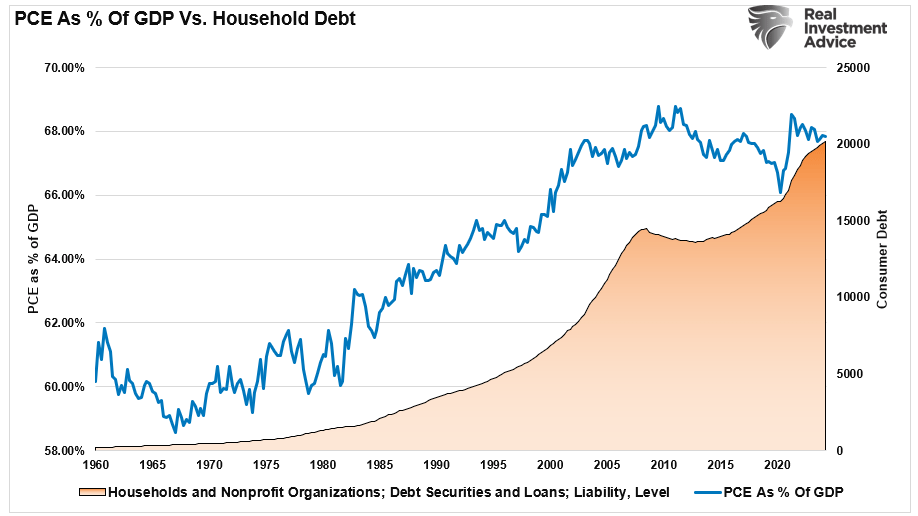

Though client spending remained sturdy in Q2, increased client debt ranges—significantly bank card debt—are an growing concern. Whereas decrease rates of interest will ease the burden for some debtors, the general stage of client debt stays excessive. Because the labor market cools and wage progress moderates, client spending might sluggish within the coming quarters, particularly if inflation continues to pinch family budgets. Notably, PCE as a share of GDP has remained comparatively stagnant since 2010 regardless of a major surge in family debt ranges.

Conclusion

I don’t disagree there are a lot of causes to be involved in regards to the economic system at present. The Authorities is clearly spending like a “drunken sailor” on pet tasks that don’t produce long-term financial prosperity. Geopolitical dangers stay together with upcoming election dangers that might considerably change the panorama for taxes and rules.

Nevertheless, whereas it’s simple to deal with these dangers as a purpose “to not make investments,” the Q2 GDP report continues to supply proof that undermines most of the “doom and gloom” predictions for the U.S. economic system.

A minimum of for now.

Will that finally change? Completely. There will probably be a recession in some unspecified time in the future sooner or later, whether or not in six months or three years. Nevertheless, if we deal with sectors and asset lessons that may carry out properly in each slow-growth and inflationary environments, buyers can navigate the present panorama and capitalize on alternatives, at the same time as some analysts proceed to warn of recession dangers.

Importantly, when a recession approaches, the market has a protracted historical past of letting buyers know.

Sources:

- Bureau of Financial Evaluation (BEA) – Q2 2024 GDP Report

- Federal Reserve Financial Information (FRED)

- U.S. Treasury – Bond Yield Information

Put up Views: 1,965

2024/10/11