{kind=link}

The CNN concern greed index of investor sentiment has fallen to “excessive concern” at 18 on a scale of 0 to 100. Furthermore, these expressing bearish sentiment within the AAII particular person investor survey are above 60%, which is simply the sixth time since 1987 that it has been that top. Watching CNBC or Bloomberg would possibly make you assume the inventory market is crashing or, at a minimal, extraordinarily risky. Statistically talking, neither is the case.

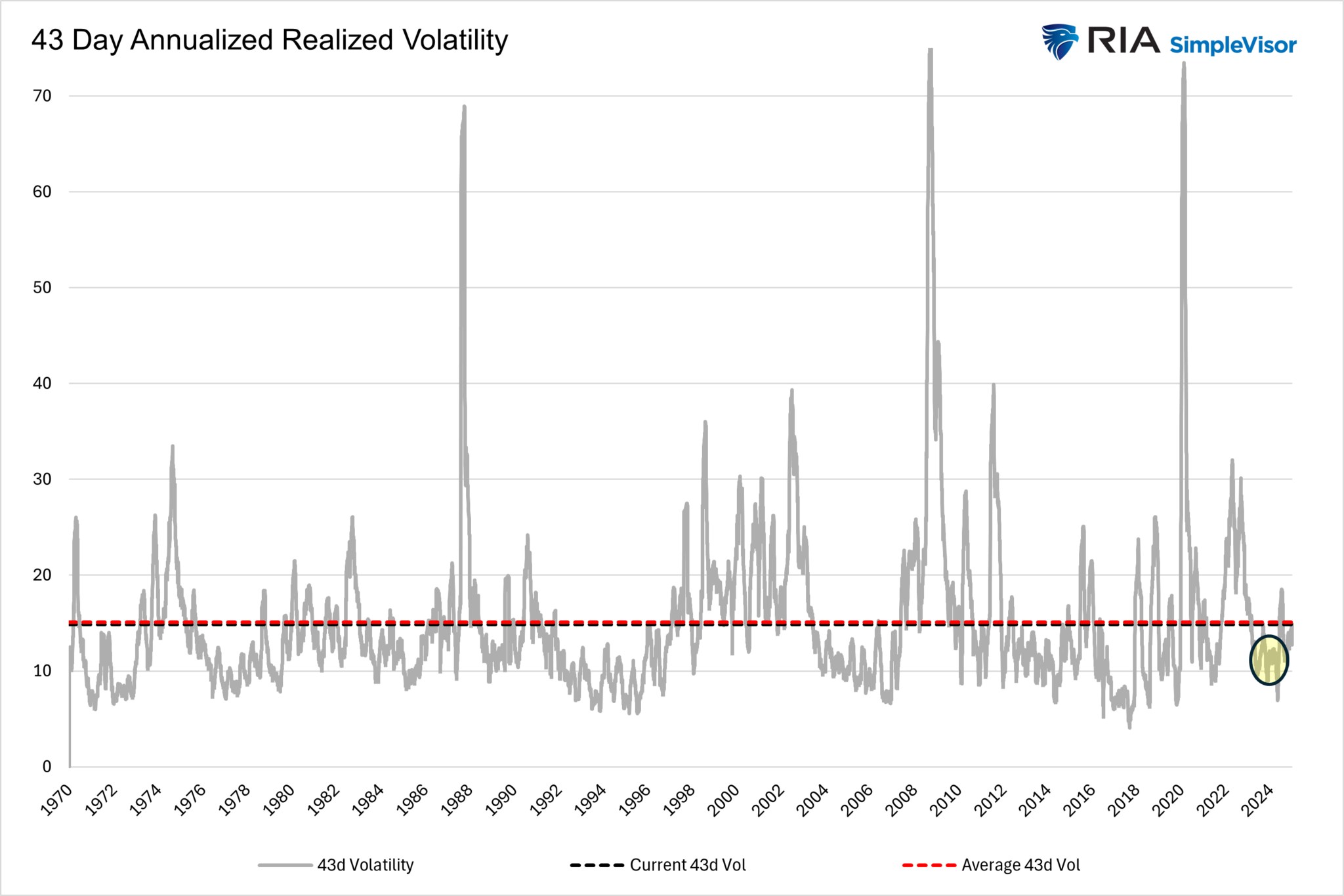

The next evaluation compares the S&P 500’s most up-to-date 43-day exercise (2025 YTD) to each different 43-day interval since 1970 and to these during the last two years (2023-2024). By way of Thursday, March sixth, the S&P 500 is down about 2.5%, hardly a crash. The 43-day annualized realized volatility throughout this era is 14.8, which is definitely a hair under the typical of 15.07 since 1970. Nevertheless, it’s decently elevated from the 12.95 common during the last two years.

Our takeaway from this evaluation is that latest market conduct is traditionally typical. Nevertheless, we had been lulled to sleep with low volatility during the last two years, so the latest buying and selling patterns appear extra excessive than they’re.

What To Watch Right now

Earnings

Economic system

Market Buying and selling Replace

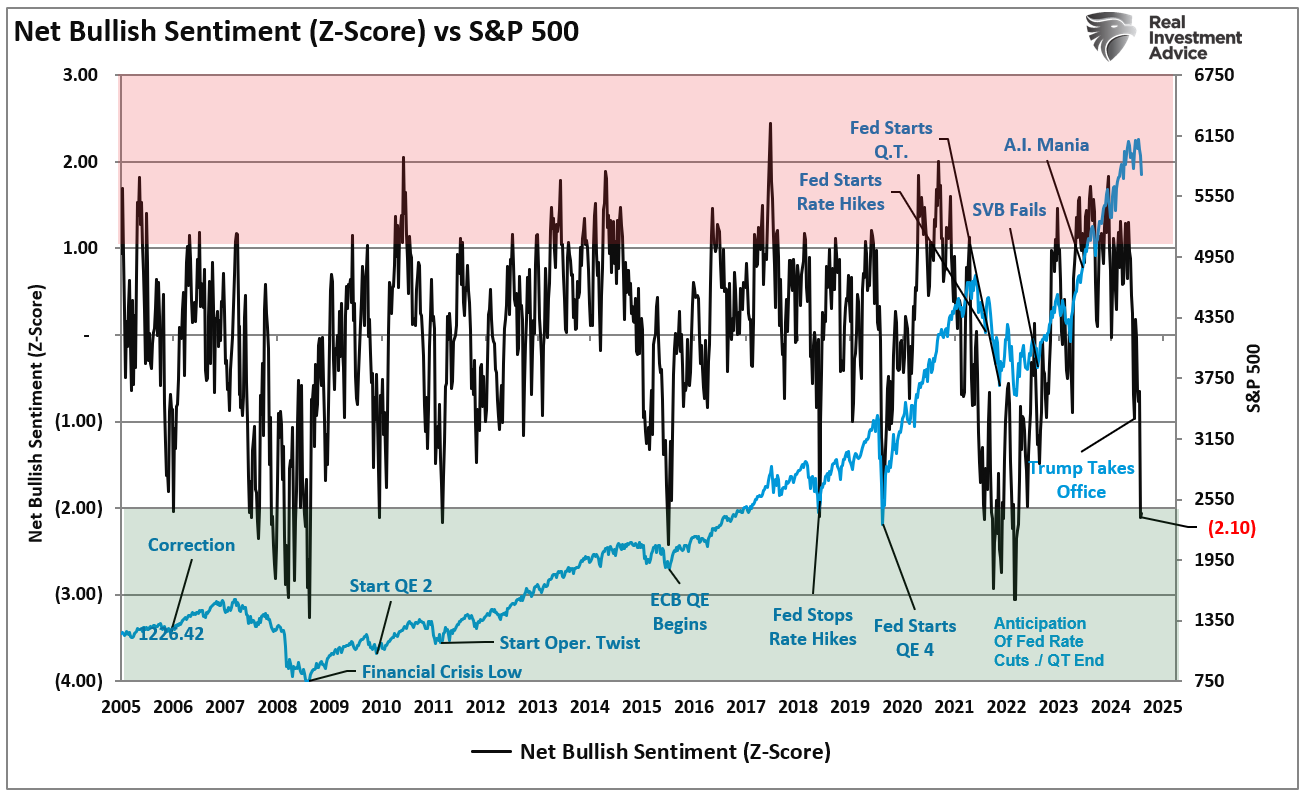

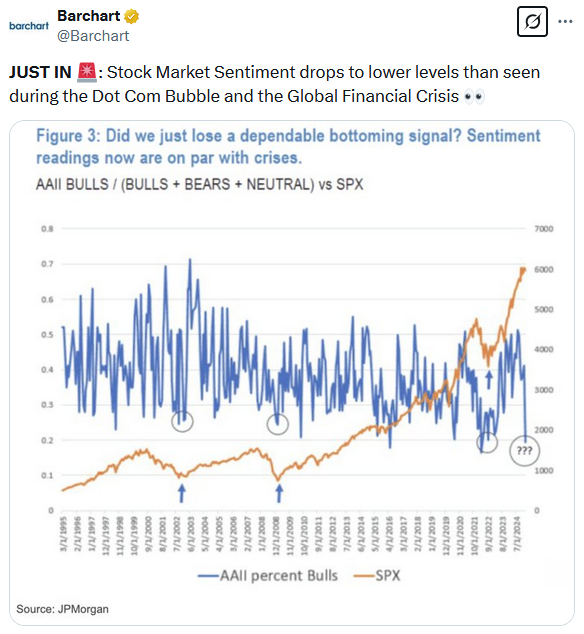

Final week, we mentioned the extra excessive ranges of bearishness which have gripped the markets as of late.

“In different phrases, whereas the media scrambled to align causes with the sell-off, the correction was very a lot consistent with seasonal tendencies. Crucially, that sell-off has pushed investor sentiment to ranges usually equating to a lot deeper corrections. From a contrarian view, that excessive adverse sentiment, now mixed with oversold situations, gives base for a rally in March.”

“Sentiment is approaching two normal deviations under its common degree. Such ranges are extra coincident with market bottoms than the start of a corrective cycle. I’ve labeled some occasions alongside the way in which. The lesson is that headlines drive sentiment, and when sentiment turns into too adverse, as could be the case immediately, such permits for rallies to type.”

The sentiment chart has been up to date, exhibiting that bearish sentiment reached much more profound ranges of negativity and is greater than two normal deviations under the norms.

Nevertheless, regardless of the deep ranges of negativity, the present correction is properly throughout the context of the volatility seen throughout Trump’s first time period as he engaged in a commerce with China. We’ll talk about this extra momentarily.

Whereas Trump’s tariffs and bearish headlines presently dominate buyers’ psychology, we should keep in mind that corrections are a traditional market operate. Sure, the market is down roughly 7% from the height, however we’ve got seen these corrections repeatedly previously. That does NOT imply a extra intensive corrective course of just isn’t doubtlessly in course of. It solely implies that markets are probably able for a technical rally to reverse the extra excessive oversold situations.

The purpose is to recollect the way you felt throughout these corrections and what actions you took. Had been they the proper actions? In the event that they weren’t, then why are you doubtlessly repeating previous errors?

Volatility is the value we pay to take a position. The exhausting half is avoiding volatility’s behavioral impacts on our investing outcomes.

Employment & The Week Forward

The BLS jobs report was good on the floor however problematic when you dig into it. Most regarding to us is the broader measure of the unemployment charge, the U6 and the family survey. Per the BLS, the U6 contains all these within the unemployment charge, plus:

All Individuals Marginally Hooked up to the Labor Drive, Plus Whole Employed Half Time for Financial Causes, as a P.c of the Civilian Labor Drive Plus All Individuals Marginally Hooked up to the Labor Drive

The U6, proven under, rose from 7.5% to eight%, regardless of the unemployment charge (U3) solely rising .1% to 4.1%. Keep in mind, the Fed focuses on U3, not U6, so this job report is unlikely to overly concern the Fed. Nevertheless, most federal worker and contractor layoffs occurred after the BLS reference week, so the preliminary affect of DOGE cuts has but to be seen. Consequently, the March report can be extra vital. Additionally of concern is that the family employment survey fell by 588k jobs in February, the most important drop since December 2023.

We’ll get yet one more piece of job knowledge with the JOLTs report on Tuesday. CPI and PPI, on Wednesday and Thursday, respectively, would be the key knowledge factors this week. The market expects CPI to extend by 0.3% after rising by 0.4% final month. Additionally of notice this week is the NFIB Small Enterprise Optimism Index on Tuesday. The Fed can be quiet as they enter their media blackout upfront of their March nineteenth FOMC assembly.

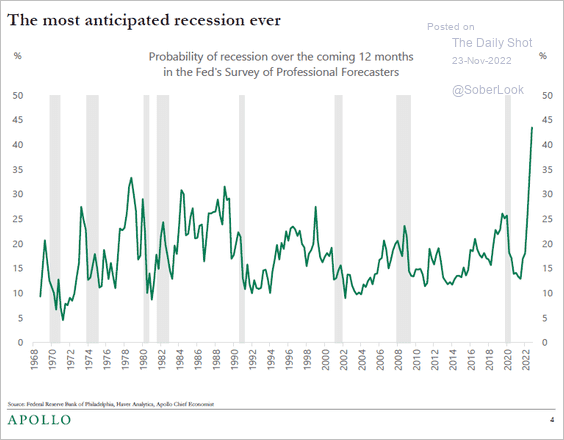

The Threat Of A Recession Isn’t Zero

The danger of a recession within the U.S. just isn’t zero. That is notably true as the present Administration tackles Authorities bloat and implements tariffs. Nevertheless, earlier than we talk about why the danger of a recession might improve, it’s essential to recollect the 2022 expertise. At the moment, most economists had been satisfied a “recession was imminent.” As mentioned in early 2023, it was essentially the most anticipated recession ever.

Tweet of the Day

“Wish to obtain higher long-term success in managing your portfolio? Listed below are our 15-trading guidelines for managing market dangers.”

Please subscribe to the day by day commentary to obtain these updates each morning earlier than the opening bell.

When you discovered this weblog helpful, please ship it to another person, share it on social media, or contact us to arrange a gathering.