{kind=link}

A few years in the past I wrote about market effectivity and investing edge – and about how you don’t have it.

However let’s dig deeper into why that is true.

You typically hear from retail punters {and professional} buyers alike that passive (or index) investing makes markets much less environment friendly.

Their argument is that this inefficiency is what justifies energetic administration.

Properly, they’re incorrect – however not in the best way you may suppose. The fact is extra nuanced.

Let’s do some maths to elucidate how passive investing truly makes life tougher for energetic managers, not simpler.

Mannequin market: Alice, Bob, and Clifton

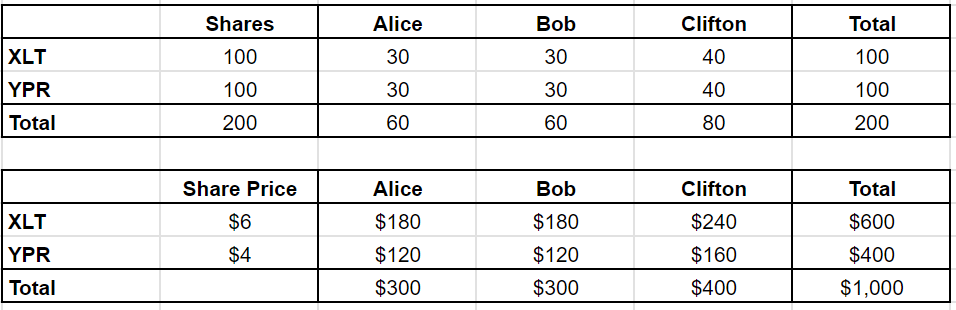

Think about a market with two shares, XLT and YPR, and three buyers: Alice, Bob, and Clifton.

The overall market capitalisation is $1,000.

Between them, Alice, Bob, and Clifton maintain portfolios that add as much as that $1,000.

There aren’t any different firms and no different buyers – we’re maintaining issues easy – however the methods wherein this mannequin is ‘incorrect’ usually are not actually materials to the purpose at this time.

Alice and Bob every maintain $300, whereas Clifton has $400.

XLT and YPR every have 100 shares excellent, with XLT priced at $6 per share and YPR at $4.

(Sure, that is beginning to sound like GCSE maths, however stick with me.)

In different phrases:

Now, Alice, Bob, and Clifton all maintain market weight portfolios. This makes them passive buyers by default.

Ideologically although, Clifton is your basic index fund investor – passive via and thru.

Alice and Bob, however, are energetic merchants. They’re prepared to take a punt in the event that they sense an edge.

So this market is 40% passive (Clifton) and 60% energetic (Alice and Bob).

Dumb passive cash?

One frequent false impression is that passive buyers blindly ‘purchase costly shares’ when costs rise.

Let’s expose this delusion with an instance.

XLT releases stellar outcomes earlier than the market open, and Alice decides she’s bullish. She calls Bob to purchase a few of his XLT inventory, figuring out that Clifton – the passive man – mainly doesn’t commerce. (Clifton doesn’t even hassle going to the workplace until after lunch!)

Right here’s how their dialog goes:

Ring, ring…

- Alice: “Hey Bob, I’m out there for XLT. What are you providing?”

- Bob: “Hmm, I noticed their outcomes. Sturdy stuff. I’d have to begin with an 8…”

- Alice: “I used to be pondering extra like $7.95.”

- Bob: “LOL, nope. I’d purchase from you at that worth. $8.05 – remaining provide.”

- Alice: “I’ll depart my bid on Quotron. Name me if you happen to change your thoughts.”

- Bob: “Catch you later.”

When Clifton lastly will get into the workplace – someday after his tennis match and an extended lunch on the membership – he logs onto his Quotron and sees that XLT has jumped 33% to $8.00.

A information headline studies: XLT Surges on Blowout Outcomes – Mild Quantity.

Happy along with his morning’s ‘work’, Clifton updates his portfolio to mirror the brand new costs.

So be aware that no one did any buying and selling in any respect right here. Alice and Bob simply kind of agreed that $8 was an inexpensive worth for XLT, and so, by proxy, did Clifton.

That is how most worth strikes within the inventory market occur. You don’t want buying and selling to maneuver costs.

The alpha chase

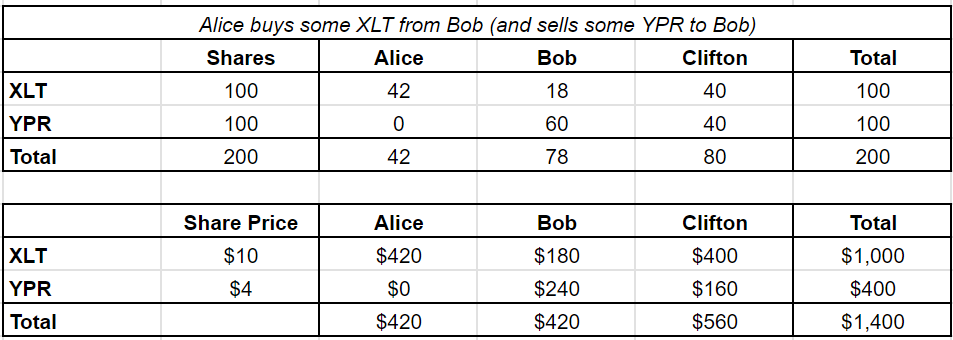

Quick-forward a number of weeks, and Alice will get some inside information on XLT – let’s say from a pleasant spherical of golf with its CEO. The corporate is about to safe a significant authorities contract.

Alice tries once more to purchase from Bob, who smells one thing fishy. He agrees to promote her some XLT shares – however at a fair increased worth, $10 per share.

Since this can be a closed system, Alice must promote YPR to lift the money to purchase XLT. And guess who she has to promote it to? Bob. They comply with swap their stakes.

Alice is now all-in on XLT, whereas Bob holds extra YPR. (For comfort we’re ignoring that Bob would most likely demand a reduction on the YPR he’s shopping for, in addition to a premium on the XLT he’s promoting – Alice’s ‘market impression’).

Right here’s a standing verify:

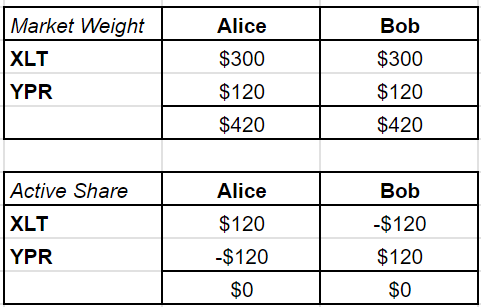

And right here’s the kicker: for Alice to obese XLT, Bob should underweight it. Clifton, because the passive investor, doesn’t change his positions in any respect.

It is a zero-sum recreation. Each greenback of ‘energetic share’ that Alice holds must be offset by Bob’s:

None of this has modified their relative portfolio values – however it should.

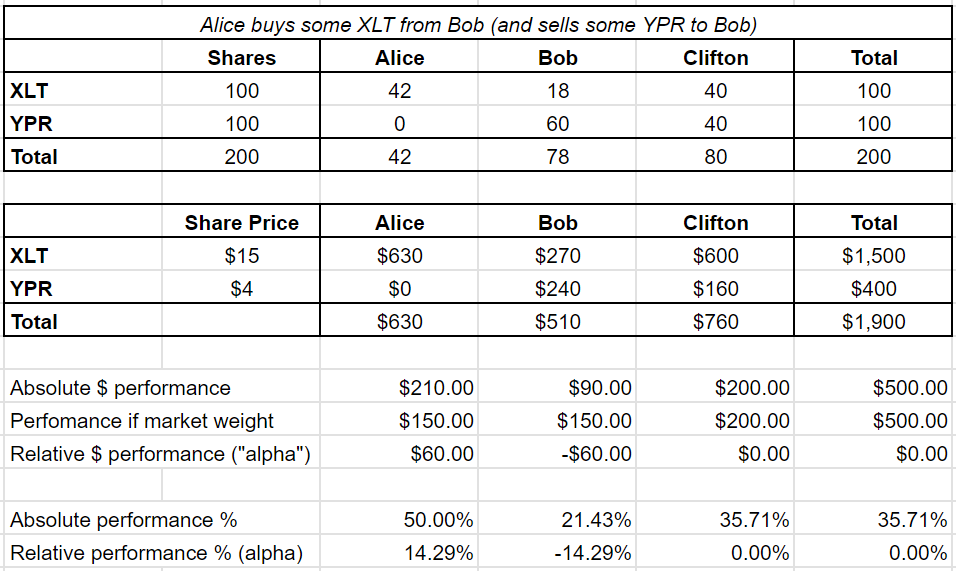

When XLT surges 50% on information of the contract, Alice makes a $60 revenue.

However Bob? His loss is the precise mirror of Alice’s achieve:

Since anybody can simply purchase the market, what issues for energetic buyers is outperformance.

Alice’s outperformance (aka alpha or revenue) of $60 is strictly offset by Bob’s underperformance of $60.

Bob nonetheless made cash. Simply much less cash than he would if he’d stayed market weight.

I do know I preserve making the identical level, nevertheless it’s vital: Alice can solely make her $60 alpha on the expense of Bob.

The winner wants the loser.

Rising passive share

Now let’s think about that Clifton, our passive investor, controls extra of the market than earlier than.

Let’s say the market has shifted so Clifton now runs $600 of the entire $1,000.

In the meantime Bob solely has $100 to handle whereas Alice’s capital stays the identical at $300.

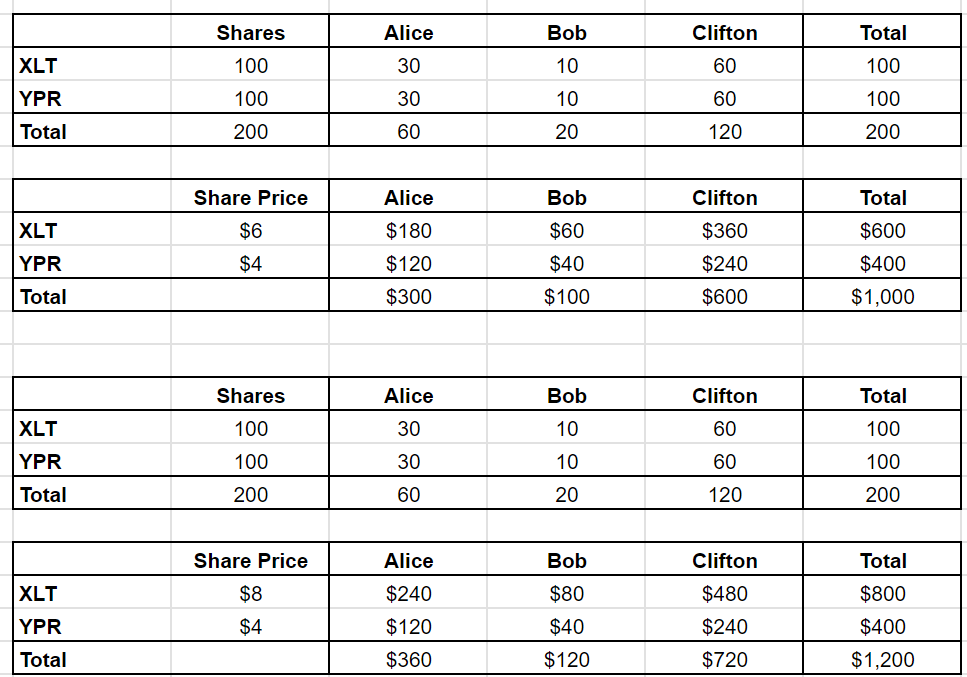

The passive share of the market has grown from 40% to 60%. Let’s re-run that first dialog between Alice and Bob that bumped up the value of XLT to $8, to see the place it will get us.

Ring, ring…

To date, nothing modifications. Nevertheless when Alice returns from golf with XLT’s CEO and tries to purchase extra shares, issues get trickier.

Bob doesn’t have sufficient shares to promote her all that she desires. Now Bob solely has ten shares of XLT, priced at $10 every, for a complete of $100.

Alice has $120 value of YPR to promote, however she will’t purchase as a lot XLT as she would have favored:

As passive buyers like Clifton take up extra market share, Alice’s technique runs right into a brick wall. She will’t go all-in on her insider tip as a result of there aren’t sufficient energetic contributors to commerce with.

And that’s a significant drawback for her alpha.

The truth is let’s verify what it’s executed to everybody’s alpha in comparison with our earlier instance of 40% passive market share:

It’s received worse for everybody besides Clifton!

- Alice’s alpha has diminished.

- Bob’s adverse alpha, in proportion to his capital, is now even worse.

- Clifton doesn’t care both manner.

The passive doom loop

Let’s think about that Alice retains getting fortunate – or inside data – and Bob persistently underperforms.

Finally, a few of Bob’s buyers will redeem their cash. Diehard believers within the quest for outperformance, they wish to hand it to Alice – however they’ll’t.

Why not? As a result of Alice’s technique is capacity-constrained.

Alice can solely generate income if she will commerce towards another person, like Bob. But when Bob’s buyers depart him and put their cash into Alice’s fund, she’ll have fewer folks to commerce with – which means she will’t deploy the capital successfully.

Bob’s redemptions have to stream to Clifton.

And so passive cash grows, and energetic managers like Alice and Bob have ever fewer alternatives to beat the market. As passive share will increase, energetic administration turns into tougher and tougher.

It doesn’t matter how good Alice’s inside data is. Her means to monetise her edge is proscribed by the availability of suckers she will commerce towards.

That is the place the so-called doom loop is available in.

As passive investing grows, energetic investing will get harder, which drives extra money to passive funds, which makes life even tougher for energetic managers… and so forth, in a vicious cycle.

Who’s Alice?

So, how do you notice a foul hedge fund?

Straightforward. They’re those prepared to take your cash.

The true hedge fund giants – names like RenTech, Citadel, and Millennium – received’t even allow you to make investments.

Why? As a result of their alpha is capability constrained.

These guys typically can’t even compound their very own cash.

Should you’re an investor with RenTech – which suggests you’d must work there – it cuts you a cheque for the income each quarter. You don’t get to go away the cash in there compounding for the long-term.

Such funds have already soaked up all of the market inefficiencies their technique has unearthed.

They’ll’t let simply anybody in – in actual fact they want suckers on the opposite aspect of their trades, so why not you.

Don’t be Bob

Lastly – who’s Bob?

Bob is anybody prepared to underperform for lengthy intervals with out having the cash taken away.

For years, this was the underperforming energetic mutual fund supervisor.

Now? More and more, it’s retail buyers.

Why do you suppose hedge funds, prop outlets, and market makers pays brokers to commerce towards their retail order stream?

*Cough* *cough* – I imply, present ‘worth enchancment’ providers!

Don’t be Bob.

Observe Finumus on Twitter and browse his different articles for Monevator.