{kind=link}

In a latest dialogue with Adam Taggart by way of Considerate Cash, we rapidly touched on the similarities between the U.S. and Japanese financial insurance policies across the 11-minute mark. Nonetheless, that dialogue warrants a deeper dive. As we’ll overview, Japan has a lot to inform us about the way forward for the U.S. economically.

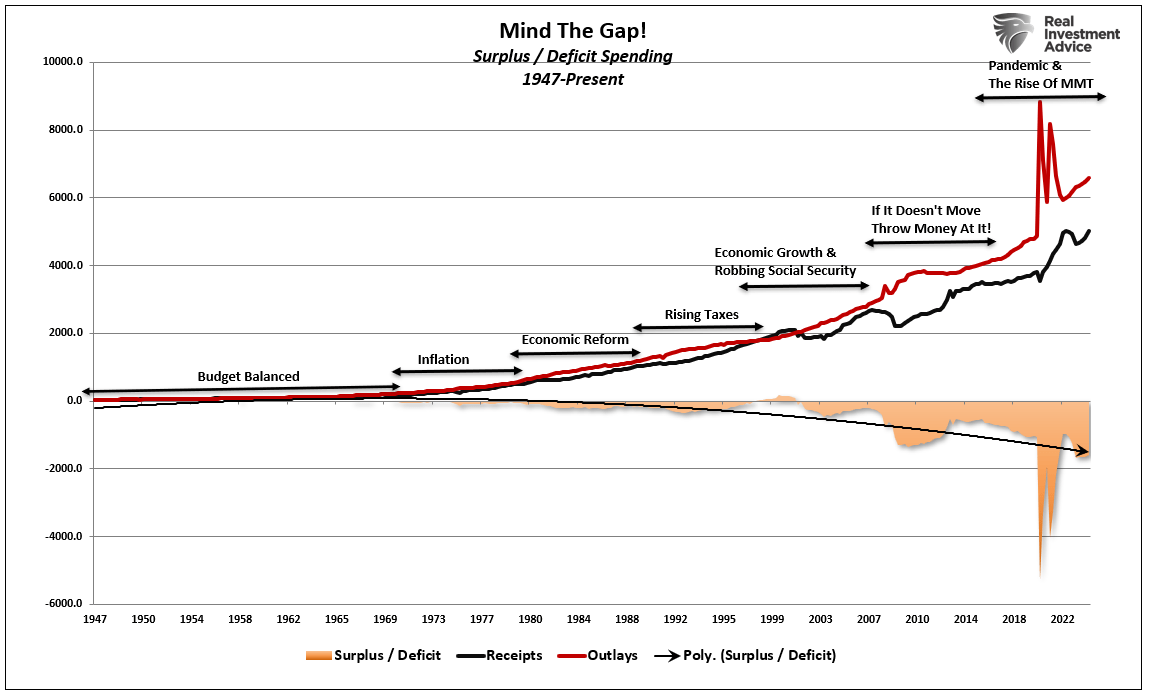

Let’s begin with the deficit. A lot angst exists over the rise in rates of interest. The priority is whether or not the federal government can proceed to fund itself, given the post-pandemic surge in fiscal deficits. From a purely “private finance” perspective, the priority is legitimate. “Dwelling properly past one’s means” has all the time been a recipe for monetary catastrophe.

Notably, extra spending is not only a perform of latest occasions however has been 45 years within the making. The federal government began spending extra within the late Nineteen Seventies than it introduced in tax receipts. Nonetheless, because the economic system recovered by way of “monetary deregulation,” economists deemed extra spending useful. Sadly, every Administration continued to make use of growing debt ranges to fund each conceivable pet political challenge. From elevated welfare to “pandemic-related” bailouts to local weather change agendas, it was all truthful sport.

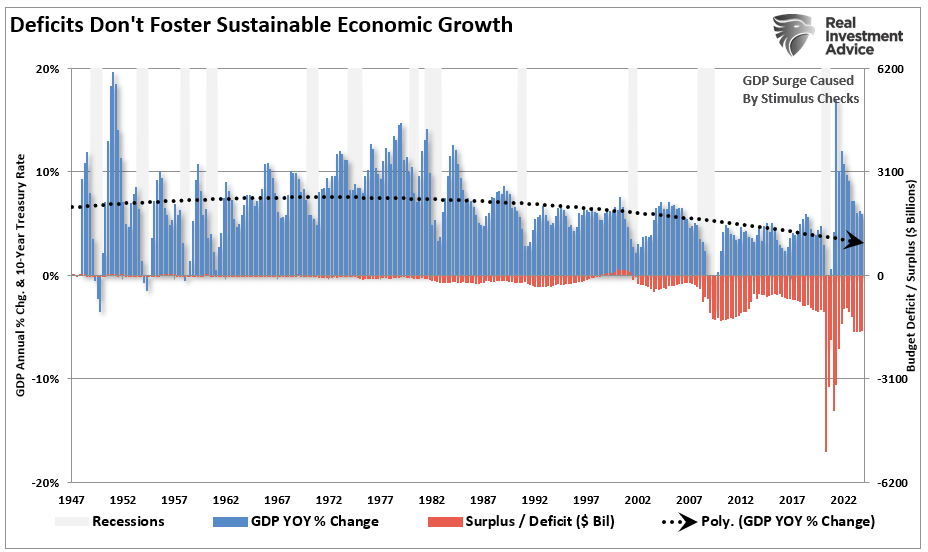

Nonetheless, whereas extra spending appeared to offer short-term advantages, primarily the good thing about getting re-elected to workplace, the impression on financial prosperity has been detrimental. To economists’ shock, Rising money owed and deficits haven’t created extra strong financial development charges.

I’m not saying there isn’t any profit. Sure, “spending like drunken sailors” to create financial development can work short-term, as we noticed post-pandemic. Nonetheless, as soon as that surge in spending is exhausted, financial development returns to earlier ranges. What these applications do is “pull ahead” future consumption, leaving a void that detracts from financial development sooner or later. That’s the reason financial prosperity continues to say no after a long time of deficit spending.

We agree that rising money owed and deficits are actually regarding. Nonetheless, the argument that the U.S. is about to develop into bankrupt and fall into financial oblivion is unfaithful.

For a case research of the place the U.S. is headed, a have a look at Japanese-style financial coverage is helpful.

The Failure Of Central Banks

“Unhealthy debt is the basis of the disaster. Fiscal stimulus could assist economies for a few years however as soon as the ‘painkilling’ impact wears off, U.S. and European economies will plunge again into disaster. The disaster gained’t be over till the nonperforming property are off the stability sheets of US and European banks.” – Keiichiro Kobayashi, 2010

Kobayashi will finally be proved appropriate. Nonetheless, even he by no means envisioned the extent to which Central Banks globally can be keen to go. As my accomplice, Michael Lebowitz identified beforehand:

“International central banks’ post-financial disaster financial insurance policies have collectively been extra aggressive than something witnessed in fashionable monetary historical past. During the last ten years, the six largest central banks have printed unprecedented quantities of cash to buy roughly $24 trillion of monetary property as proven beneath. Earlier than the monetary disaster of 2008, the one central financial institution printing cash of any consequence was the Peoples Financial institution of China (PBoC).”

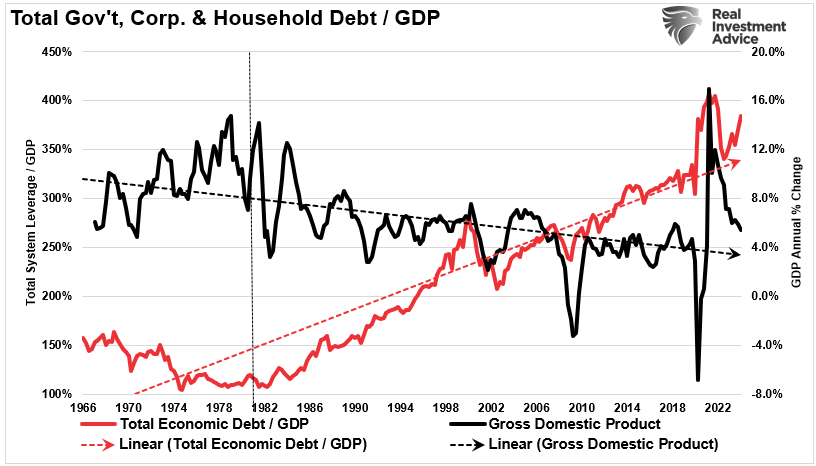

The assumption was that driving asset costs larger would result in financial development. Sadly, this has not been the case, as debt has exploded globally, particularly within the U.S.

“QE has compelled rates of interest downward and lowered curiosity bills for all debtors. Concurrently, it boosted the quantity of excellent debt. The online impact is that the worldwide debt burden has grown on a nominal foundation and as a share of financial development since 2008. The debt burden has develop into much more burdensome.”

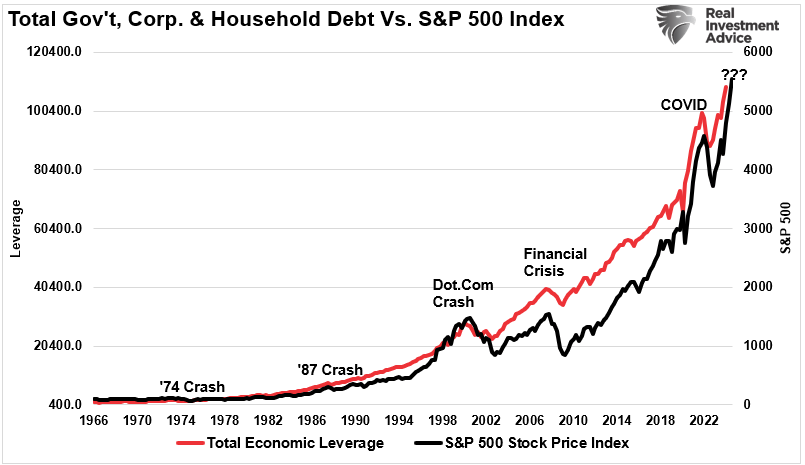

Not surprisingly, the large surge in debt has led to an explosion within the monetary markets as low cost debt and leverage fueled a speculative frenzy in nearly each asset class.

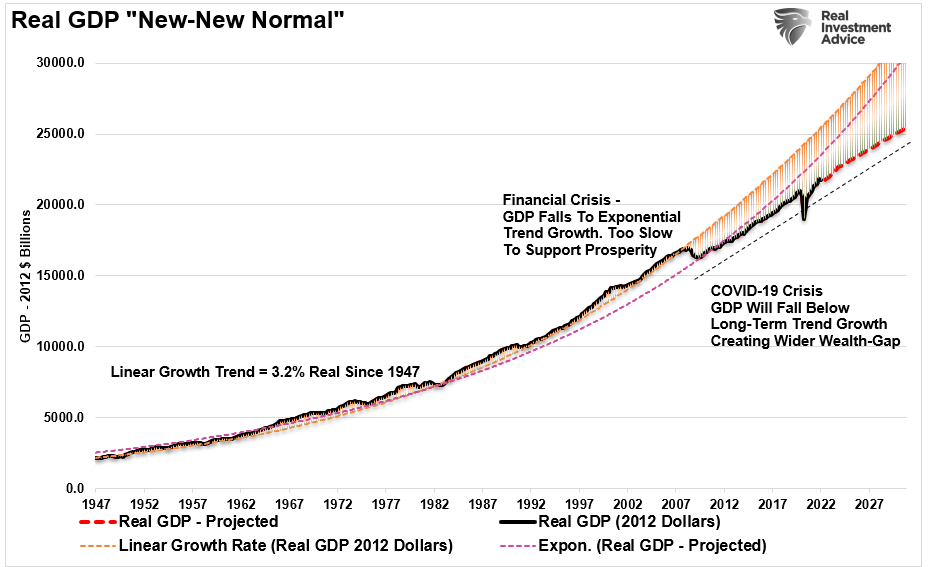

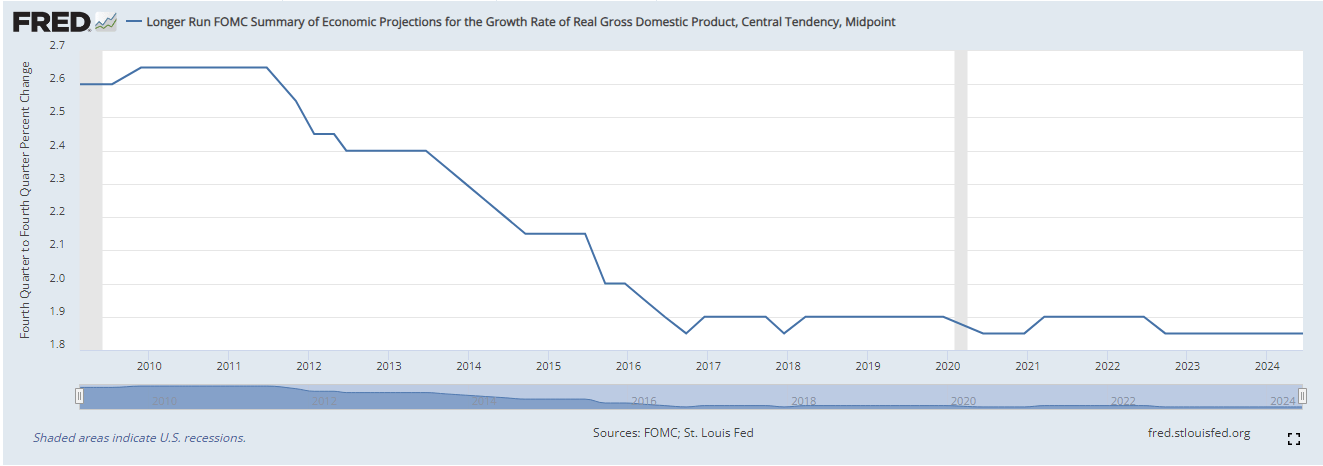

Hovering U.S. debt, rising deficits, and demographics are the culprits behind the economic system’s disinflationary push. The complexity of the present surroundings implies years of sub-par financial development forward. The Federal Reserve’s long-term financial projections stay at 2% or much less.

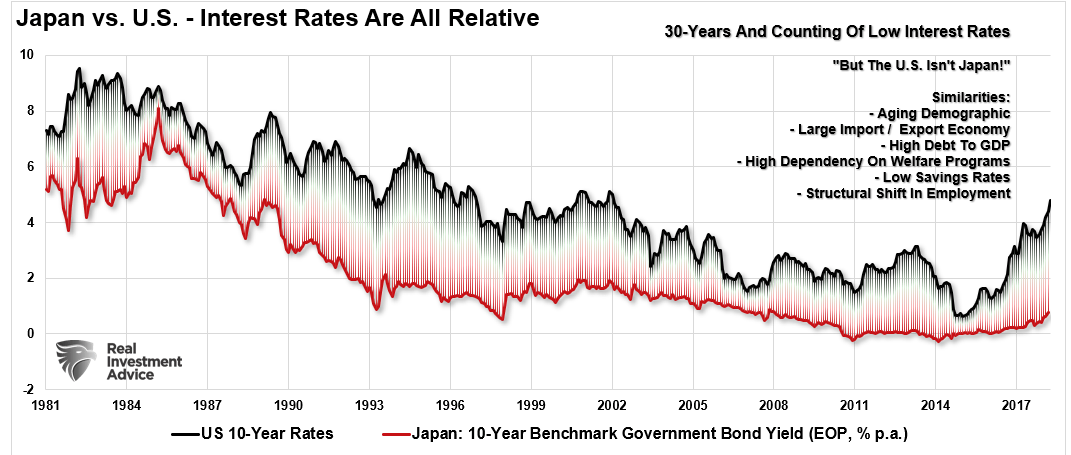

The U.S. isn’t the one nation going through such a dark public finance outlook. The present financial overlay shows compelling similarities with the Japanese economic system.

Many imagine that extra spending will repair the issue of lackluster wage development, create extra jobs, and increase financial prosperity. Nonetheless, one ought to at the least query the logic provided that extra spending, as represented within the debt chart above, had ZERO lasting impression on financial development. As I’ve written beforehand, debt is a retardant to natural financial improvement because it diverts {dollars} from productive funding to debt service.

Japanese Coverage And Financial Outcomes

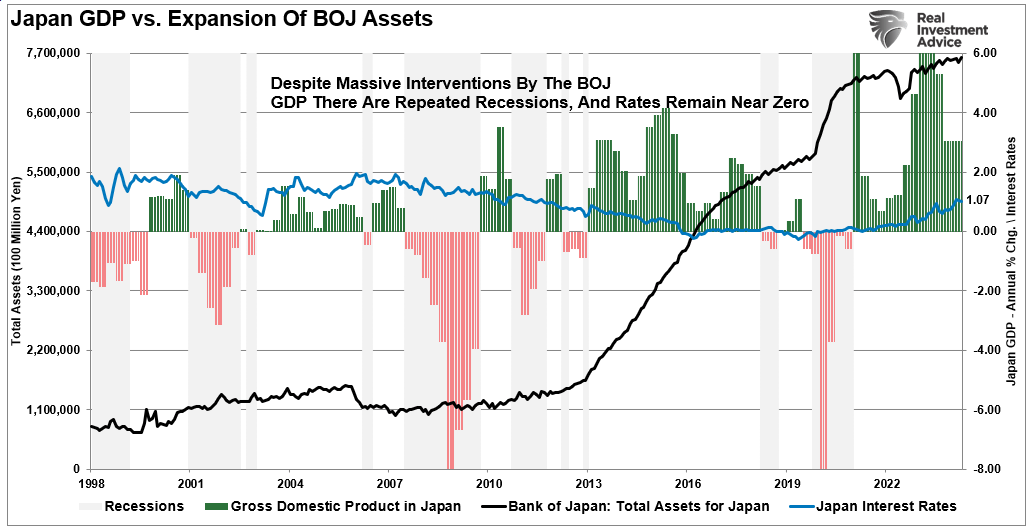

One solely wants to have a look at the Japanese economic system to grasp that Q.E., low-interest charge insurance policies, and debt enlargement have finished little economically. The chart beneath exhibits the enlargement of BOJ property versus the expansion of GDP and rate of interest ranges.

Discover that since 1998, Japan has been unable to maintain a 2% financial development charge. Whereas large financial institution interventions by the Japanese Central Financial institution have absorbed many of the ETF and Authorities Bond market, spurts of financial exercise repeatedly fall into recession. Even with rates of interest close to zero, financial development stays weak, and makes an attempt to create inflation or improve rates of interest have rapid detrimental impacts. Japan’s 40-year experiment offers little assist for the concept that inflating asset costs by shopping for property results in extra substantial financial outcomes.

Nonetheless, the present Administration believes our final result will likely be totally different.

With the present financial restoration already pushing the lengthy finish of the financial cycle, the chance is rising that the subsequent financial downturn is nearer than not. The hazard is that the Federal Reserve is now doubtlessly trapped with an incapability to make use of financial coverage instruments to offset the next financial decline when it happens.

That’s the similar drawback Japan has wrestled with for the final 25 years. Whereas Japan has entered into an unprecedented stimulus program (on a relative foundation twice as massive because the U.S. on an economic system 1/3 the scale), there isn’t any assure that such a program will outcome within the desired impact of pulling the Japanese economic system out of its 40-year deflationary cycle. The issues that face Japan are much like what we’re at present witnessing within the U.S.:

- A decline in financial savings charges to extraordinarily low ranges which depletes productive investments

- An getting old demographic that’s top-heavy and drawing on social advantages at an advancing charge.

- A closely indebted economic system with debt/GDP ratios above 100%.

- A decline in exports attributable to a weak world financial surroundings.

- Slowing home financial development charges.

- An underemployed youthful demographic.

- An inelastic supply-demand curve

- Weak industrial manufacturing

- Dependence on productiveness will increase to offset decreased employment

The lynchpin to Japan and the U.S. stays demographics and rates of interest. Because the getting old inhabitants grows and turns into a internet drag on “financial savings,” dependency on the “social welfare internet” will proceed to broaden. The “pension drawback” is simply the tip of the iceberg.

Conclusion

Just like the U.S., Japan is caught in an ongoing “liquidity entice” the place sustaining ultra-low rates of interest is the important thing to sustaining an financial pulse. The unintended consequence of such actions, as we’re witnessing within the U.S. at present, is the continued battle with deflationary pressures. The decrease rates of interest go, the much less financial return that’s generated. Opposite to mainstream thought, an ultra-low rate of interest surroundings has a detrimental impression on making productive investments, and threat begins to outweigh the potential return.

Extra importantly, whereas rates of interest did rise within the U.S. because of the large surge in stimulus-induced inflation, charges will return to the long-term downtrend of deflationary pressures. Whereas many anticipate charges to extend because of the rise in debt and deficits, such is unlikely for 2 causes.

- Rates of interest are relative globally. Charges can’t rise in a single nation, whereas most world economies push towards decrease charges. As has been the case during the last 30 years, so goes Japan, and the U.S. will observe.

- Will increase in charges additionally kill financial development, dragging charges decrease. Like Japan, each time charges start to rise, the economic system rolls right into a recession. The U.S. will face the identical challenges.

Sadly, for the subsequent Administration, makes an attempt to stimulate development by way of extra spending are unlikely to vary the result within the U.S. The reason being that financial interventions and authorities spending don’t create natural, sustainable financial development. Merely pulling ahead future consumption by way of financial coverage continues to go away an ever-growing void. Ultimately, the void will likely be too nice to fill.

However hey, let’s hold doing the identical factor over and over. Whereas it hasn’t labored for anybody but, we will all the time hope for a distinct outcome.

What’s the worst that would occur?

Submit Views: 1,719

2024/08/30