{kind=link}

In final week’s dialogue with Considerate Cash, I famous that we have gotten extra “tactically bearish” as we progress into 2025. Whereas now we have remained primarily bullish in fairness positioning during the last two years, a number of dangers at the moment are value contemplating.

Nevertheless, it’s vital to notice that being “tactically bearish” does NOT imply we predict a bear market or a extreme market crash. Relating to portfolio administration, the distinction between being “tactically bullish” or “tactically bearish” is the extent of fairness threat we soak up shopper portfolios. During the last two years, now we have been “tactically bullish” and have held extra important weightings in equities which have benefitted from market momentum and investor sentiment. Nevertheless, shifting towards a “tactically bearish” place would recommend rebalancing publicity to extra basic, value-oriented, dividend-paying corporations that can cut back general portfolio volatility. It additionally could imply proudly owning much less fairness publicity and rising money ranges.

Might a “crash” occur? Sure. Nevertheless, bear markets hardly ever occur abruptly. In most bear markets, the market confirmed loads of warning indicators nicely earlier than the “bear” got here out of hibernation. Such gave traders ample time to exit the market, cut back dangers, and lift money to attenuate the eventual reversion to capital. Even a easy technical sign, corresponding to when the market violates the 48-week easy shifting common, allowed traders to exit threat nicely earlier than the remainder of the correction occurred. Did you get out proper on the high? No. Did you get again in on the actual backside? No. Did you take part in many of the advance and keep away from most declines? Sure.

Moreover, as mentioned in “Credit score Spreads,” the distinction between Treasury and Junk bond yields tends to be one of many earliest alerts that credit score markets are pricing in larger dangers. In contrast to inventory markets, which might typically stay buoyant resulting from short-term optimism or speculative buying and selling, the credit score market is extra delicate to basic shifts in financial situations.

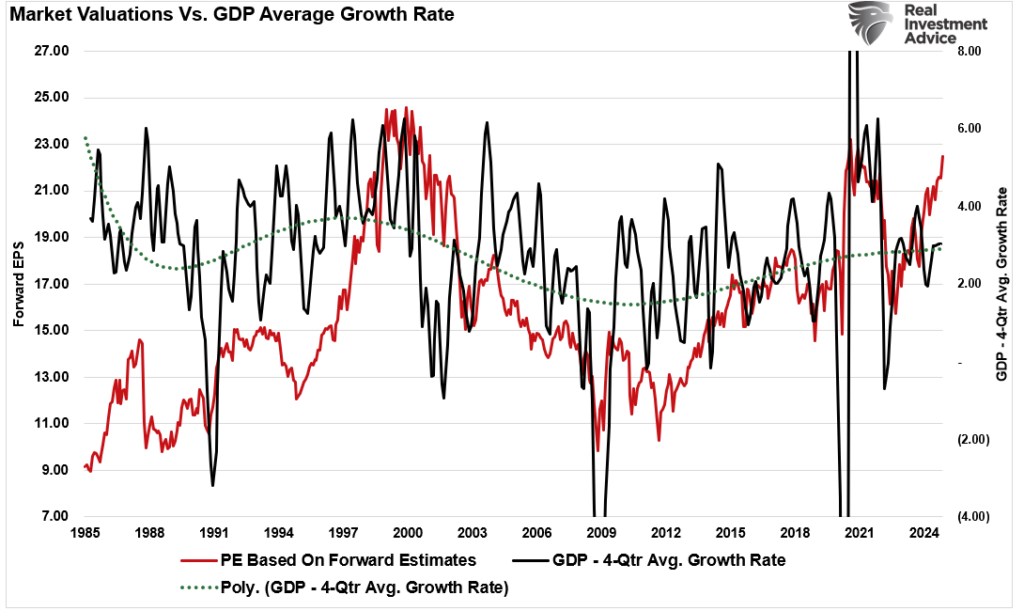

At present, Wall Avenue analysts are very optimistic about 2025. Notably, earnings estimates for 2025 stay nicely deviated from historic long-term development tendencies. That in and of itself isn’t a motive to be extra cautious. Nevertheless, present valuations recommend that shares are priced for perfection as asset costs are nicely forward of what a declining financial development fee can ship. This leaves little room for error. In different phrases, traders are primarily betting on companies’ flawless execution in a yr when macroeconomic uncertainties loom giant.

Within the quick time period, valuations are a horrible timing software for traders. Nevertheless, there are occasions when valuations collide with different elements, making them a extra important short-term threat.

Rates of interest are a kind of elements.

Curiosity Charges Are An Unappreciated Danger

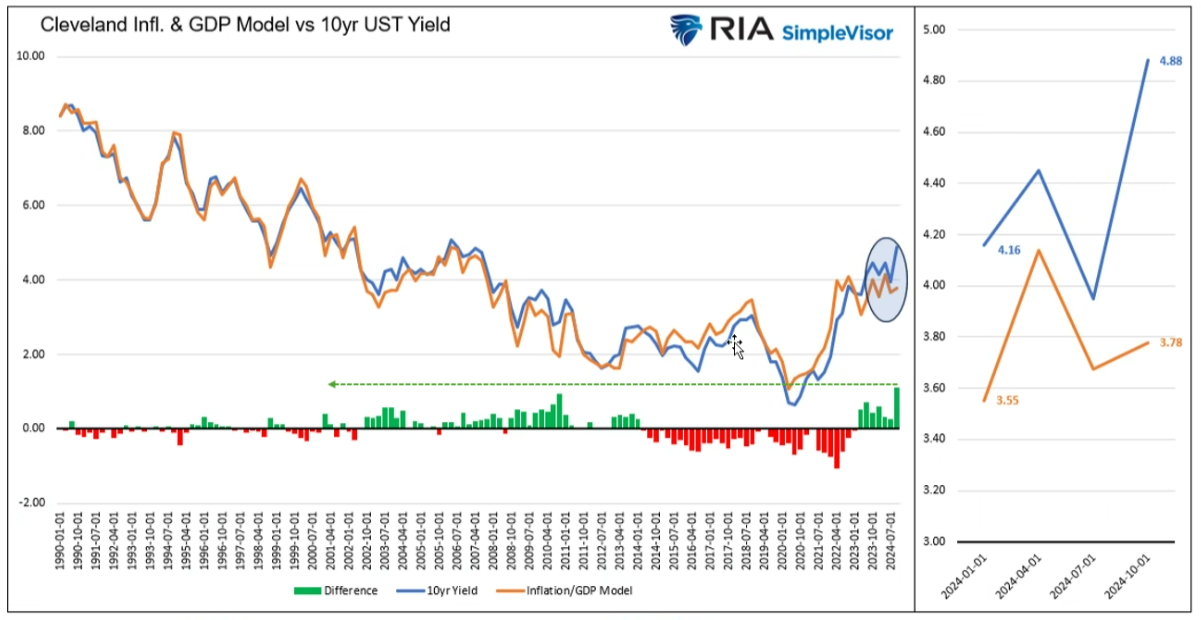

During the last two months, rates of interest have risen sharply resulting from fears of “tariffs” underneath the brand new Administration. Moreover, there may be concern that stronger-than-expected financial information may stall the Federal Reserve from chopping charges additional. Notably, the speed enhance is primarily a operate of short-term sentiment, as financial information stays in a longer-term reversion course of. Michael Lebowitz just lately mentioned the influence of sentiment on charges. The mannequin under combines the Cleveland Fed Inflation Expectations Index and GDP right into a mannequin. (Financial exercise is what creates inflation: provide vs demand). That mannequin traditionally dictates the place rates of interest must be. Whereas rates of interest are nearing 5%, the financial and sentiment mannequin says charges must be nearer to three%.

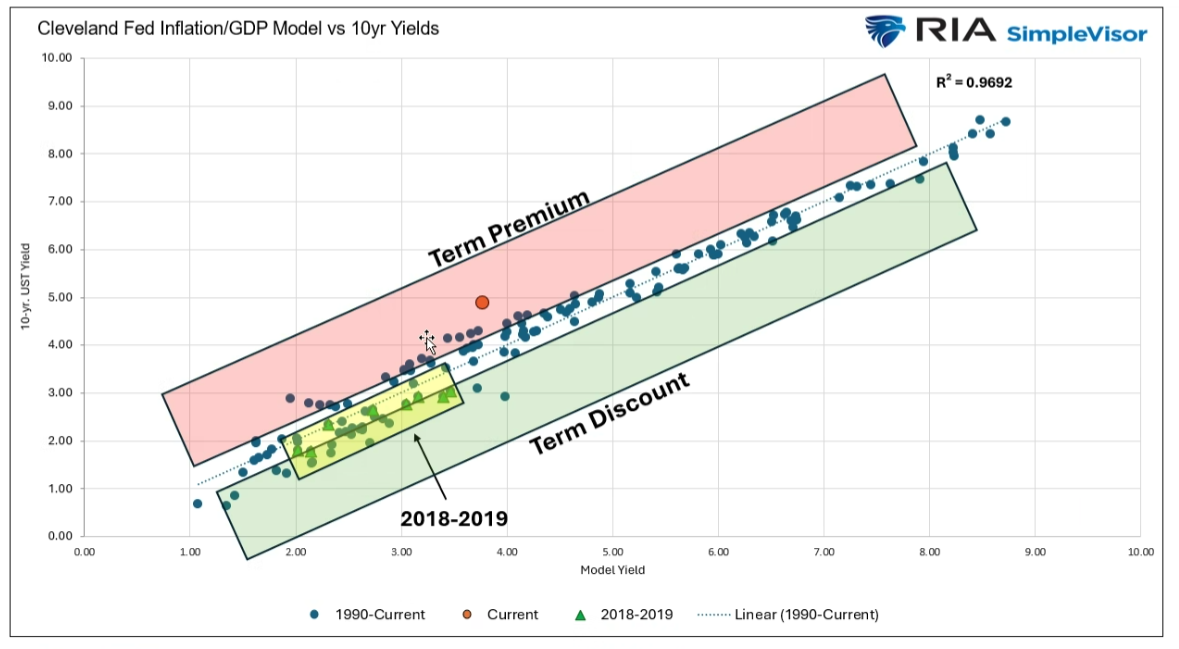

The following chart correlates the mannequin and presents the “time period” premium and low cost. The orange dot exhibits the place yields commerce at present relative to the mannequin, which is the very best in its 35-year historical past. Mike has additionally highlighted the 2018-2019 vary when the Trump Administration beforehand imposed tariffs. Whereas the bond market has offered off on fears of inflation from tariffs, the earlier interval resulted in decrease yields, not larger.

Nevertheless, within the close to time period, larger yields current an unappreciated market threat to the market and the economic system usually. Rates of interest are a operate of financial development and inflation. Inflation is a byproduct of financial development, which is curtailed by larger charges. Moreover, will increase in rates of interest negatively influence company earnings as borrowing prices enhance. Subsequently, whereas rising rates of interest don’t instantly impair earnings development, ultimately, they do as financial development slows.

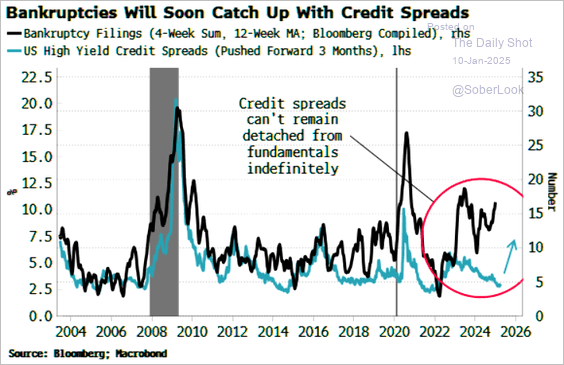

Provided that larger borrowing prices divert earnings into debt service, the damaging influence on companies is obvious in an economic system and monetary market supported by rising debt ranges. During the last two years, company bankruptcies have elevated sharply as borrowing prices have risen. Whereas credit score spreads have but to mirror this actuality, debtors will ultimately turn out to be extra “threat averse.” Because of this credit score spreads, as proven above, are an vital main indicator of market threat.

Lastly, valuations are a operate of earnings development and investor sentiment. Subsequently, fee will increase pose a big menace if earnings development turns into impaired resulting from larger prices and slowing financial demand. Traditionally, rising rates of interest have triggered extra important imply reverting occasions. It’s because traders should reprice belongings for decrease anticipated earnings development charges. With valuations on the highest degree for the reason that stimulus-induced frenzy in 2021, the chance of a reversion has elevated. Such is especially true if Wall Avenue’s bullish forecasts fail to turn out to be actuality.

The excellent news is that in financial and earnings contraction intervals, yields fall considerably because the markets are repriced to a brand new actuality. Such ultimately supplies the bottom for the subsequent bull market cycle.

However that will probably be a dialog for a later article.

Technicals Counsel Being Extra Tactically Bearish

Whereas there are actually some extra important macroeconomic considerations heading into 2025, the technical backdrop helps being extra “tactically bearish” into the brand new yr.

The next chart has offered a powerful foundation for our portfolio risk-management protocols through the years. It’s a weekly worth chart of the S&P 500 index exhibiting the present bullish worth pattern channel that began in 2009 on a logarithmic scale. At any time when that market has traded on the high or backside of that channel, it has been a big indication to start altering allocation ranges in portfolio fashions. The underside two panels are a brief—and longer-term weekly Shifting Common Convergence Divergence Indicator (MACD). Notably, the deviation of these indicators from the long-term norms post-2020 has been important because of the flood of stimulus and surge in market hypothesis. Notably, each indicators are topping and starting to sign a market warning. Whereas these indicators can stay elevated for a while, the market will probably be in a extra corrective course of when the tendencies turn out to be constantly decrease, as seen in 2022.

With the market nonetheless buying and selling above longer-term means, it’s not but time to sound the warning bell to scale back portfolio threat considerably. Nevertheless, given the mix of upper charges, extreme valuations, and the chance of slower earnings development, specializing in threat heading into 2025 appears prudent. Subsequently, it appears applicable to restate one thing I wrote the final time we noticed these divergences.

“Our job as traders is to navigate the waters inside which we at present sail, not the waters we expect we’ll sail in later. Larger returns come from the administration of ‘dangers’ relatively than the try and create returns by chasing markets. Robert Rubin, former Secretary of the Treasury, outlined this philosophy when he said;

‘As I believe again through the years, I’ve been guided by 4 rules for determination making. The one certainty is that there isn’t any certainty. Second, each determination, as a consequence, is a matter of weighing possibilities. Third, regardless of uncertainty, we should resolve and we should act. And lastly, we have to decide selections not solely on the outcomes but additionally on how we made them.

Most individuals are in denial about uncertainty. They assume they’re fortunate, and that the unpredictable will be reliably forecasted. Such retains enterprise brisk for palm readers, psychics, and stockbrokers, however it’s a horrible option to take care of uncertainty. If there are not any absolutes, all selections turn out to be issues of judging the chance of various outcomes, and the prices and advantages of every. Then, on that foundation, you can also make determination.’”

An Trustworthy Evaluation

For all of those causes, we have gotten extra “tactically bearish” as we ponder the outcomes of 2025. It must be evident that an sincere evaluation of uncertainty results in higher selections. Nonetheless, the advantages of Rubin’s strategy, and ours, transcend that. Though it could appear contradictory, embracing uncertainty reduces threat, whereas denial will increase it. One other good thing about acknowledging uncertainty is it retains you sincere.

“A wholesome respect for uncertainty and give attention to chance drives you by no means to be happy along with your conclusions. It retains you shifting ahead to hunt out extra data, to query typical pondering and to repeatedly refine your judgments and understanding that distinction between certainty and chance could make all of the distinction.” – Robert Rubin

We should acknowledge and reply to modifications in underlying market dynamics. If they modify for the more serious, we should concentrate on the inherent dangers in portfolio allocation fashions. The fact is that we will’t management outcomes. Essentially the most we will do is affect the chance of particular outcomes. Such is why we handle threat by investing in possibilities relatively than potentialities.

Such is important to capital preservation and funding success over time.

For extra in-depth evaluation and actionable funding methods, go to RealInvestmentAdvice.com. Keep forward of the markets with professional insights tailor-made that will help you obtain your monetary objectives.