{kind=link}

The prospect of a Trump presidency has led to a lot debate and hypothesis about how markets would possibly react. Relying on what insurance policies are ultimately handed, there are potential dangers and alternatives in each the inventory and bond markets. Whereas the market surged instantly following the election, many potential future headwinds might impression returns from financial development, financial and financial coverage, and geopolitical occasions.

Listed below are some fast ideas about what we at RIA Advisors take into consideration the inventory and bond markets in 2025.

Inventory Markets

Upside Potential: Through the Trump presidency, he’ll deal with making certain the Tax Lower and Jobs Act, handed in 2017, doesn’t sundown in 2025, which is able to maintain company tax charges at 21%. Nevertheless, it’s not unlikely that he may also push for a brand new company tax lower invoice at a decrease charge, nearer 15%, which was his authentic objective throughout his first time period. Whereas sustaining the company tax charge at 21% will assist companies keep present profitability, a decrease charge would profit sure sectors like client discretionary and expertise, the place earnings are particularly delicate to tax adjustments. Monetary shares might additionally profit from Trump’s historical past of deregulation, probably resulting in extra mergers and funding alternatives. In actual fact, throughout his first time period, the S&P 500 rose almost 70%, partly as a result of these pro-business insurance policies.

Technically, the market stays on stable bullish underpinnings with very excessive ranges of anticipated earnings development heading into 2025. The bullish pattern stays intact, and as mentioned, the seasonally robust interval of the 12 months has began. Notably, company share buybacks and year-end efficiency chasing will help the final two months of the 12 months.

“In response to Morningstar, throughout the first half of 2024, solely 18.2% of actively managed mutual and exchange-traded funds outperformed the cap-weighted S&P 500 index. There are a number of causes for this, together with the shortage of allocation to the ‘Magnificent 7,’ dispersion in returns of holdings, and lack of allocation to non-traditional property.

Nevertheless, there are dangers.

It’s Not All Roses

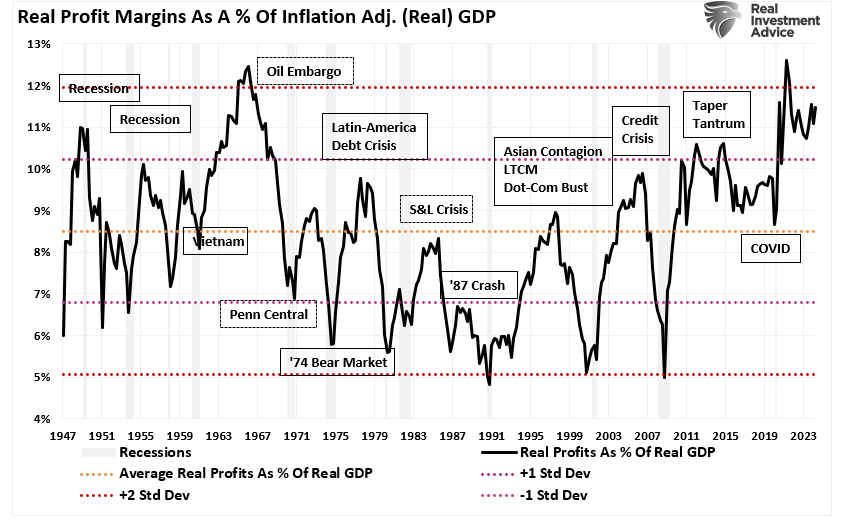

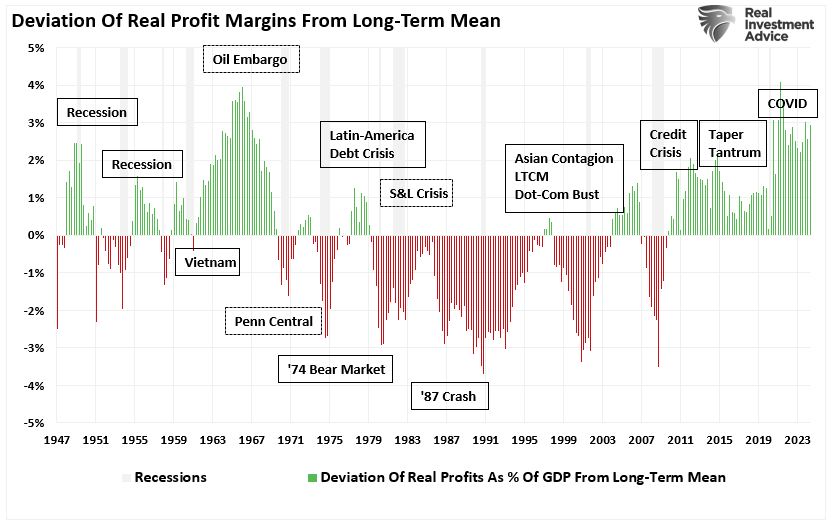

Draw back Dangers: It’s not all rosy. A Trump presidency additionally brings danger from protectionist commerce insurance policies, together with larger tariffs on Chinese language items. These tariffs can probably disrupt provide chains and enhance prices for customers and corporations. Moreover, if there are deep cuts to Authorities employment or spending, such would additionally sluggish financial development greater than anticipated and will offset the advantage of the extension of tax cuts. Nevertheless, whereas these dangers are current, essentially the most important danger is a reversion of financial development, negatively impacting company profitability. The chance of investor disappointment is elevated with company earnings already considerably deviated from long-term means.

Backside Line: Shares would possibly see an preliminary soar on business-friendly guarantees however might face challenges if tariffs or unpredictable governance introduce financial shocks that suppress company profitability.

Bond Markets

Causes for Warning: The bond market offered off sharply following the announcement of a Trump presidency. Such was not unsurprising, as bonds sometimes react negatively to narratives which may result in larger inflation and rising rates of interest. The preliminary knee-jerk response within the bond market was the belief that the administration would emphasize deficit-financed spending on infrastructure or protection. Such spending would definitely result in stronger financial development and better wages, which might maintain a better degree of inflation than witnessed from 2008 to 2020. The Federal Reserve will keep larger rates of interest to align with stronger financial development if stronger development happens. In such an setting, bond costs would fall to accommodate larger financial exercise. Such an consequence would stabilize bond costs at a better “terminal charge,” decreasing the potential upside in proudly owning bonds.

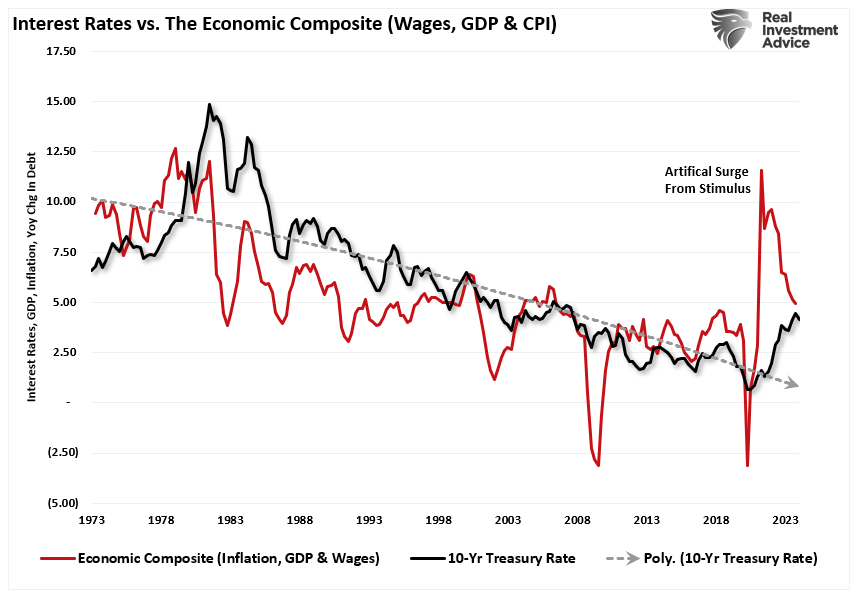

As mentioned in “Charges Are Going A lot Greater?” there is a crucial correlation between wages, financial development, inflation, and rates of interest. To wit:

“If we create a composite index of wages (which gives client buying energy, aka demand), financial development (the results of manufacturing and consumption), and inflation (the byproduct of elevated demand from rising financial exercise). We then evaluate that composite index to rates of interest. Unsurprisingly, there’s a excessive correlation between financial exercise, inflation, and rates of interest as charges reply to the drivers of inflation.”

Due to this fact, the bond market has a proper to be involved if a Trump presidency can foster a sustained degree of upper financial development and elevated wages, making a comparative inflation degree. Such inflation would increase yields to align with these variables.

Nevertheless, such will seemingly be tougher to do than many suppose.

It’s The Economic system

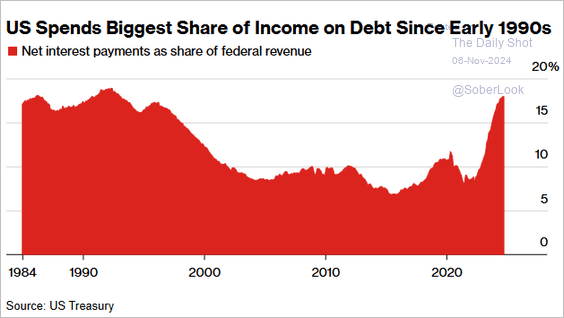

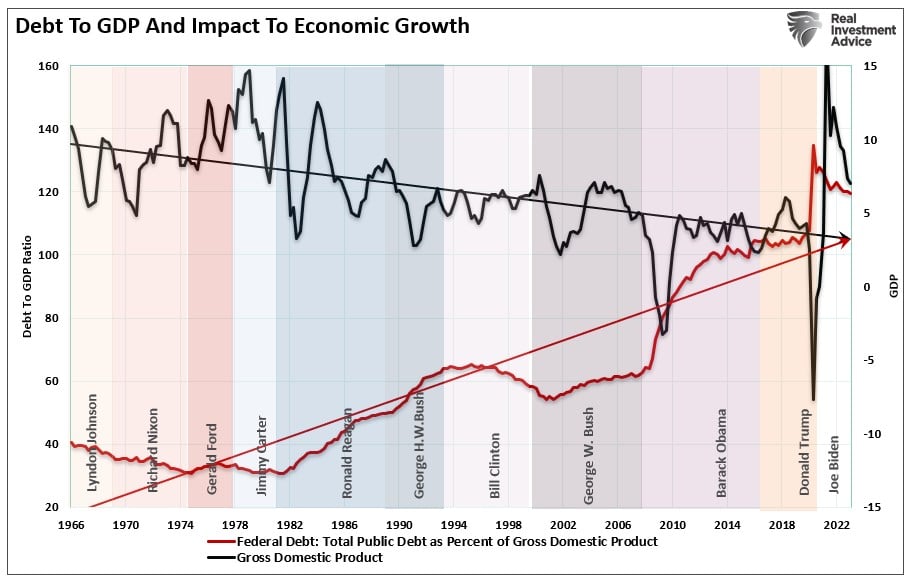

Potential Silver Linings: On the flip aspect, a Trump presidency should cope with excessive debt ranges and a big fiscal deficit. Will increase within the nationwide debt had been squandered on non-productive investments, and rising debt service ends in a damaging return on funding. Due to this fact, the bigger the debt steadiness, the extra economically damaging it’s by diverting growing quantities of {dollars} from productive property to debt service. As rates of interest enhance, extra federal tax income is diverted into servicing the nationwide debt.

Whereas many count on that Trump’s insurance policies will result in inflationary pressures, what must be evident is that will increase in debt and deficits proceed to divert extra tax {dollars} away from productive investments into the service of debt and social welfare. The result’s decrease, not larger, financial development, inflation, and, in the end, rates of interest.

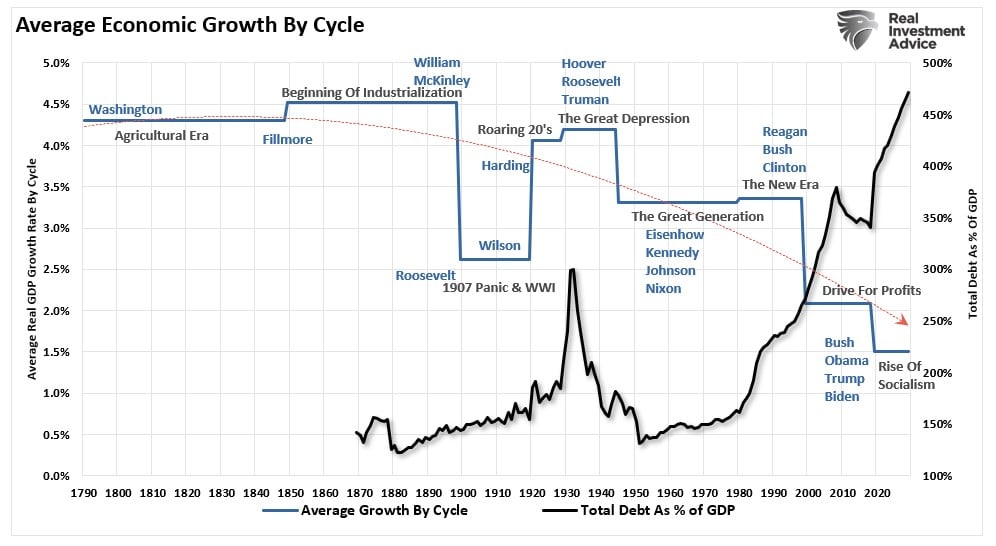

When put into perspective, one can perceive the extra important downside plaguing financial development. An extended take a look at historical past clearly exhibits the damaging impression of debt on financial development.

Moreover, adjustments in structural employment, demographics, and deflationary pressures derived from adjustments in productiveness will enlarge these issues. Trump or another president can’t successfully resolve these specific points.

Total Takeaway

Below a Trump presidency, the outlook for the inventory and bond markets presents a mix of alternatives and challenges. The outcomes for each are closely depending on which insurance policies change into realities.

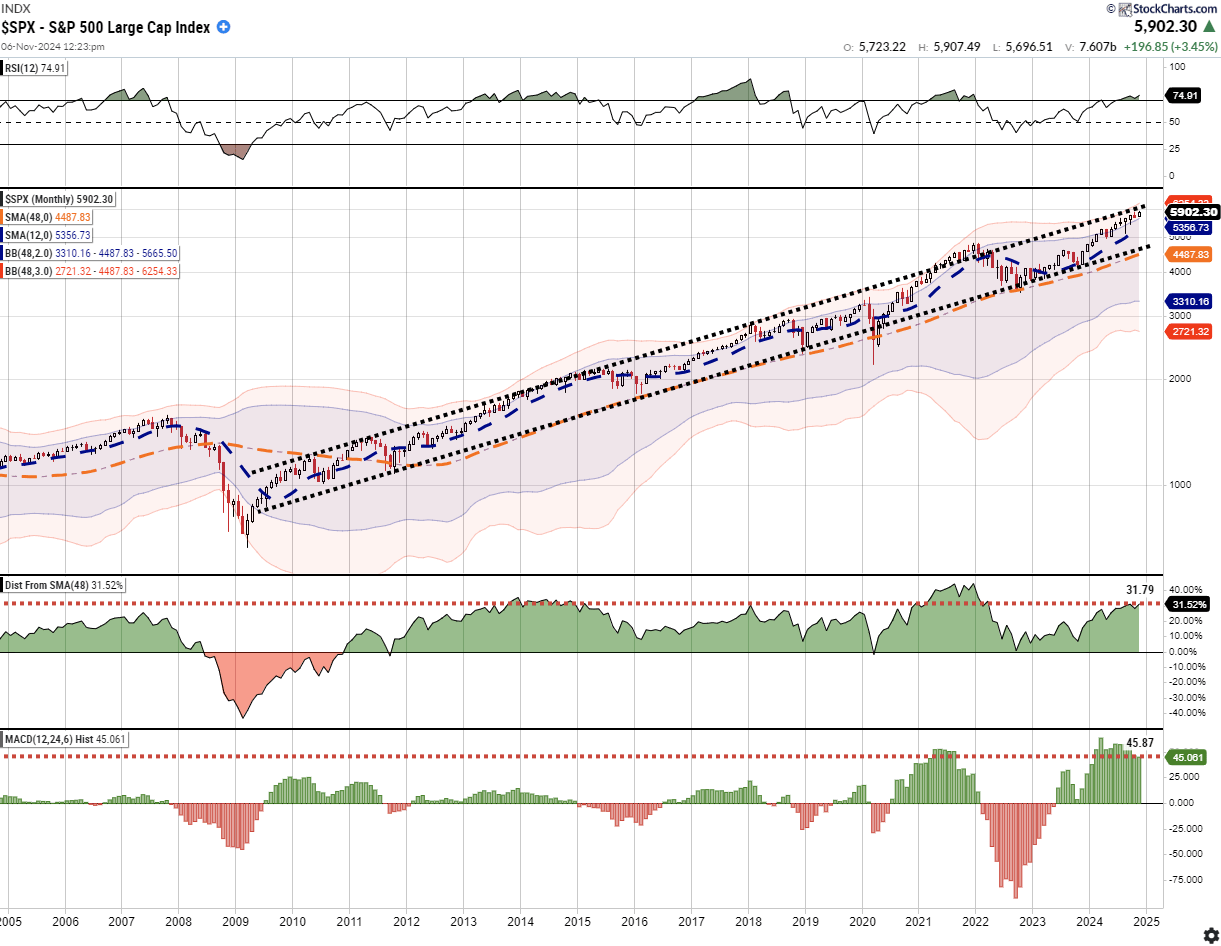

The one massive concern for us at RIA Advisors continues to be a market that has loved outsized returns over the previous two years and deviates from long-term means. With the markets being overbought month-to-month and buying and selling on the high of its long-term pattern channel, expectations of additional market upside appear overly assured with out some correction first. Since 2009, the market has retested the 4-year shifting common quite a few instances. Such is a traditional and wholesome course of for an ongoing bull market, and a imply reversion must be anticipated sooner or later sooner or later. Nevertheless, such an occasion isn’t seemingly between now and year-end.

Moreover, market predictions hinge on the steadiness between development and inflation. Whereas Trump has many insurance policies on his want checklist, these insurance policies have to be handed by a closely bipartisan Congress. With solely slim majorities to work with, there’s a danger of defection on some payments, notably by the “Freedom Caucus,” which might oppose giant deficit spending payments.

Lastly, shares might rally on tax cuts however would possibly stumble if tariffs weigh closely on world commerce. Bonds might certainly face headwinds, however the “3-Ds” of money owed, deficits, and demographics will proceed to plague financial development. Whereas there was an preliminary surge in shares and a sell-off in bonds on the announcement of a Trump presidency, there’s nonetheless a really lengthy street forward that buyers should navigate. Fed coverage, economics, earnings and company profitability all pose danger to longer-term outlooks.

Buyers ought to keep knowledgeable and take into account a diversified method, as the following presidency guarantees to carry each alternatives and dangers throughout asset lessons.

Publish Views: 932

2024/11/08