{kind=link}

The dying profit assure reset possibility

The dying profit assure is the core of segregated fund insurance policies. It ensures a set payout to beneficiaries, adjusted for any withdrawals. Canada Life presents a reset possibility for this assure, which updates the dying profit assure every year based mostly on market values, locking in development. This implies the upper funding quantity is protected.[1]

Canada Life has prolonged the utmost age to reset from 70 to 80,[2] catering to Canadians’ longer lives. With this selection added to a Canada Life segregated fund coverage, you may assist safe beneficial properties to your purchasers and assist them really feel extra assured in regards to the legacy they’re constructing, for longer.

Easy administration with a ‘set it and overlook it’ security internet

Investments might be advanced. Including Canada Life’s reset choice to a segregated fund coverage simplifies issues. It acts as a “development seize” mechanism, locking in beneficial properties every year while not having to observe market cycles. This supplies stability and preserves development.

Maximizing a legacy by development safety

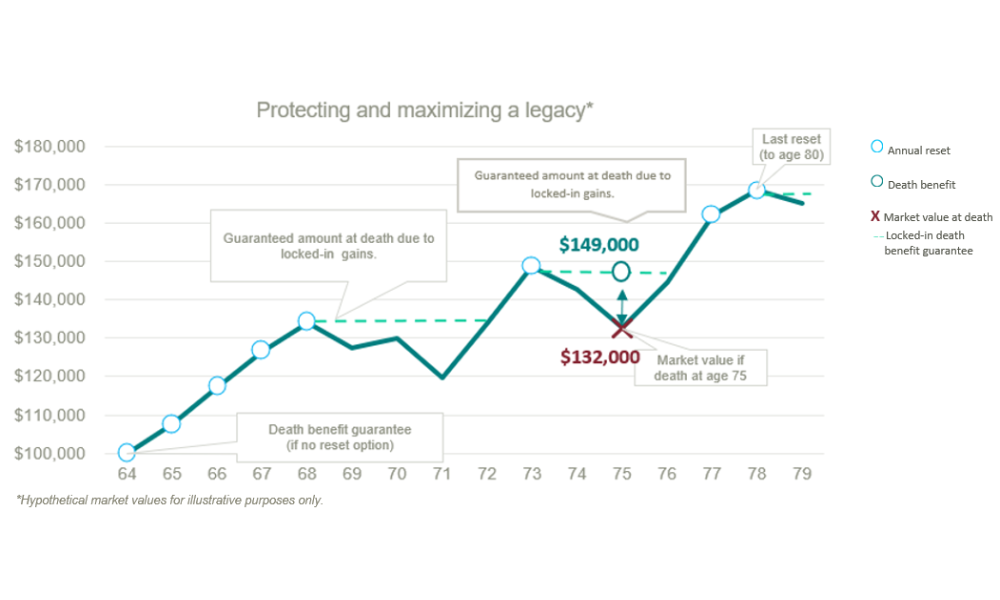

Think about Catherine, who at 64 is planning for her retirement. Her aim is to construct an inheritance for her grandchildren whereas balancing her want for development with a way of safety. She invests $100,000 right into a Canada Life 75/100 segregated fund coverage and provides the annual dying profit assure reset possibility. By the point she’s 79, her coverage has grown to $170,000 as a result of reset possibility capturing and locking in market development years. If Catherine had handed away throughout a market downturn at age 75, her beneficiaries would have obtained her final locked-in reset quantity of $149,000, regardless of the market worth of the portfolio being solely $132,000 at the moment. This quantity would make a major distinction to her grandchildren’s lives.