{kind=link}

Lately, James Grant, editor of the Curiosity Charge Observer, was requested about his outlook for rates of interest. He sees rates of interest transferring in a cyclical sample, doubtlessly rising for an additional multi-decade interval. Grant bases his view on historic observations reasonably than a mystical perception in cycles. He states that finance has proven a cyclical nature, transferring from extremes of euphoria to revulsion in numerous asset lessons. Subsequently, he proposes that persistent inflation, elevated navy spending, and vital fiscal deficits might drive charges greater. The Fed’s goal of a 2% inflation charge and the citizens’s desire for insurance policies that result in inflation additionally contribute to this development.

Let me state that I’ve an amazing quantity of respect for Grant and his work. Nonetheless, I can’t totally agree along with his view. I’ll focus at the moment’s dialogue on the outlook for rates of interest based mostly on the 2 bolded sentences above.

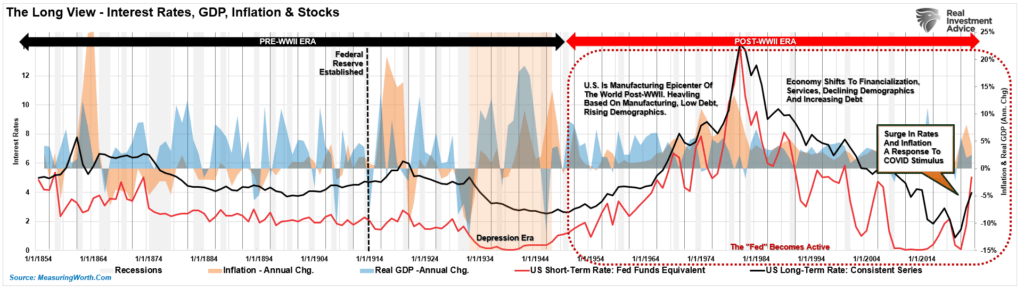

The chart under reveals the long-term view of quick and long-bond rates of interest, inflation, and GDP. As Grant notes, there’s a cycle to rates of interest beforehand.

Rates of interest rose throughout three earlier intervals in historical past.

- Through the financial/inflationary spike within the early 1860s

- The “Golden Age” from 1900-1929 noticed inflation rise as financial development resulted from the Industrial Revolution.

- The newest interval was the extended manufacturing cycle within the Fifties and Nineteen Sixties. That cycle adopted the tip of WWII when the U.S. was the worldwide manufacturing epicenter.

Remembering Historical past

Nonetheless, whereas rates of interest fell through the Despair, financial development and inflationary pressures remained strong. Such was because of the very lopsided nature of the economic system at the moment. Like the present financial cycle, the rich prospered whereas the center class suffered. Subsequently, cash didn’t stream via the system, resulting in a decline in financial velocity.

The Fifties and 60s are a very powerful.

Following World Struggle II, America grew to become the “final man standing.” France, England, Russia, Germany, Poland, Japan, and others had been devastated, with little potential to provide for themselves. America discovered its most substantial financial development because the “boys of conflict” returned dwelling to start out rebuilding a war-ravaged globe.

However that was simply the beginning of it.

Within the late ’50s, America stepped into the abyss as humankind took its first steps into area. The area race, which lasted practically 20 years, led to leaps in innovation and expertise that paved the best way for America’s future.

These advances, mixed with the commercial and manufacturing backdrop, fostered excessive ranges of financial development, elevated financial savings charges, and capital funding, which supported greater rates of interest.

Moreover, the Authorities ran NO deficit, and family debt to internet price was about 60%. So, whereas inflation elevated and rates of interest rose in tandem, the typical family might maintain its residing customary.

So, why is that this little bit of historical past so essential to the outlook of rates of interest,

What Drives Curiosity Charges

Grant means that rates of interest will rise as a result of they’ve been low for thus lengthy. That’s akin to saying that because the Atlanta Falcons haven’t received a Tremendous Bowl within the final 58 years, they need to now win it yearly for the following 58 years. What drives the Atlanta Falcons to win a Tremendous Bowl are the components to result in a terrific crew, not simply the truth that they’ve by no means received one. The identical goes for rates of interest.

Rates of interest are a perform of the final development of financial development and inflation. Extra strong development and inflation charges enable lenders to cost greater borrowing prices throughout the economic system. Such can be why bonds can’t be overvalued. To wit:

“In contrast to shares, bonds have a finite worth. The principal and remaining curiosity funds are returned to the lender at maturity. Subsequently, bond patrons know the value they pay at the moment for the return they may get tomorrow. In contrast to an fairness purchaser taking up funding threat, a bond purchaser loans cash to a different entity for a particular interval. Subsequently, the rate of interest takes into consideration a number of substantial dangers:”

- Default threat

- Charge threat

- Inflation threat

- Alternative threat

- Financial development threat

“Since the future return of any bond, on the date of buy, is calculable to the 1/one hundredth of a cent, a bond purchaser won’t pay a worth that yields a damaging return sooner or later. (This assumes a holding interval till maturity. One would possibly buy a damaging yield on a buying and selling foundation if expectations are benchmark charges will decline additional.) “

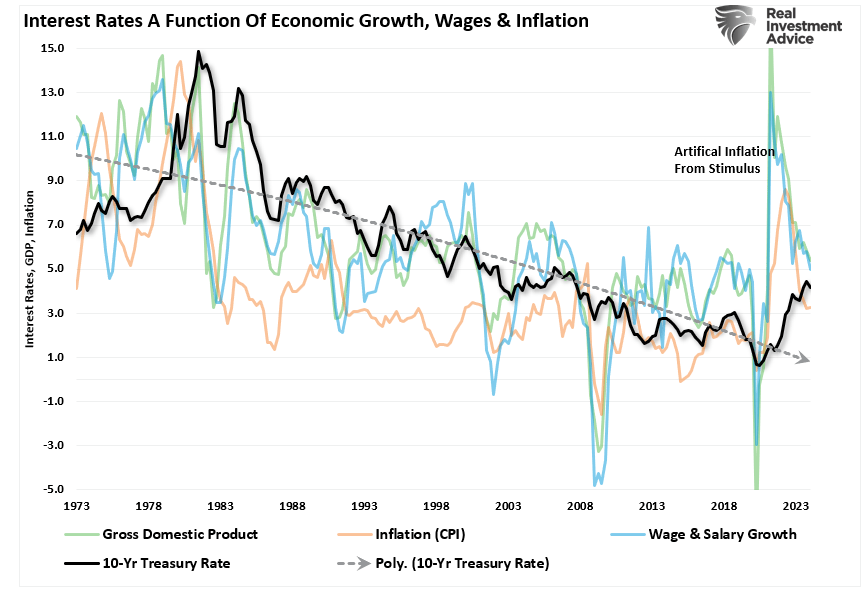

The chart under reveals the correlation between financial development, inflation, and rates of interest. Unsurprisingly, rates of interest rise when financial development will increase, resulting in extra demand for credit score. Inflation rises with financial exercise as the provision/demand imbalance will increase costs. That’s primary economics.

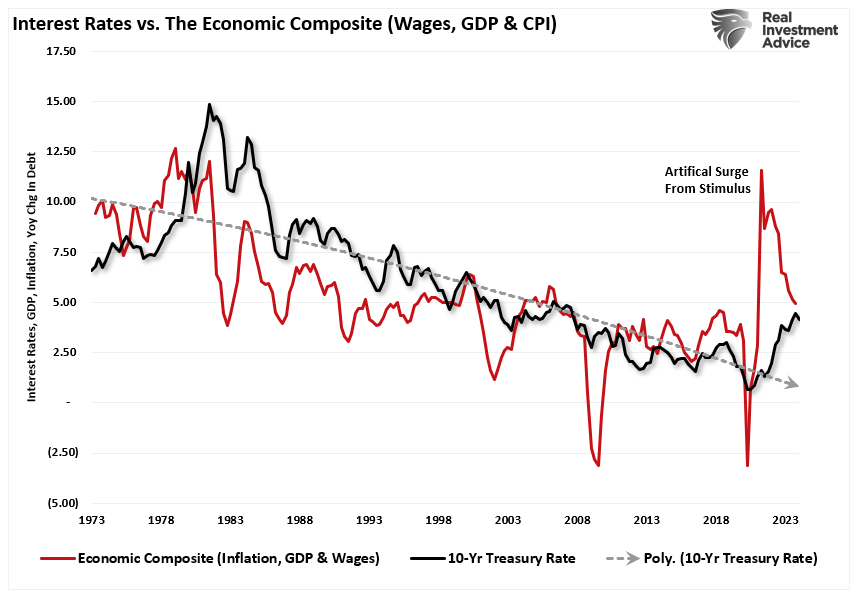

The chart above reveals so much happening, so let’s create a composite index of wages (which offers client buying energy, aka demand), financial development (the results of manufacturing and consumption), and inflation (the byproduct of elevated demand from rising financial exercise). We then examine that composite index to rates of interest. Unsurprisingly, there’s a excessive correlation between financial exercise, inflation, and rates of interest as charges reply to the drivers of inflation.

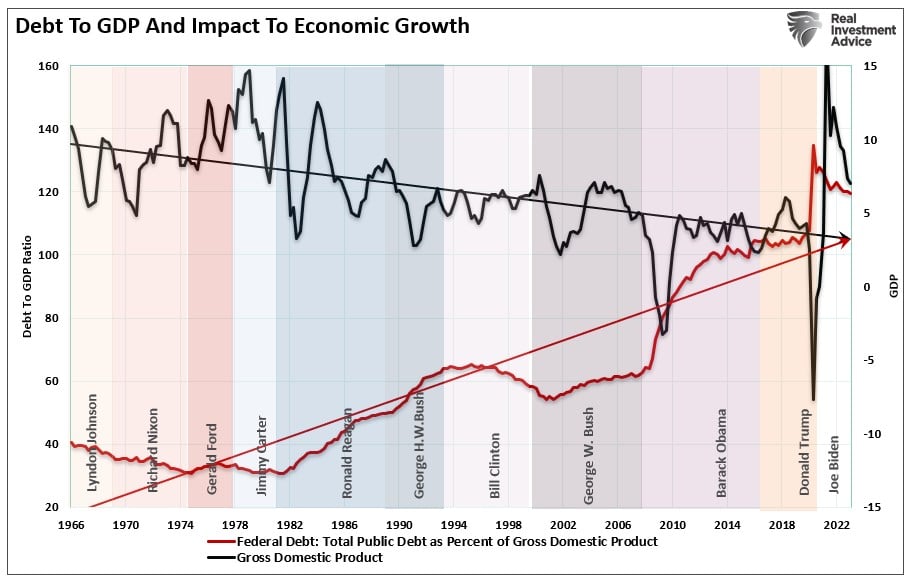

Grant additional means that rates of interest shall be greater as a consequence of elevated debt and deficits. Sadly, there isn’t a proof supporting that speculation.

The Deficit Fallacy

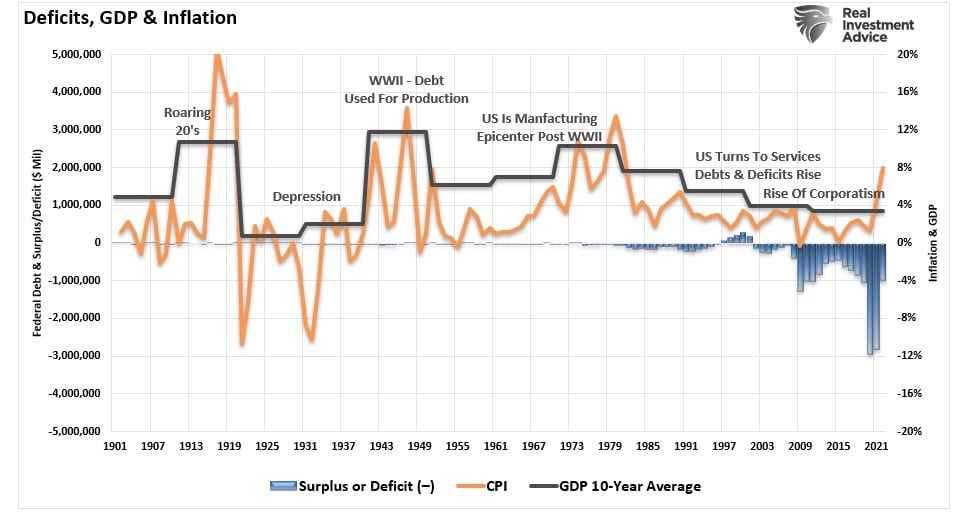

As proven under, the 10-year financial development common correlates with rates of interest. When financial development rises, lenders can cost greater rates of interest.

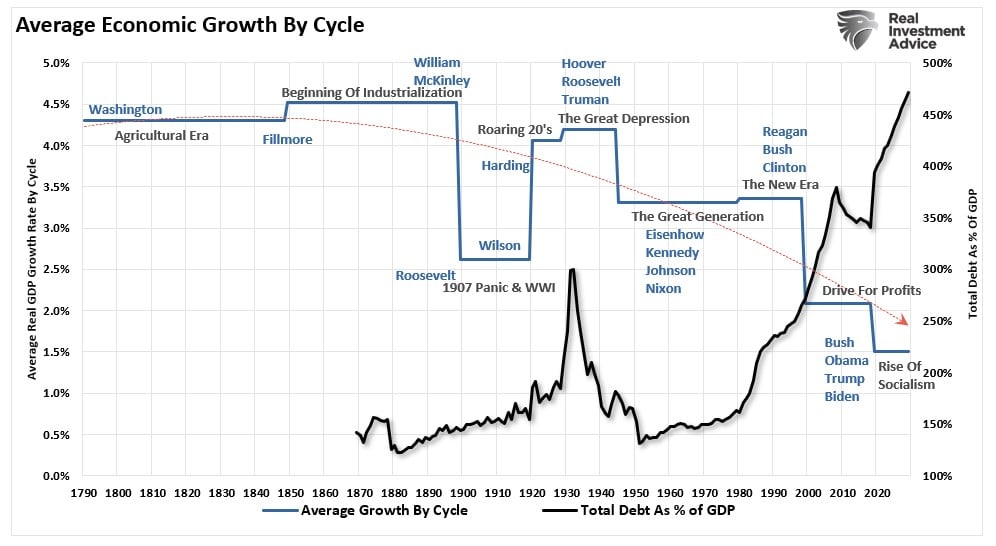

What ought to instantly bounce out at you is that the 10-year common financial development charge was round 8%, apart from the Nice Despair period, from 1900 via 1980. Nonetheless, there was a marked decline in financial development since then. (The present spike in rates of interest is a perform of the substitute stimulus injected into the economic system, which is now reversing.)

Will increase within the nationwide debt squandered on non-productive investments and rising debt service leads to a damaging return on funding. Subsequently, the bigger the debt stability, the extra economically harmful it’s by diverting growing quantities of {dollars} from productive property to debt service.

Since 1980, the general enhance in debt has surged to ranges that presently usurp the whole thing of financial development. What ought to be evident is that will increase in debt and deficits proceed to divert extra tax {dollars} away from productive investments into the service of debt and social welfare. The result’s decrease, not greater, financial development, inflation, and, finally, rates of interest.

When put into perspective, one can perceive the extra vital drawback plaguing financial development. A protracted have a look at historical past clearly reveals the damaging impression of debt on financial development.

Moreover, modifications in structural employment, demographics, and deflationary pressures derived from modifications in productiveness will amplify these issues.

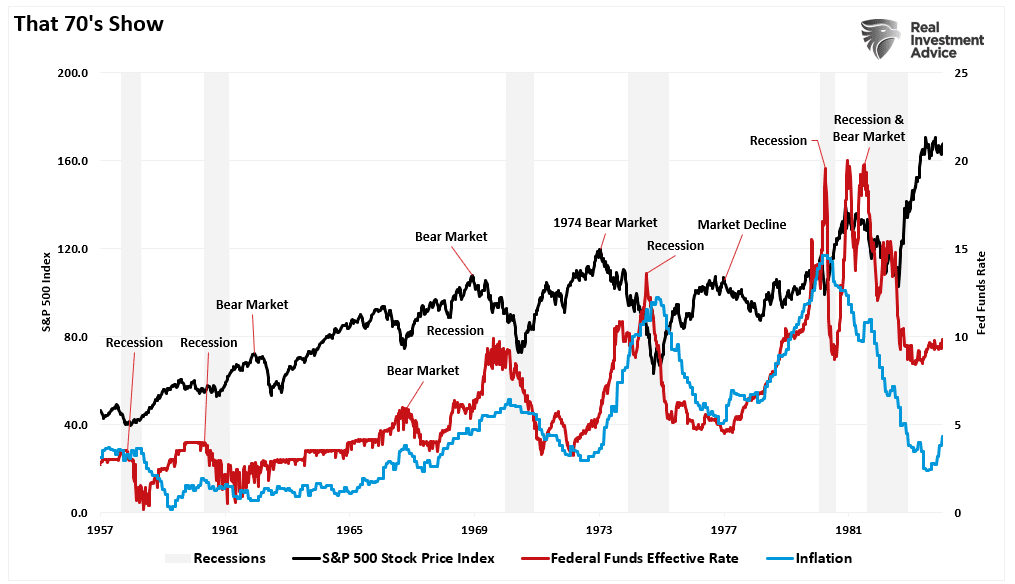

Inflation Wasn’t Simply The Nineteen Seventies

Whereas many concentrate on the inflation surge through the late Nineteen Seventies, as famous above, your complete interval from the Fifties via 1980 was marked by rising rates of interest and inflation as a consequence of a extra strong financial development cycle.

Like at the moment, the Fed was mountaineering charges to quell inflationary pressures from exogenous components. Within the late 70s, the oil disaster led to inflationary pressures as oil costs fed via a manufacturing-intensive economic system. At present, inflation resulted from financial interventions that created demand towards a supply-constrained economic system.

Such is a vital level.

Throughout “That 70s Present,” the economic system was primarily manufacturing-based, offering a excessive multiplier impact on financial development. At present, the combo has reversed, with companies making up the majority of financial exercise. Whereas companies are important, they’ve an especially low multiplier impact on financial exercise.

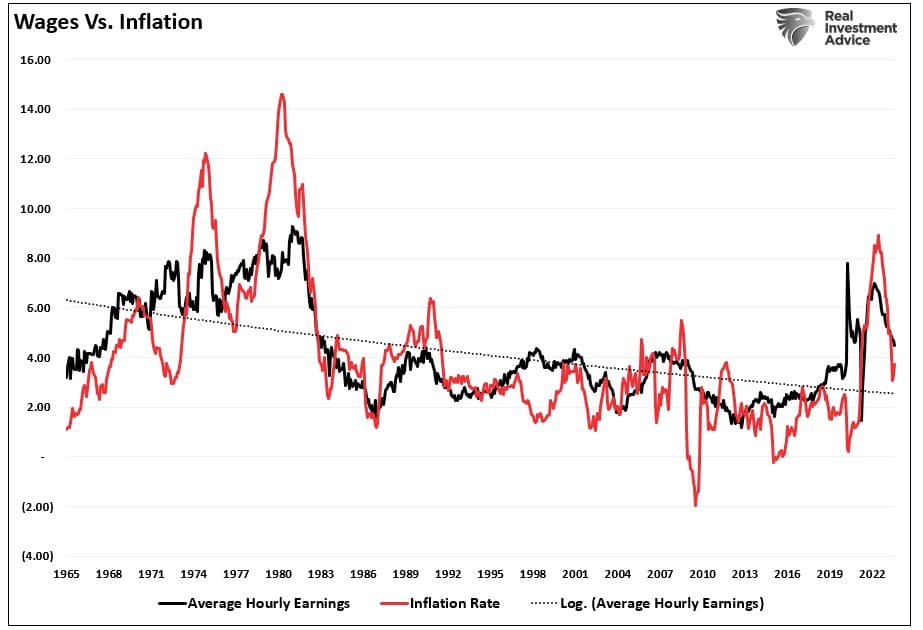

One main purpose is that companies require decrease wage development than manufacturing. Inflation rose within the Nineteen Seventies as a consequence of a gentle development of accelerating wages, which created extra financial demand. Exterior of the substitute spike in demand from authorities stimulus in 2020, the longer-term development of wage development, and finally inflation, is decrease as wage development stays suppressed.

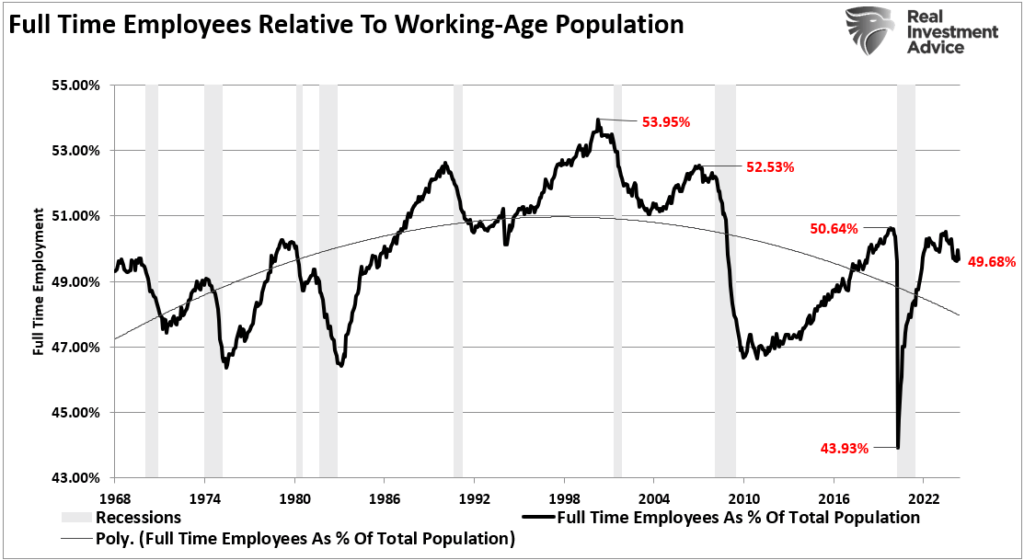

Wages come from the kind of employment. Full-time employment offers greater salaries to help financial development. Sadly, full-time employment as a share of the working-age inhabitants has declined because the flip of the century. Such is because of elevated productiveness ranges via expertise, offshoring, and immigration. The byproduct of fewer full-time workers is decrease consumption and decrease charges of financial development.

At present’s financial setting vastly differs from the financial growth years of the Nineteen Seventies. Rising debt ranges, elevated deficits, productiveness, and wage suppression erode financial development, not help it. Subsequently, whereas Grant makes the case for greater rates of interest for “a lot, for much longer,” the financial proof doesn’t help that thesis.

Conclusion

Nonetheless, even when Grant is right and growing debt ranges and deficits do trigger greater charges, central banks will take actions to artificially decrease charges.

At 4% on 10-year Treasury bonds, borrowing prices stay comparatively low from a historic perspective. Nonetheless, we nonetheless see indicators of financial deterioration and damaging client impacts even at that charge. When the economic system’s leverage ratio is almost 5:1, 5% to six% charges are a completely totally different matter.

- Curiosity funds on the Authorities debt enhance, requiring additional deficit spending.

- The housing market will decline. Folks purchase funds, not homes, and rising charges imply greater funds.

- Increased rates of interest will enhance borrowing prices, which results in decrease revenue margins for firms.

- There’s a damaging impression on the huge derivatives market, main to a different potential credit score disaster as rate of interest unfold derivatives go bust.

- As charges enhance, so do the variable curiosity funds on bank cards. Such will result in a contraction in disposable revenue and rising defaults.

- Rising charges negatively impression banks, as greater charges impair the banks’ collateral, resulting in financial institution failures.

I might go on, however you get the concept.

Subsequently, as debt and deficits enhance, Central Banks are pressured to suppress rates of interest to maintain borrowing prices down and maintain weak financial development charges.

The issue with Grant’s assumption that charges MUST go greater is three-fold:

- All rates of interest are relative. The idea that charges within the U.S. are about to spike greater is probably going mistaken. Increased yields on U.S. debt appeal to flows of capital from nations with low to damaging yields, pushing charges decrease within the U.S. Given the present push by Central Banks globally to suppress rates of interest to maintain nascent financial development going, an eventual zero-yield on U.S. debt just isn’t unrealistic.

- The funds deficit balloon. Given Washington’s lack of fiscal coverage controls and guarantees of continued largesse, the funds deficit is ready to swell above $2 Trillion in coming years. It will require extra authorities bond issuance to fund future expenditures, which shall be magnified through the subsequent recessionary spat as tax income falls.

- Central Banks will proceed to purchase bonds to take care of the present establishment however will turn out to be extra aggressive patrons through the subsequent recession. The Fed’s subsequent QE program to offset the following financial downturn will seemingly be $4 trillion or extra, pushing the 10-year yield towards zero.

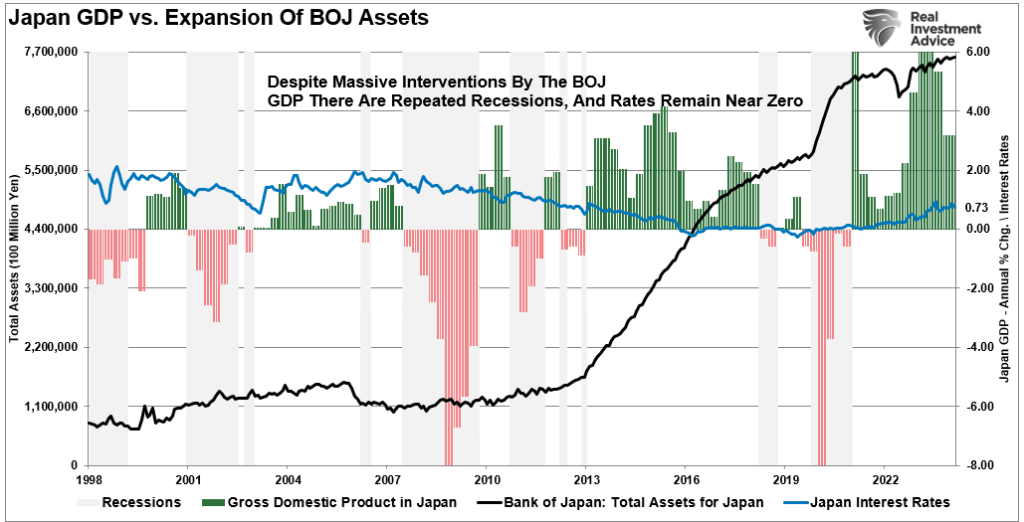

When you want a street map of how this ends with decrease charges, have a look at Japan.

Historic proof means that rates of interest shall be decrease, not greater, until the Authorities embarks on a large infrastructure growth program. Such would doubtlessly revitalize the American economic system and result in greater charges, stronger wages, and a affluent society.

Nonetheless, exterior of that, the trail of rates of interest sooner or later stays decrease.

Publish Views: 3,867

2024/06/14