{kind=link}

Inside This Week’s Bull Bear Report

- Trump Election Sends NFIB Optimism Surging

- How We Are Buying and selling It

- Analysis Report – Financial Indicators And Earnings Expectations

- Youtube – Earlier than The Bell

- Market Statistics

- Inventory Screens

- Portfolio Trades This Week

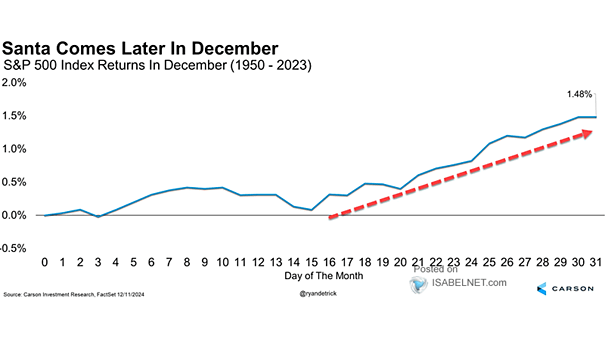

First Comes The Fed, Then Santa

Final week, we mentioned that the chance to the markets was the annual portfolio rebalancing course of. To wit:

“With the year-end approaching, portfolio managers must rebalance their holdings as a consequence of tax concerns, distributions, and annual reporting. For instance, as of this writing, the S&P 500 is at the moment up about 28% year-to-date, whereas investment-grade bonds (as measured by iShares US Combination Bond ETF (AGG) are up 3.2%. That differential in efficiency would trigger a 60/40 inventory/bond allocation to shift to a 65/35 allocation. To rebalance that portfolio again to 60/40, portfolio managers should cut back fairness publicity by 5% and improve bond publicity by 5%. Relying on the magnitude of the rebalancing course of, it may exert downward strain on threat belongings, resulting in a short-term market correction or consolidation.”

That definitely appeared the case this previous week, with the market buying and selling being pretty sloppy. Makes an attempt to push the market increased have been repeatedly met with sellers, and we noticed a rotation from over-owned to under-owned belongings. Notably, that promoting strain arrived as anticipated, and whereas such may persist till early subsequent week, we needs to be getting near the top of the distribution and rebalancing course of. The excellent news is that the latest consolidation paves the way in which for “Santa Claus to go to Broad and Wall.”

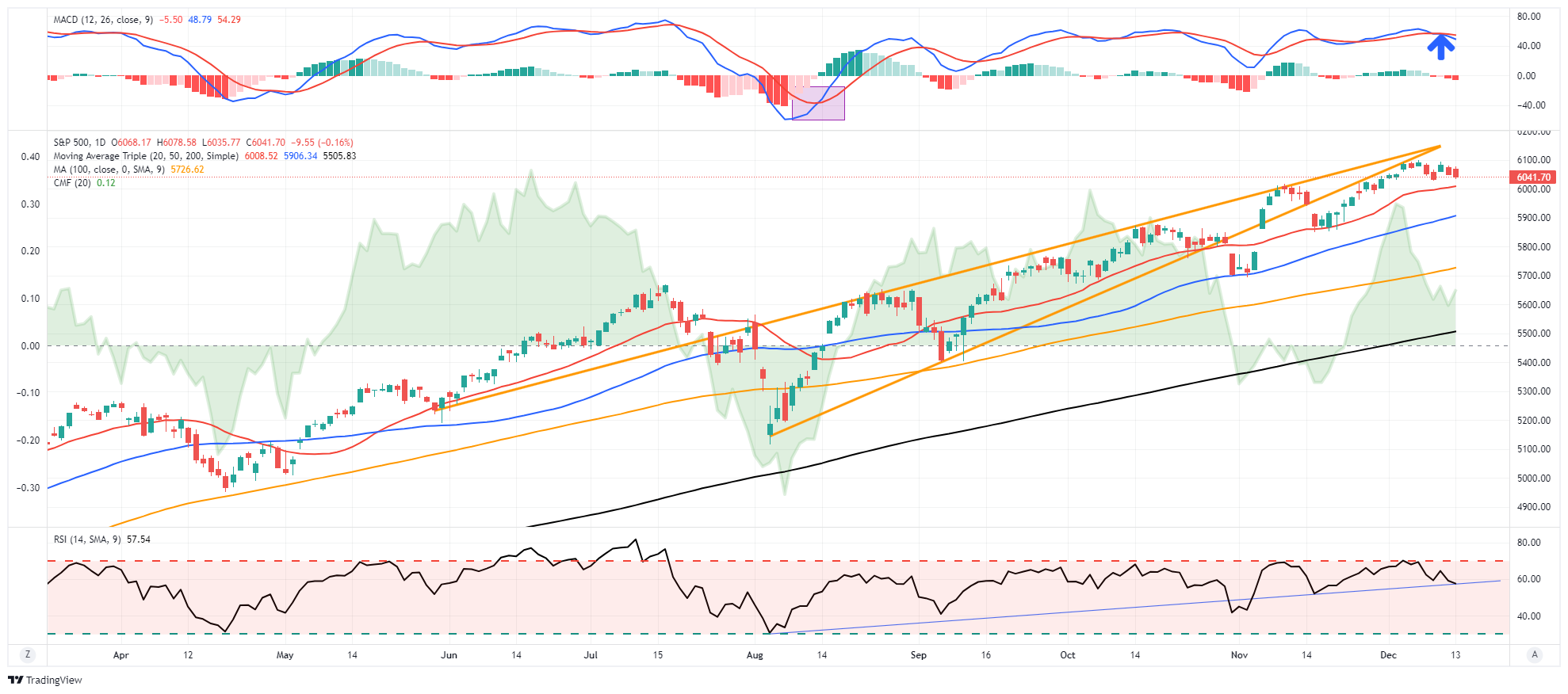

Technically talking, the market did register a short-term MACD promote sign final week, which may exert additional downward strain on shares into subsequent week. With relative energy not oversold, there’s some threat of the market declining towards the 20-DMA by the point the Fed pronounces its subsequent charge reduce on Wednesday. Nevertheless, barring any surprising occasions, the market ought to be capable to rally into year-end with a goal of 6100 to 6150.

Quick-term forecasts all the time have dangers, so we propose managing threat accordingly. Nevertheless, the seasonal tendencies, present bullish sentiment, and share buybacks proceed to favor increased costs into the primary week of 2025. After that, all bets are off as a brand new administration, govt actions, and the primary 100 days of policymaking will set the stage for market expectations subsequent 12 months. As famous final week, optimism is exceptionally excessive. Nonetheless, a radical transformation of Authorities, which shall be nice in the long run, doesn’t come with out short-term financial and monetary. dangers.

Talking of optimism, we are going to evaluate small enterprise house owners and what that probably means for the financial system this week.

Want Assist With Your Investing Technique?

Are you searching for full monetary, insurance coverage, and property planning? Want a risk-managed portfolio administration technique to develop and defend your financial savings? No matter your wants are, we’re right here to assist.

A Fast Historical past Lesson

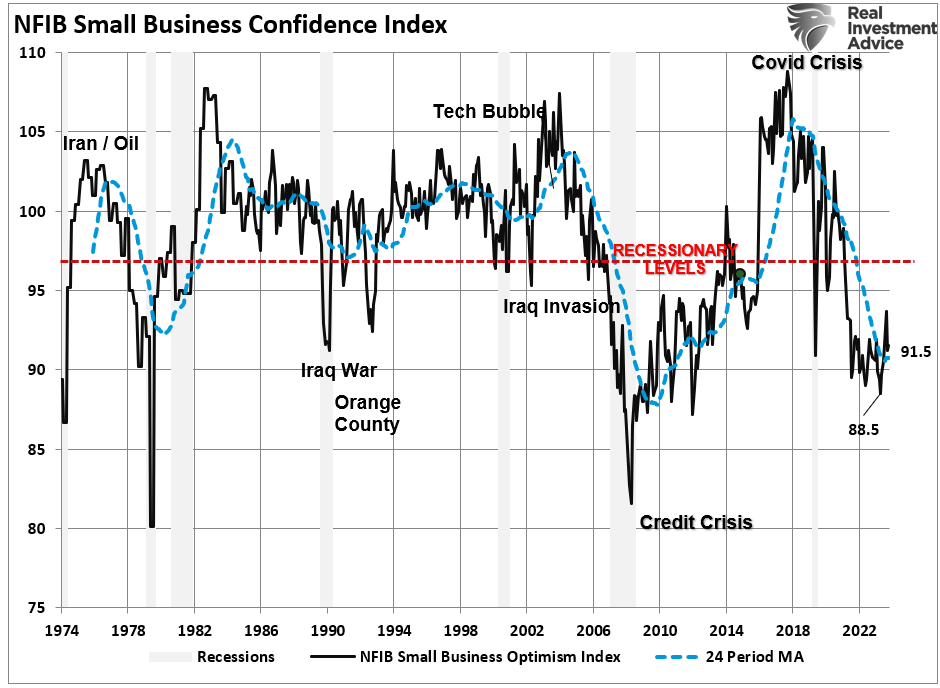

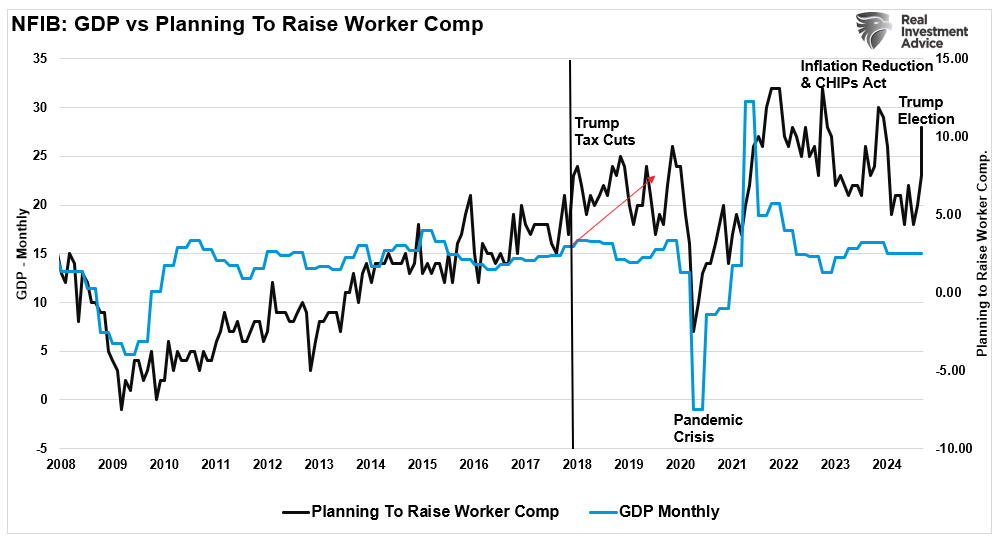

During the last a number of years, we have now often mentioned the significance of the Nationwide Federation Of Unbiased Enterprise Survey (NFIB) in regards to the financial system. As famous in our most up-to-date replace (October twelfth) on the index:

“Whereas Wall Avenue’s bullish narrative is compelling, the most recent information from the NFIB Small Enterprise Optimism Index gives a stark distinction. Small companies are the spine of the U.S. financial system, and the sentiment captured within the NFIB survey gives a extra granular view of the challenges dealing with Major Avenue, which regularly diverges from Wall Avenue’s broader outlook. The index stays at ranges extra usually related to financial contractions than expansions.”

As famous, that article was posted earlier than Trump’s election in November. At the moment, sentiment was broadly detrimental relating to every little thing from the outlook on gross sales to employment. Provided that retail gross sales comprise roughly 40% of Private Consumption Expenditures (PCE) which make up almost 70% of the GDP calculation, small companies are an necessary driver of the financial system. As famous in October:

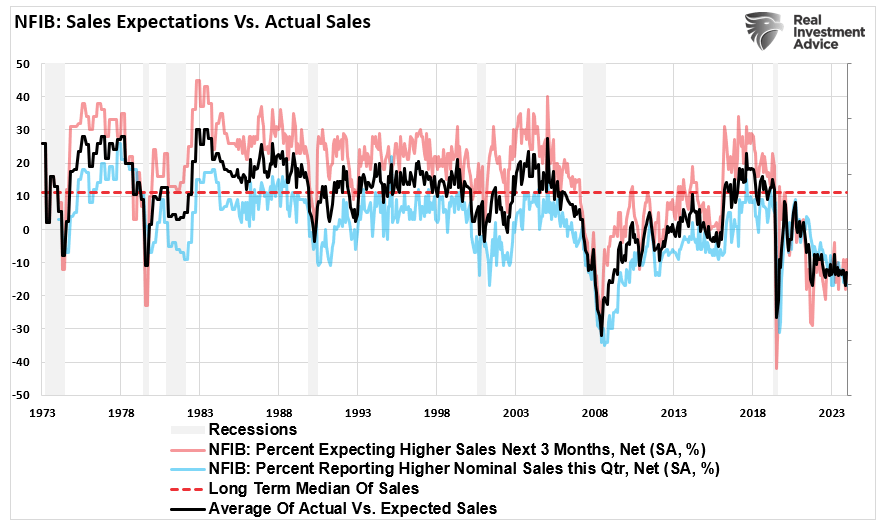

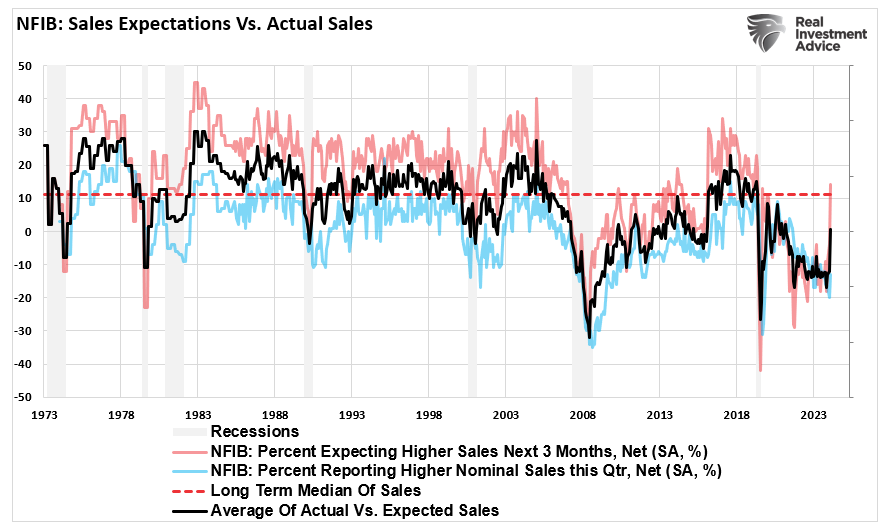

“One of many extra troubling elements of the NFIB survey is the outlook for future gross sales. In keeping with the information, many small enterprise house owners anticipate gross sales to say no over the following six months. This pessimism is especially pronounced within the retail and repair sectors, the place rising prices and shrinking revenue margins power many companies to cut back their operations. The survey gives two fascinating elements: precise gross sales over the last quarter and anticipated gross sales within the upcoming quarter. Often, enterprise house owners are all the time extra optimistic about future gross sales regardless of precise gross sales typically extra disappointing. Nevertheless, each anticipated and precise gross sales are at the moment dismal, as proven by the typical of the 2 measures.”

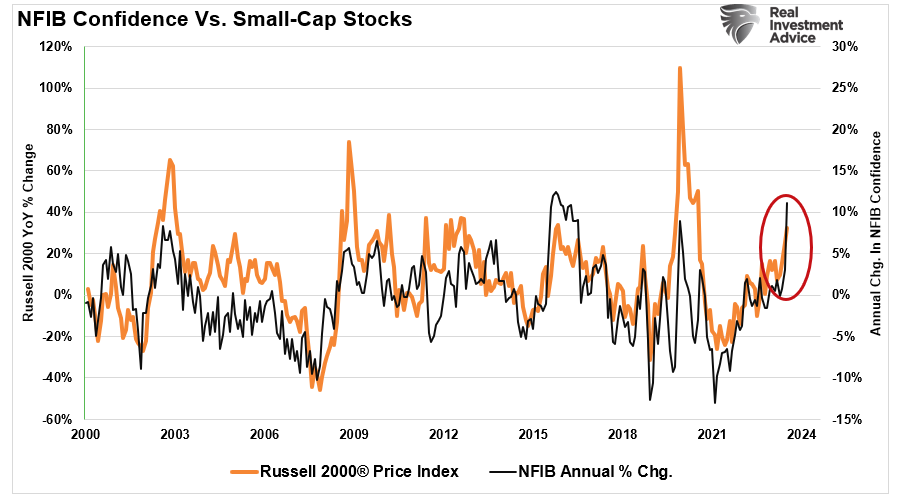

Then, on November eighth, in our Each day Market Replace, we mentioned Trump’s election and its potential influence on small and mid-capitalization corporations. To wit:

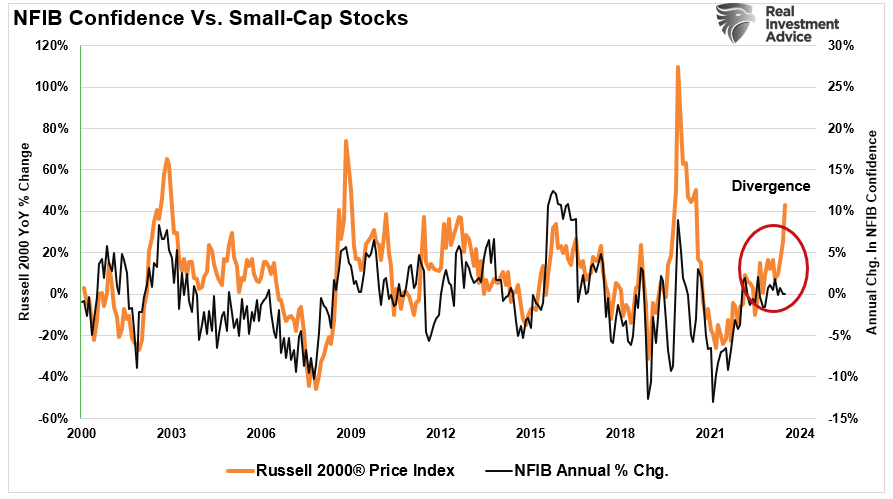

“Notably, the large surge in small/mid-cap shares was probably the most compelling. The chart under reveals a really excessive correlation between small/mid-cap shares’ annual charge of change and the NFIB small enterprise confidence index. Since enterprise house owners are inclined to lean conservative, favoring insurance policies that promote financial progress, lowered laws, and tax cuts, Trump’s election helps enterprise house owners.

We suspect that the following iteration of the NFIB index shall be a catchup transfer fueled by an explosion of enterprise house owners’ confidence. This could result in will increase in CapEx spending, employment, and wage progress.“

The explanation for the short historical past lesson comes all the way down to the final sentence.

NFIB Index Surges On Trump’s Election

Early this week, the NFIB launched its newest small enterprise confidence index. I’m uncertain that “explosion” totally encapsulates the transfer we noticed following Trump’s election. Nevertheless, because the saying goes, “an image is price a thousand phrases.”

The greater than 10-point soar within the studying is astonishing and one thing we haven’t seen since Trump’s election in 2016. After remaining at ranges usually related to recessionary economies during the last three years, the most recent studying suggests a massively constructive shift in enterprise house owners’ outlooks. That shift is a operate of expectations in a number of areas:

- Tax charges won’t rise because the Tax Cuts And Jobs Act of 2017 shall be made everlasting.

- There’s a potential that company tax charges could possibly be reduce from 21% to fifteen%.

- A discount in regulatory overreach from the earlier administration.

- The discount of unlawful immigration and the establishment of authorized pathways for immigration.

- A reversal of the abandonment of the “rule of legislation.”

- A shift in insurance policies that can assist U.S.-based companies and encourage home manufacturing.

- Expedited allowing for U.S.-based enterprise improvement investments.

Whereas these insurance policies are designed to assist U.S.-based companies, they current some dangers that shouldn’t be neglected. For instance, whereas company tax cuts and deregulation could improve profitability and funding, commerce insurance policies and immigration restrictions may introduce challenges corresponding to elevated prices and labor shortages. As such, small companies, particularly, might want to navigate these dynamics to leverage potential advantages whereas mitigating related dangers.

Nevertheless, for now, the shift in constructive sentiment is mirrored in lots of expectations from employment to gross sales. Let’s study just a few of the necessary ones.

Financial Outlook

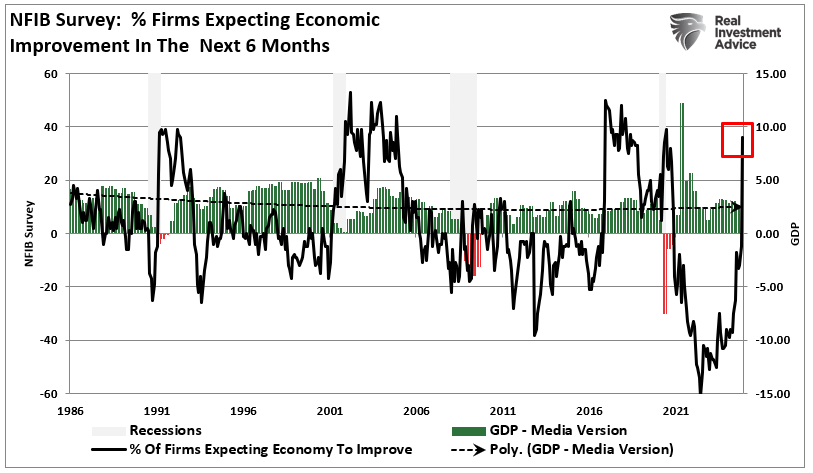

A symbiotic hyperlink exists between the assorted NFIB survey information and potential financial outcomes. Because the Trump election, the variety of small enterprise corporations anticipating financial enchancment has surged. Such a surge was additionally seen following Trump’s election in 2016. Notably, whereas the spike lasted for a while, it will definitely started to reverse for 2 causes. First, whereas financial progress did initially enhance, it didn’t develop as strongly as was anticipated. Secondly, as famous above, whereas small companies are optimistic concerning the “proposed” insurance policies, precise enactment and offsetting dangers of 1 coverage over one other (i.e., tariffs versus deregulation) muted the result.

Whereas Trump will possible not face one other “pandemic-related” disaster over the following 4 years, many different potential dangers, from financial recession to credit-related occasions, may influence future expectations.

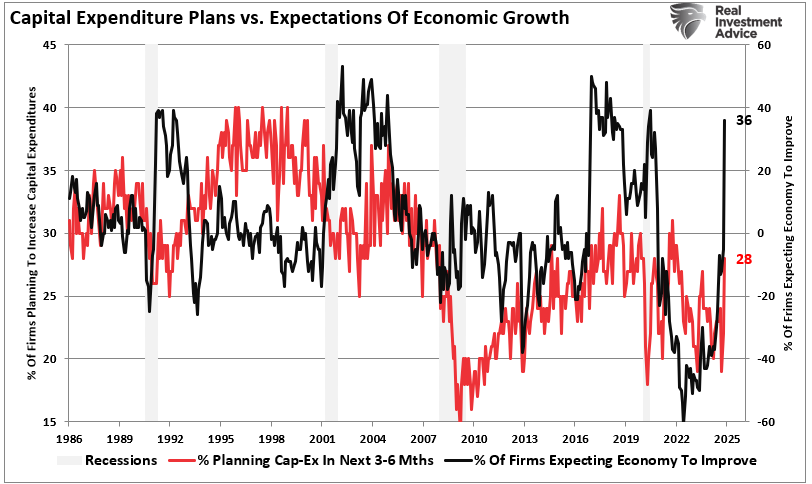

Nonetheless, within the close to time period, the surge in expectations for financial progress will possible “loosen the purse strings” of small enterprise house owners to extend capital expenditures. Capital expenditures, or CapEX, are included within the “non-public funding” element of the GDP calculation. Unsurprisingly, there’s a correlation between financial progress and CapEx. Because the financial system grows, derived from shopper demand, companies should make investments to extend manufacturing. Subsequently, if present expectations are for the financial system to develop over the following 6-months, it’s logical that expectations for CapEx would additionally improve.

Given the influence of small companies CapEx plans on the financial system, we should always anticipate financial progress to extend in the event that they comply with by means of with these plans. Notably, the expectation enchancment suggests an additional decline in recession dangers into 2025.

Crucially, if small companies anticipate financial enchancment, which helps the necessity to improve CapEx, in addition they anticipate sizable will increase in gross sales and employment.

Elevated Gross sales And Employment

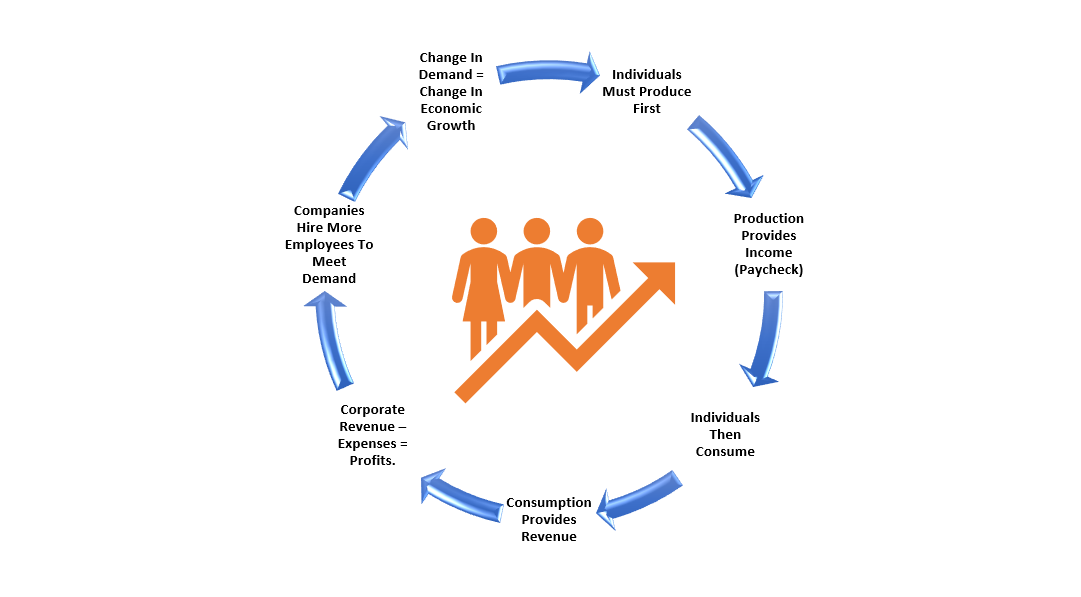

There’s a very fundamental diagram that explains our financial system. In a consumption-based financial system, just like the U.S., people should produce one thing first to eat. That consumption is the demand facet of the financial equation, to which producers create the availability. The extra demand within the financial system, the extra manufacturing is required. That demand for manufacturing drives employment and wages.

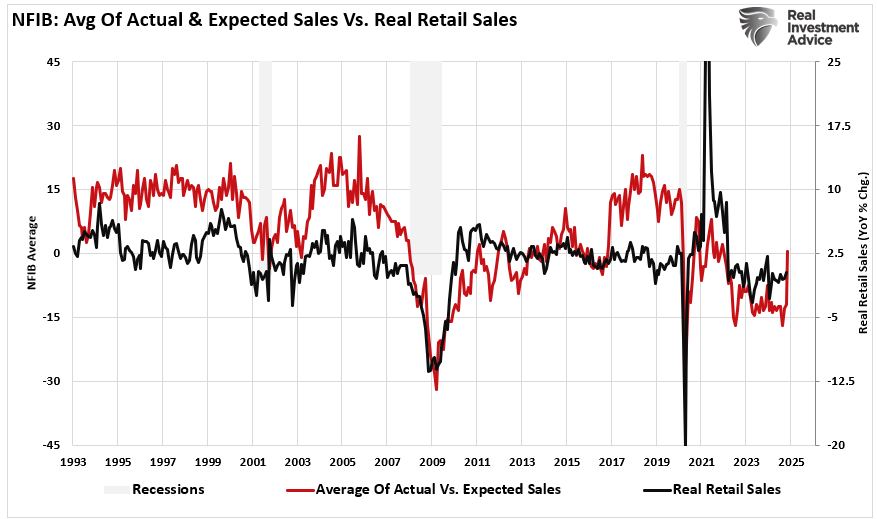

Understanding the surge in financial progress expectations since Trump’s election aligns with a pointy improve in future gross sales expectations. Each anticipated and precise gross sales have been beforehand at ranges that all the time aligned with financial recessions. Nevertheless, because the election, gross sales expectations have climbed sharply. What shall be essential to the financial system is to see ACTUAL gross sales improve into 2025. Whereas traditionally, there was a deviation between precise and anticipated gross sales; if gross sales don’t improve from present ranges, neither will financial progress charges.

Whereas the NFIB survey could be very optimistic about future gross sales, it’s price noting that precise (inflation-adjusted) retail gross sales, as reported by the BEA, whereas correlated, are sometimes much less optimistic. Given the present state of the patron, elevated rates of interest, and better charges of inflation, we are going to possible see some disappointment in future NFIB gross sales expectations.

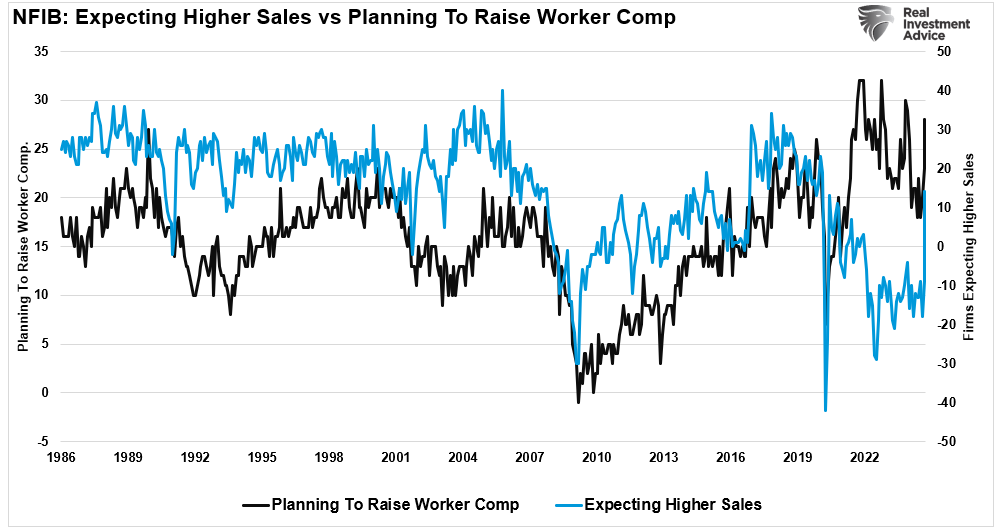

Nevertheless, for now, if small enterprise house owners anticipate a rise in gross sales, such can even result in extra demand for hiring and a rise in wages. Once more, it needs to be evident that gross sales will increase end in increased wages.

Lastly, to complete the financial cycle, gross sales (demand) improve manufacturing (provide), requiring increased wages and employment and facilitating extra demand. That is the idea of the financial progress cycle.

If the optimism since Trump’s election seems to be well-founded, it may bode effectively for small and mid-capitalization shares at the very least early into 2025.

Small Cap Shares – Look At Me Now

As I famous on the outset, there was beforehand a reasonably vital hole between small and mid-capitalization shares, as represented by the iShares Russell 2000 Index (IWM) and the annual change within the NFIB index. Given the historic correlation, one would ultimately meet up with the opposite. On this case, the market anticipated a Trump win, with IWM working effectively forward of NFIB sentiment. Because the election, that hole has now closed, with sentiment surging increased.

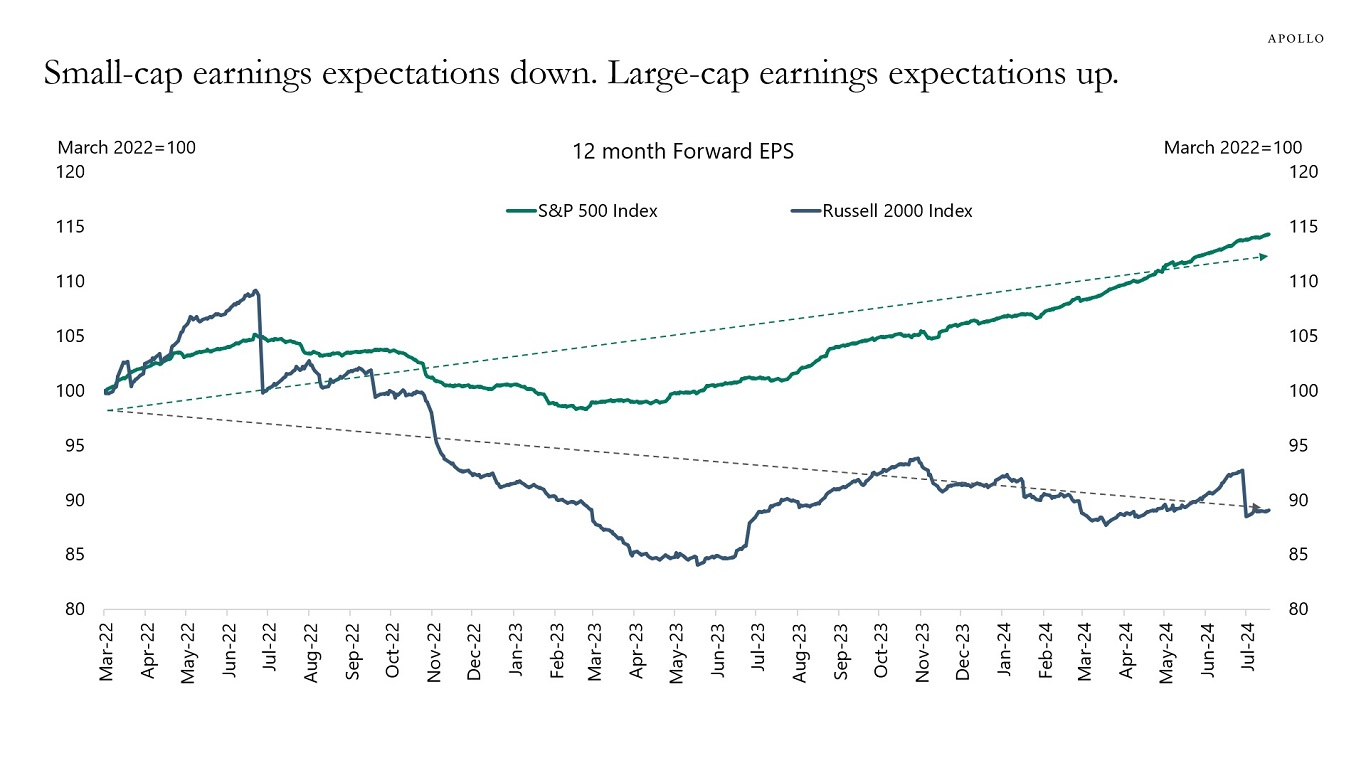

Whereas small and mid-capitalization shares have surged increased in latest weeks, many dangers nonetheless plague these corporations going ahead. As famous beforehand, roughly 41% of those unprofitable corporations are closely indebted, with a maturity wall approaching over the following two years. If rates of interest stay elevated, such may weigh on each refinancing functionality and profitability, resulting in a pickup in default charges. The issue with surging expectations for financial progress, employment, and wages is that such will maintain inflation and better rates of interest.

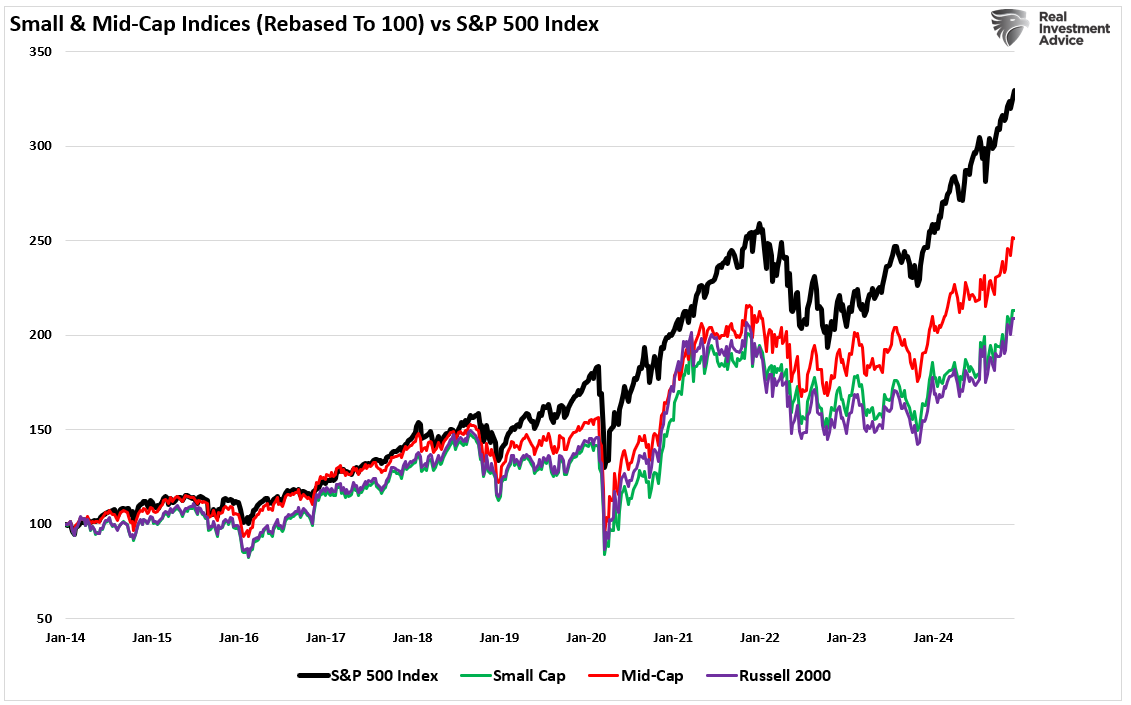

Moreover, the long-term efficiency of small and mid-capitalization shares stays dismal, as proven.

May that change sooner or later? Sure. Nevertheless, such would require a reset in earnings progress expectations, possible following the following recession. For now, most earnings progress stays attributed to massive capitalization corporations and primarily only a small subset of these shares. Whereas we may see a pickup in total financial exercise, there’s a threat that it’ll not translate to small and mid-capitalization corporations.

Although shopper and enterprise house owners’ confidence has surged since Trump’s election, we should proceed to observe the incoming information and alter our threat preferences accordingly. Whereas the brand new administration definitely has many formidable plans to “Make America Nice Once more,” the fact stays that many of those plans could not come to fruition. There can even possible be offsetting forces between insurance policies, and the debt and deficits are nonetheless a longer-term downside weighing on financial progress trajectories. Most significantly, whereas the U.S. is producing financial progress at the moment, the remainder of the world is just not. As such, we usually tend to import financial weak spot over the following 12 months reasonably than export progress.

We stay optimistic and allotted to equities within the close to time period. Nevertheless, we understand that the extra extreme optimism about 2025 comes at a threat. Many issues may derail these expectations and the market, so we should stay targeted on the information because it presents itself.

With the S&P 500 up almost 30% this 12 months and a greater than 20% return final 12 months, tempering expectations for returns in 2025 appears prudent.

How We Are Buying and selling It

With portfolio rebalancing possible largely behind us, there’s nonetheless a threat of some sloppy motion earlier than Christmas. Nevertheless, we have to begin fascinated with making ready for the year-end “window dressing” motion often known as the “Santa Claus Rally.”

If you’re lengthy equities within the present market, rebalancing threat is manageable.

- Tighten up stop-loss ranges to present assist ranges for every place.

- Hedge portfolios in opposition to main market declines.

- Take earnings in positions which were massive winners

- Promote laggards and losers

- Increase money and rebalance portfolios to focus on weightings.

Keep in mind, our job as buyers is fairly easy – defend our funding capital from short-term destruction so we will play the long-term funding sport. Listed below are our ideas on this.

- Capital preservation is all the time the first goal. In the event you lose your capital, you might be out of the sport.

- Search a charge of return enough to preserve tempo with the inflation charge. Don’t give attention to beating the market.

- Preserve expectations primarily based on practical targets. (The market doesn’t compound at 8%, 6% or 4%)

- Larger charges of return require an exponential improve within the underlying threat profile. This tends to by no means work out effectively.

- You possibly can exchange misplaced capital – however you may’t exchange misplaced time. Time is a valuable commodity that you just can not afford to waste.

- Portfolios are time frame particular. If in case you have a 5-year retirement horizon however construct a portfolio with a 20-year time horizon (taking up extra threat), the outcomes will possible be disastrous.

There may be a variety of potential outcomes, primarily based on valuations, in 2025. Nobody is aware of with any certainty what subsequent 12 months will maintain. Nevertheless, by specializing in threat controls and the technical underpinnings, we will safely navigate the waters to security.

Be at liberty to succeed in out if you wish to navigate these unsure waters with professional steering. Our staff focuses on serving to purchasers make knowledgeable selections in as we speak’s risky markets.

Have an incredible week.

Analysis Report

Subscribe To “Earlier than The Bell” For Each day Buying and selling Updates

Now we have arrange a separate channel JUST for our brief each day market updates. Please subscribe to THIS CHANNEL to obtain each day notifications earlier than the market opens.

Click on Right here And Then Click on The SUBSCRIBE Button

Subscribe To Our YouTube Channel To Get Notified Of All Our Movies

Bull Bear Report Market Statistics & Screens

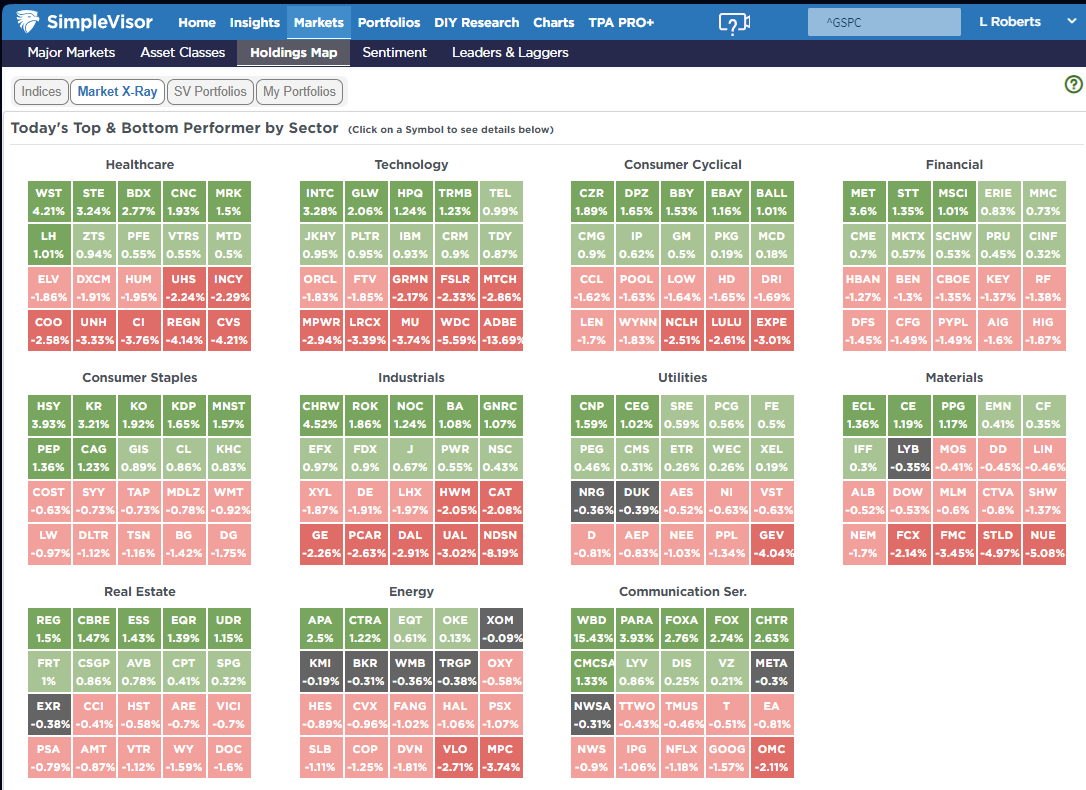

SimpleVisor High & Backside Performers By Sector

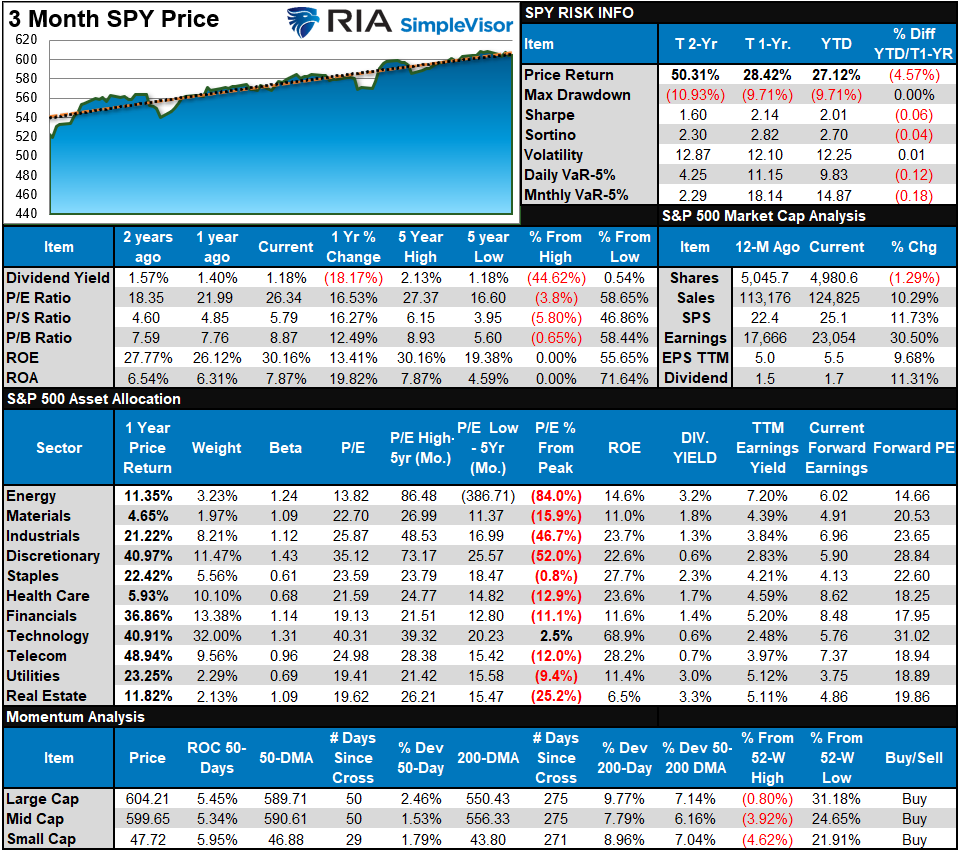

S&P 500 Weekly Tear Sheet

Relative Efficiency Evaluation

In final week’s e-newsletter, we famous that this previous week could be when mutual fund rebalancing begins, which may result in elevated volatility and sloppy buying and selling motion. With the index overbought together with know-how, discretionary, and bonds, a pullback in these belongings could be unsurprising. We noticed a lot of that rebalancing happen as anticipated, and now the market is usually oversold, excluding know-how, discretionary, and communications, that are pushed by the “Magnificent 7.” Whereas we may see a bit extra sloppiness beginning the week, managers ought to begin “window dressing” portfolios by Wednesday for year-end reporting. Such will possible assist the “Santa Claus” rally, and with the market remaining bullishly biased, growing fairness threat into year-end is doable. Don’t overlook to handle your threat in that course of, “simply in case.”

Technical Composite

The technical overbought/bought gauge contains a number of value indicators (R.S.I., Williams %R, and many others.), measured utilizing “weekly” closing value information. Readings above “80” are thought-about overbought, and under “20” are oversold. The market peaks when these readings are 80 or above, suggesting prudent profit-taking and threat administration. One of the best shopping for alternatives exist when these readings are 20 or under.

The present studying is 86.43 out of a potential 100.

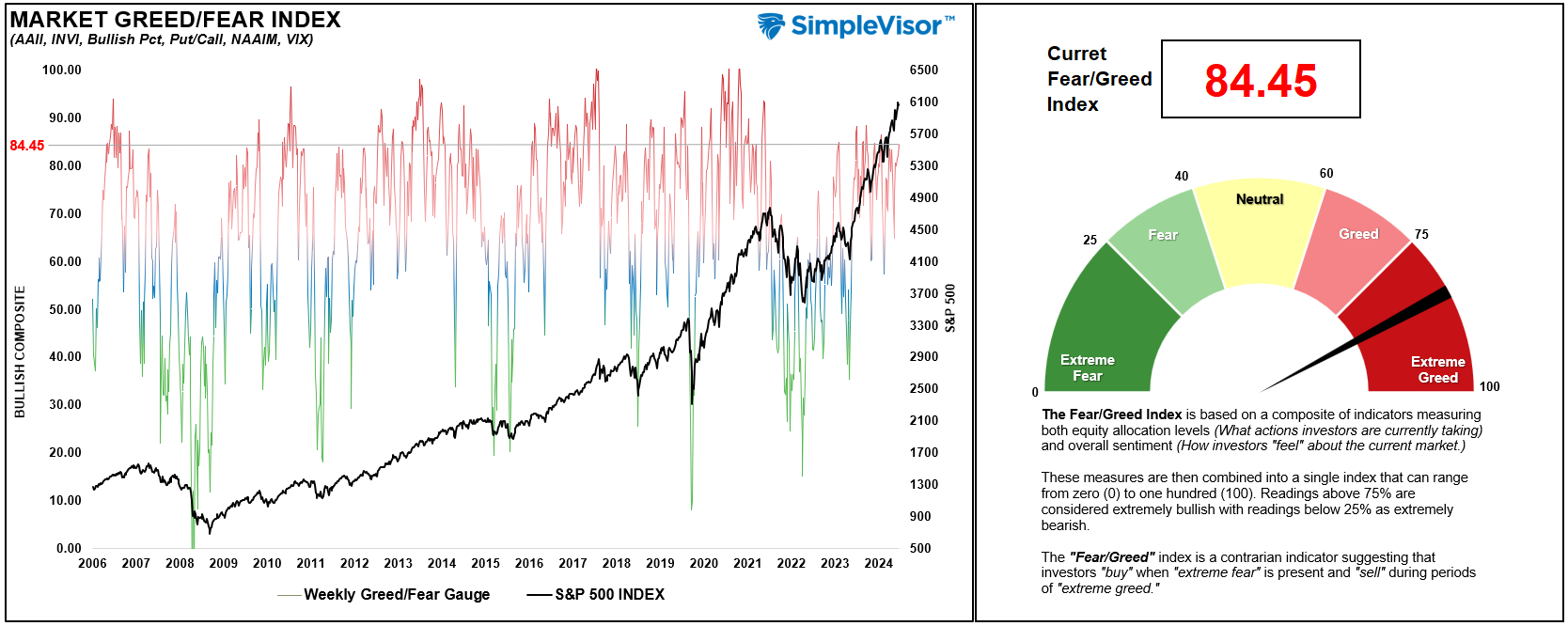

Portfolio Positioning “Worry / Greed” Gauge

The “Worry/Greed” gauge is how particular person {and professional} buyers are “positioning” themselves available in the market primarily based on their fairness publicity. From a contrarian place, the upper the allocation to equities, the extra possible the market is nearer to a correction than not. The gauge makes use of weekly closing information.

NOTE: The Worry/Greed Index measures threat from 0 to 100. It’s a rarity that it reaches ranges above 90. The present studying is 84.45 out of a potential 100.

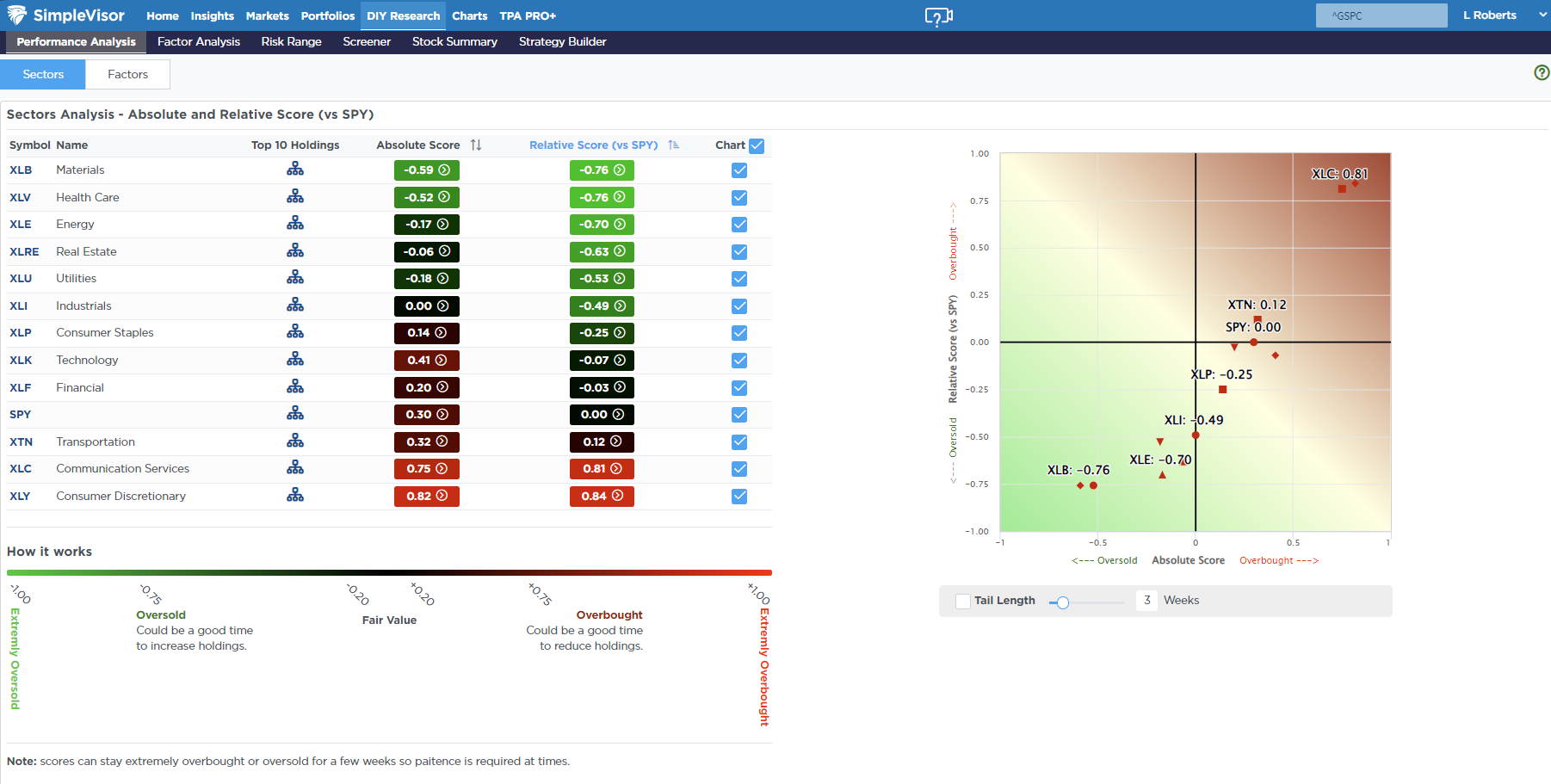

Relative Sector Evaluation

Most Oversold Sector Evaluation

Sector Mannequin Evaluation & Threat Ranges

How To Learn This Desk

- The desk compares the relative efficiency of every sector and market to the S&P 500 index.

- “MA XVER” (Transferring Common Crossover) is set by the short-term weekly shifting common crossing positively or negatively with the long-term weekly shifting common.

- The danger vary is a operate of the month-end closing value and the “beta” of the sector or market. (Ranges reset on the first of every month)

- The desk reveals the worth deviation above and under the weekly shifting averages.

The sell-off this previous week took a majority of sectors, together with bonds, effectively under their month-to-month threat ranges. Such units up these sectors, together with bonds, for a rally into year-end as portfolio window costume their portfolios for year-end reporting. We mentioned beforehand that a lot of the buying and selling motion this previous week could be on the draw back because of the want for funds to make annual distributions and full tax loss promoting for year-end. That has largely been accomplished, giving the market room to rally.

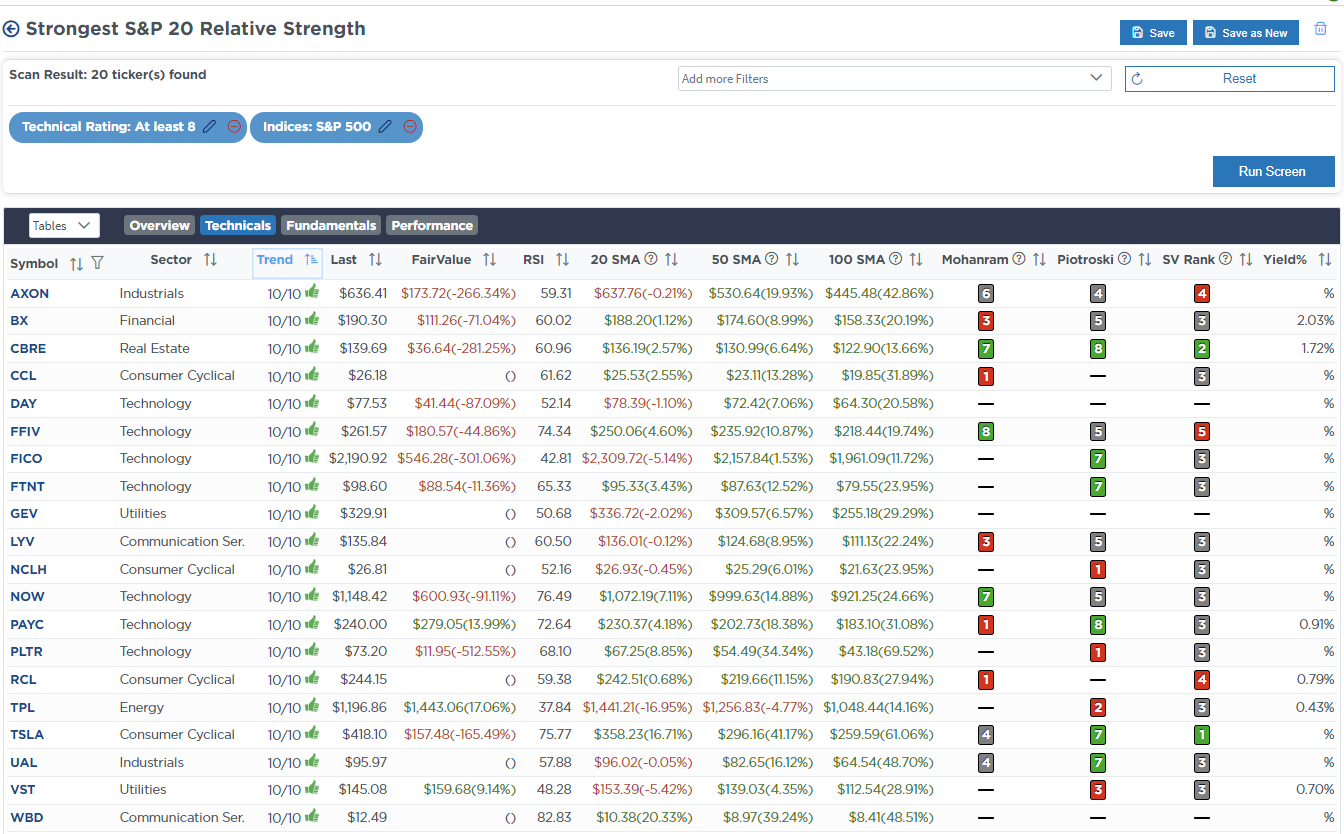

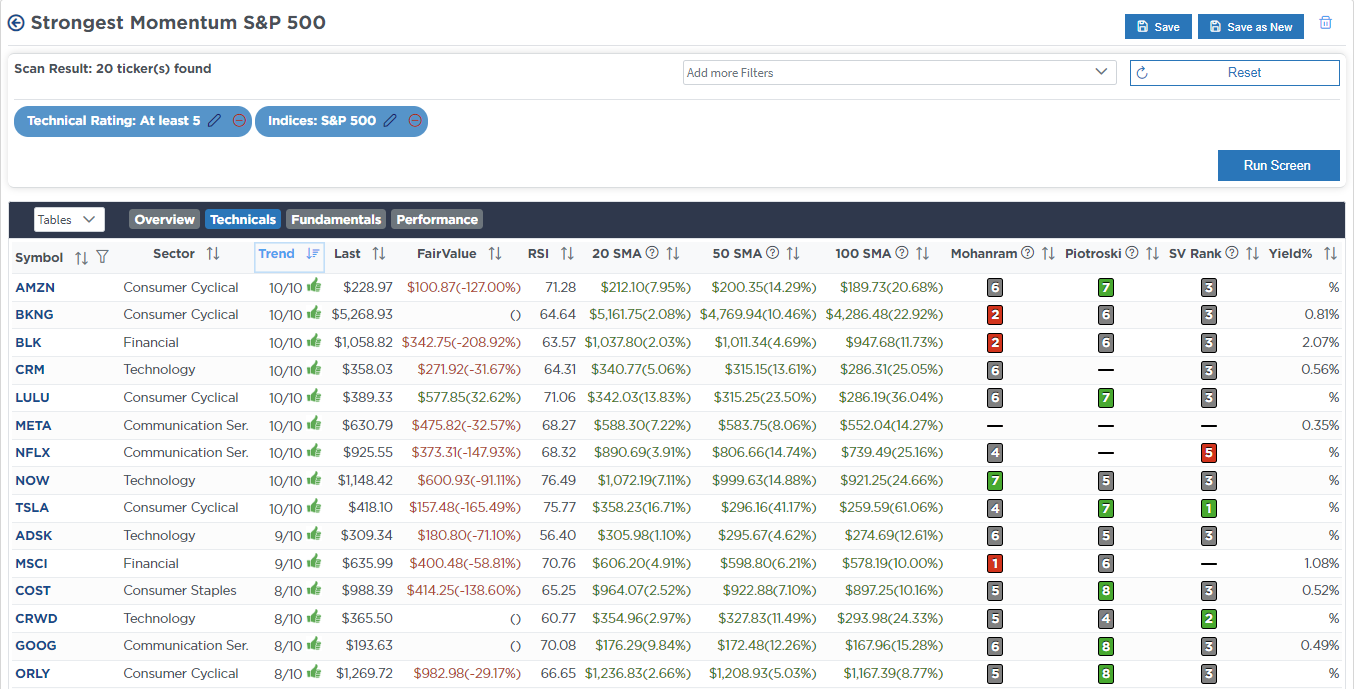

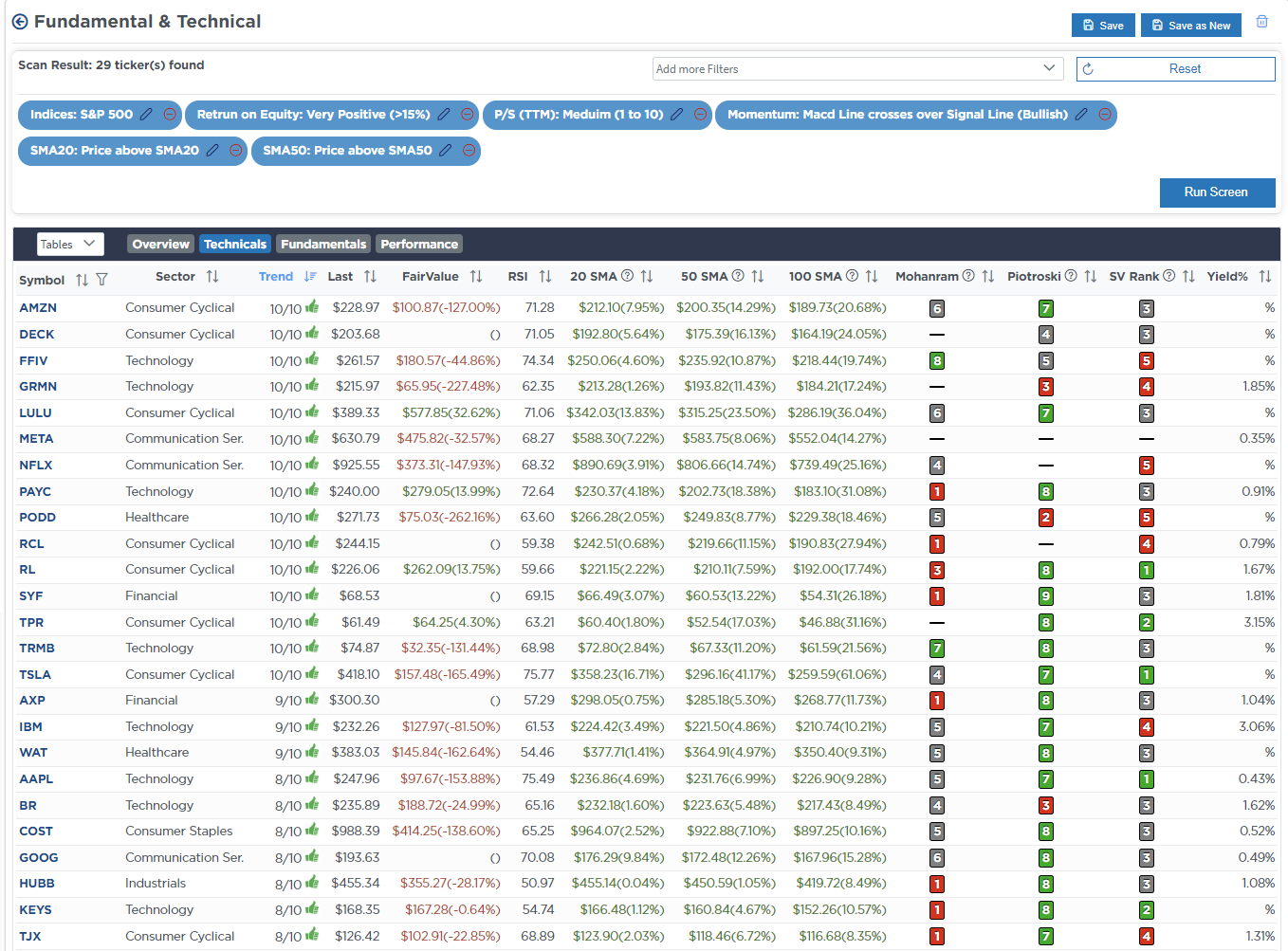

Weekly SimpleVisor Inventory Screens

We offer three inventory screens every week from SimpleVisor.

This week, we’re looking for the High 20:

- Relative Power Shares

- Momentum Shares

- Basic & Technical Power W/ Dividends

(Click on Photographs To Enlarge)

RSI Display screen

Momentum Display screen

Basic & Technical Display screen

SimpleVisor Portfolio Adjustments

We publish all of our portfolio adjustments as they happen at SimpleVisor:

No Trades This Week

Lance Roberts, C.I.O., RIA Advisors

Have an incredible week!