{kind=link}

Artificial biology is the only most fun theme we cowl, nevertheless it’s additionally been an enormous disappointment for traders. Harnessing the facility of nature sounds simpler than it seems. Simply over a decade in the past, Intrexon went public with their “channel” enterprise mannequin which smelled much like Ginkgo Bioworks (DNA), one other synbio disappointment that bought Zymergen, one other failure of a synbio firm. These are just a few examples of how exasperating it’s been to be an artificial biology investor. That brings us to the subject of immediately’s article – Twist Bioscience (TWST).

A Path to Profitability

We cowl round 460 disruptive tech shares and have invested in over 35 which permits us to identify tendencies throughout firms and industries. For instance, stock points are plaguing {hardware} firms as provide chain whiplash results lastly manifest themselves from The Rona. Moreover, each {hardware} and software program firms are conserving money as elevating capital turns into harder. It’s virtually anticipated that firms with dwindling money positions must be addressing these constraints with some said plan to realize profitability. Right here’s the place Twist sits.

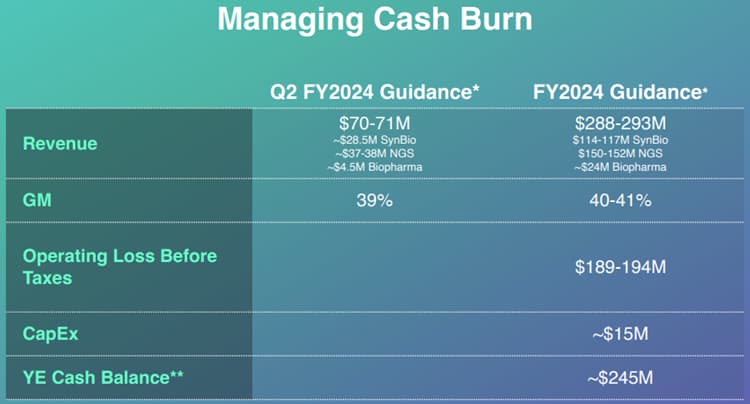

On the finish of 2023, the corporate had money and money equivalents of $311 million and expects to burn by way of $66 million this yr primarily based on the beneath desk taken from their newest earnings deck.

Assuming the identical burn price going ahead, Twist has a runway of three.7 years ($245 million/$66 million burn per yr). Given this firm has now blown by way of greater than $1 billion placing collectively their synbio platform, traders are understandably involved when critics query gross margins that might not be what they appear.

The Brief Report

Twist didn’t handle final yr’s brief report by Scorpion Capital a lot besides to say in a concise press launch that it was “extremely deceptive, with many distortions and inaccuracies.” (Then Twist pointed to their ESG report which is a purple flag in itself.) Our article on the matter titled Twist Bioscience Will get Stung by Brief Report pointed to issues we had lengthy earlier than Scorpion raised their pointy tail. “Twist is competing towards some very established firms and spending a ton of cash to take action, notably on the gross sales aspect,” we wrote in early 2022, noting that our “greatest concern surrounds Twist’s companies enterprise mannequin which we imagine could possibly be displaced by a {hardware} enterprise mannequin such because the one on supply from DNA Script.” Whereas that concern is exclusive to their artificial DNA enterprise, the linear scalability downside is attribute of each companies enterprise on the market. We a lot favor platforms which might be offered to shoppers together with high-margin consumables.

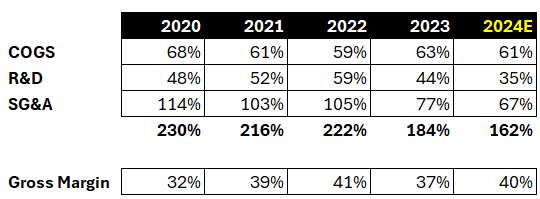

Twist supplies a companies platform in a extremely aggressive area which implies they’re all the time feeling pricing pressures. It’s no shock that their declare of with the ability to broaden gross margins ought to come into query together with accusations that they’re stuffing cost of goods soutdated (COGS) into R&D bills and capital expenditures (capex). We’ve taken each COGS and working bills and expressed these three gadgets as a share of complete revenues over time (together with 2024 estimates).

To attain profitability, these three buckets will – in complete – have to fall beneath 100%. Whereas they’ve dropped some in 2023, and probably extra in 2024, they’re nonetheless a good distance from seeing profitability, and we haven’t even thought of capital expenditures. The outdated saying that “income are an opinion, money is a truth,” means we’re in the end interested by seeing constructive working money flows above all else.

Twist continues spending a great deal of cash on growing DNA storage with $38 million slated for that objective in 2024. We don’t imagine that’s an economically viable path primarily based on our analysis piece titled, DNA Information Storage: A Resolution In search of a Downside?, and that was one other criticism by Scorpion Capital. In Spring of 2021, Twist talked about “trade leaders becoming a member of forces to advance DNA information storage,” then identify dropped Microsoft, Illumina, and Western Digital. Extra lately the message has turn into extra tame as they discuss debuting their Terabyte Century Archive answer in 2025. An article by GenomeWeb final yr talks about how “Twist will sluggish its funding in DNA-based information storage attributable to a perceived lack of competitors,” and take a services-based strategy. Once more with the companies that are a lot much less fascinating than a consumables-based enterprise mannequin. Maybe there’s no competitors for a purpose.

Investing in one thing that won’t generate revenues for some time – if ever – may delay profitability, one thing Twist talked about of their most up-to-date earnings name when stating, “a number of years in the past, we established a plan to realize profitability for the enterprise.” So, let’s have a look at what Twist Bioscience stated a number of years in the past.

Predicting Profitability and Progress

Scorpion’s report made some very particular accusations as follows:

- Twist is misclassifying COGS

- as an R&D expense

- as CAPEX through two automobiles:

- a) its purported “Manufacturing unit of the Future,”

- b) its “DNA Storage Initiative”

Per the desk we checked out earlier, R&D as a share of income decreased in 2023. As for capex, they’re guiding to $15 million in 2024. That’s all good, however let’s take a holistic have a look at the steering Twist offered a number of years in the past.

Again then we have been puzzled why they’d give two years of steering in a row, and now it’s apparent why that’s not a good suggestion. They missed 2023 midpoint income steering by 7.5% and their 2024 midpoint income steering is lacking their outdated 2024 steering by 17%. They obsessively talked about gross margins again then estimating almost 50% for 2024. That’s now anticipated to be 40%. So, when Scorpion attacked Twist’s declare of hitting 60% gross margins, they appear to be proper up to now.

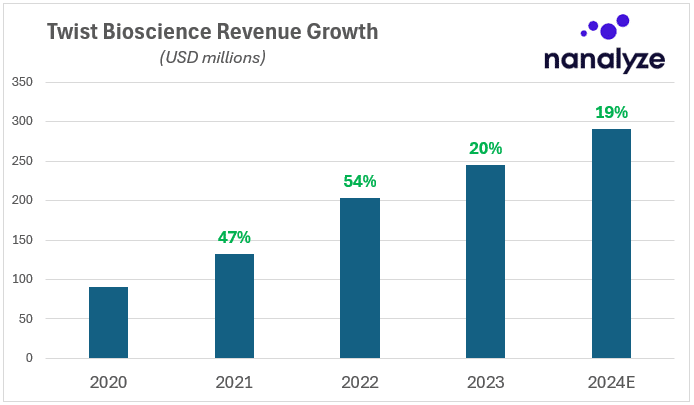

In an August 2022 investor deck, Twist mentions twice that they’ll hit EBITDA breakeven when the core enterprise (Synbio and NGS) hits $300 million, so we’re holding them to that. The midpoint for these two segments this yr is $266.5 million. With 13% extra development in 2025, they’ll be on the $300 million goal. Primarily based on historic income development, this must be attainable.

Purchase or Promote Twist Inventory

Everybody desires to be instructed what shares to purchase and when to promote them. That’s as a result of taking accountability on your funding choices isn’t a cushty factor to do. Should you’re proper, that’s anticipated and no person cares. Should you’re incorrect, folks will crawl out of their graves to chastise you. Our funding in Twist Bioscience sits the place it has for some time now – at half a place dimension – as a result of we had (and at present nonetheless have) reservations in regards to the firm even previous to the brief report. Certain, they’re constantly rising revenues over time. That’s nice to see, however the profitability questions stays, particularly since they’ve dramatically missed their 49% gross margin goal for 2023. Traders may give them a cross as a result of these forecasts have been made up to now again, however the obvious gross margin ceiling of 40% is trigger for concern. Is that sufficient leeway to function a worthwhile companies enterprise?

That brings us to the “EBITDA breakeven” goal they’re working in direction of. After they say “a number of years in the past, we established a plan to realize profitability for the enterprise,” that’s what we assume they’re speaking about. (It could be good in the event that they explicitly said these objectives of their earnings deck as a substitute of us having to tease them out from varied items of previous collateral.) On the plus aspect, Twist has reduce on working bills and hopefully – after they laid off 25% of their employees – kicked all these ESG / DEI time wasters to the curb the place they belong. That occasion was stated to maneuver manufacturing from South San Francisco to the brand new facility in Portland – the “Manufacturing unit of the Future” – and the announcement coincided with the 2023 steering drop (and 2024 steering withdrawal) that was attributed to “the dangers of managing the workforce discount.” Truthful sufficient. Money burn has been tamed, they usually seem to have a number of years of runway remaining a minimum of which ought to allow the agency to achieve profitability while not having to boost capital and show Scorpion Capital incorrect as soon as and for all.

Conclusion

Out there performs on artificial biology have all however dried up as a result of most by no means realized their promise of harnessing the powers of nature. It’s loads harder than it seems. Gene modifying – a device of synbio – reveals early promise, whereas Gingko Bioworks struggles to show the idea of their platform whereas paying their leaders ludicrous quantities of cash. There’s each purpose to view Twist Bioscience with a substantial amount of suspicion, and that’s the place we sit immediately. If 2024 sees steering met or exceeded with no capital raises popping out of the blue, we’ll then see if 2025 brings us what the corporate has promised – a severe have a look at profitability which proves that Twist Bioscience has been proper all alongside. Any extra setbacks they usually’ll probably exhaust what little endurance traders have left.